The consensus is for the European Central Bank to begin tapering purchases under the PEPP Program this quarter and be announced as soon as this Thursday. If that were the case, the ECB would lead the Federal Reserve to end accommodative monetary policies.

That would be a clear signal that the bear bond market has begun and that it is time to short Bunds and Treasuries. However, how to do that?

We will talk about that shortly. First, it’s essential to understand what is at stake during this week’s ECB meeting.

- Economic outlook revision. Following a robust second quarter, the ECB will certainly need to revise projections for this year. However, would it change growth and inflation for 2022 and 2023? That is crucial because if the central bank revises inflation upwards for the next two years, it will signal that inflation is more permanent than expected. Yet, such a revision would be more significant for US Treasuries than for EGBs. Indeed, contrary to the US, inflationary pressures would still be expected to undershoot the ECB’s target after this year. In June, the central bank expected inflation to come at 1.5% and 1.4% in 2022 and 2023. A slight revision upward should still place expectations below the ECB target of 2%, meaning that monetary policy will be less accommodative in Europe but still quite loose in the long-run.

- PEPP and APP program. The PEPP program was created to stimulate the economy in the wake of the Covid-19 pandemic, and the official deadline is March 2022. The question here is whether the central bank recognizes that we are out of the pandemic period and believes that the economy doesn’t need stimulus anymore. Yet, the Delta variant might weigh in that decision. If the PEPP program ends in the first quarter of 2022, the question is whether the APP will be modified to partially substitute the PEPP. This information is critical for rates because it will imply more or less support for EGBs.

- Financing conditions. One of the most significant focuses of the ECB this year has been to maintain financing conditions loose. Yet, since the market started to speculate about tapering, rates began to rise with Italian 10-year BTP gaining 11bps in six trading days and 10-year French OAT turning positive for the first time since mid-July. While it is true that financial conditions remain extremely easy, a fast adjustment of rates higher might tighten conditions suddenly. That’s the main reason why any announcement from the ECB needs to be dovish. Hence, the market expects a “dovish taper“, which should limit market volatility.

It’s easy to conclude that whatever decision the ECB will take to taper purchases under the PEPP program, it will try to deliver it dovishly. It’s up to the market to interpret whether the dovish framework that the ECB presents is dovish enough. However, if it works, volatility can be contained. Yet, it’s impossible to ignore that times are changing fast. Suppose an announcement over the PEPP is not presented now. In that case, it must be tackled in December, adding more pressure on rates, which will be even more volatile following the German election.

Additionally, if a dovish taper is delivered on Thursday, the biggest loser might still be US Treasuries. Indeed, the Fed is falling behind the curve, and the longer it waits to taper, the more aggressive it has to be. That’s why this is also the right moment to short US Treasuries.

Using options to short Bunds and US Treasuries

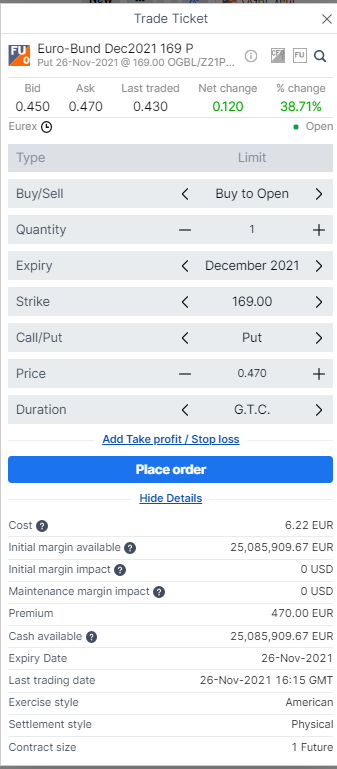

It is relatively easy to short Bunds and US Treasuries through options. Expectations are for interest rates to rise, thus falling bond prices by the end of the year. If you are long put options, you have the right to sell a bond at the strike price, exposing yourself to a limited downside (premium) and unlimited upside.

In the Saxo platform is possible to browse options by uploading the ticker and clicking on “Option Chain”. The ticker for the Euro-Bund is FGBL, while for US Treasuries, it is ZN.

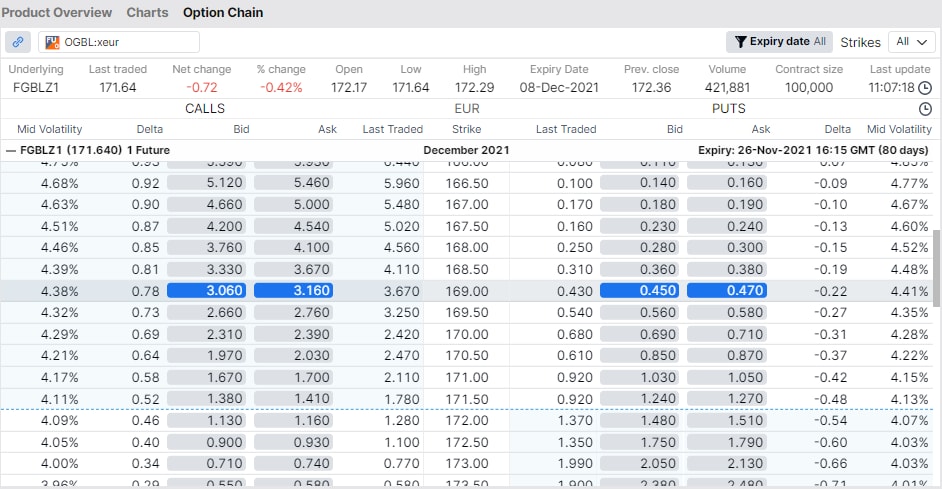

Let’s take the Euro-Bund option with the December expiry as an example. We like the December expiry because we expect yields to accelerate their rise during the last quarter of the year.

The cost of a put option with delta -0.22 today is of 0.470. Because the size of the option is 1,000, the total premium to put up to buy the put option is 470 EUR.

Similarly, the premium to pay for 10-year US Treasuries put options with a delta of -0.23 is 390 USD.