These days many commentators are declaring the death of the “60-40 portfolio”, which is 60% in equities and 40% in bonds, that has been the core portfolio concept in retirement strategies. With plunging interest rates the future returns are likely to be low but going out on the risk curve is not a free lunch as valuations on growth pockets have become quite stretched. Whether or not the 60/40 portfolio is dead or not is semantics and not the point of this note. Many commentators have recently talked about the fact that the correlation between equities and bonds has historically been more positive than the recent decades with more negative correlation making asset allocation strategies look easy. Recently the correlation is turning positive again and many have argued that the link is inflation, which is not unreasonable, but is this positive correlation a bad thing?

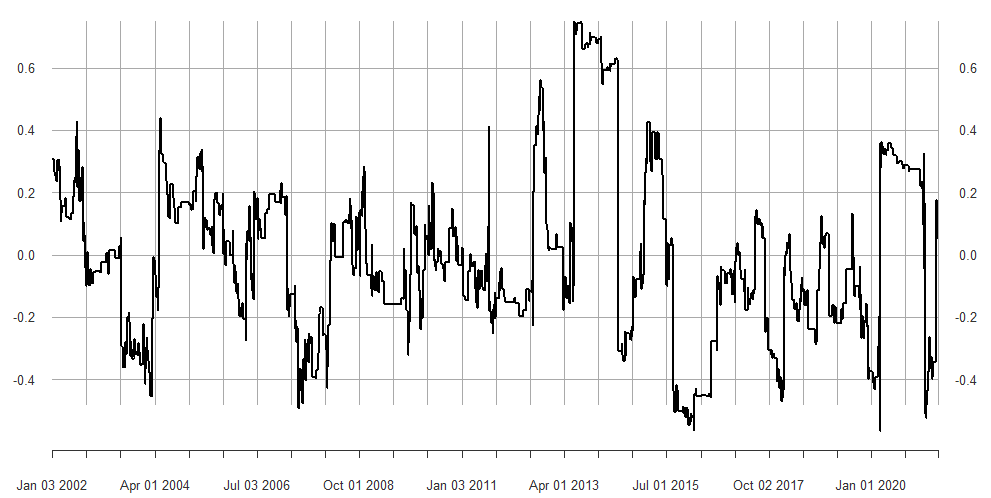

The more interesting question is whether bonds still play a role in portfolios. Yes, they do. The chart below shows the real strength of bonds in the portfolio. The chart shows the running correlation between global equities and global government bonds on the 10% worst trading days in global equities in 1-year sliding window. As we can see, the overall tail-risk correlation is slightly negative over the entire period since 2002 and is currently slightly positive but not alarmingly high. That is not to say that we could not get there on an inflation shock, but the tail-risk correlation shows you that bonds, despite their low expected return, are still the best way to offset risk for ordinary long-term investors. Also note that the worst tail-risk correlation happened during Bernanke’s taper tantrum in 2013, followed by the Greenspan surprise interest rate hike in 2004 and the EM/oil selloff in 2015.