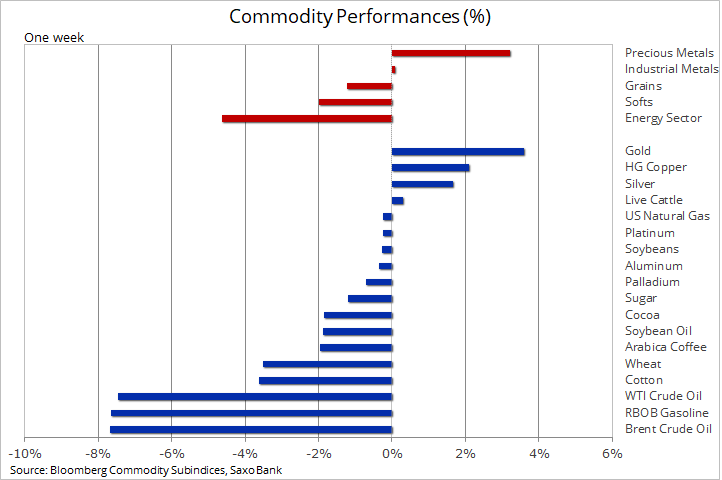

A sense of déjà vu emerged across markets this past week with some behaving like they did back in Q1 when the Covid-19 pandemic sent asset prices sharply lower. Since April, the economic impact of months of lockdowns had been painted over by a massive rally in global stock markets. The support, however, from the Fed (wall of liquidity), TINA (there is no alternative) and FOMA (fear of missing out) showed its first cracks this week.

Despite a very dovish message from the U.S. Federal Reserve, markets have returned to risk-off mode with the dollar reclaiming some lost ground and the S&P 500 index on Thursday experiencing its biggest drop since March 6. Treasury yields were heading toward all-time lows thereby supporting gold while crude oil’s somewhat speculatively fueled rally came to halt after the price had run ahead of current fundamentals.

The combination of the U.S. Federal Reserve seeing a long road to recovery and the World Bank confirming the deepest global recession since WW2, and not least the risk of a second wave building in the U.S. and some other countries, has all but confirmed that the much touted V-shaped recovery is going to be very difficult to achieve.

Crude Oil: The outlook for demand for key commodities, not least energy, remains challenged by the not yet under control Covid-19 pandemic. While the situation in Europe, with the exception of the U.K., and China among others has improved, globally it is still worsening with a record number new cases being reported – mostly in the Americas and South Asia. There are more and more indications that a possible second ware of the pandemic could be taking hold in some U.S. states and that was the key driver behind the latest market developments. Not least considering that most countries experiencing a second wave, including the U.S., are unlikely to adopt renewed lockdowns measures for fears of the economic impact.

These developments helped send crude oil sharply lower to record its first weekly drop since April. The risk of a second wave slowing the recovery in global demand will pose multiple challenges. Not least to the OPEC+ group of producers who just recently managed to agree a one-month production cut extension. These cuts now translate into spare capacity which can be brought back when demand has recovered and the global overhang of stocks have been lowered. The group can for a period control supply, but not demand, and a weak recovery in demand may challenge the group’s resolve with the risk of quota cheating emerging.

The impact of Saudi Arabia’s ill-timed price war back in March continues to be felt in the U.S. where millions of extra barrels of imported oil from the Kingdom has helped send commercial stocks to a record high. While these flows will slow over the coming weeks, the positive impact on prices may not materialize for some time due to the combination of elevated gasoline and not least distillate stocks and the slow process with which demand continues to recover. Adding to this the risk that some shale oil producers may start to increase production as long forward prices remain around current levels.

Both WTI and Brent crude oil did not manage to close the gaps that were left open when the markets collapsed in early March after Saudi Arabia embarked on its short-lived price war. Instead, the market behavior following the agreement by OPEC+ members to extend the 9.7 million barrels/day production cut until end July, ended up signaling the beginning of an overdue correction/consolidation.

Hedge funds have been strong buyers of WTI crude since early March with the net-long reaching 380 million barrels in the week to June 2, the largest bullish bet on WTI crude oil since August 2018. While our longer-term bullish outlook hasn’t changed the next few months may look a bit more challenging with renewed Covid-19 outbreaks in the U.S. being the trigger that reduces the speculative position.

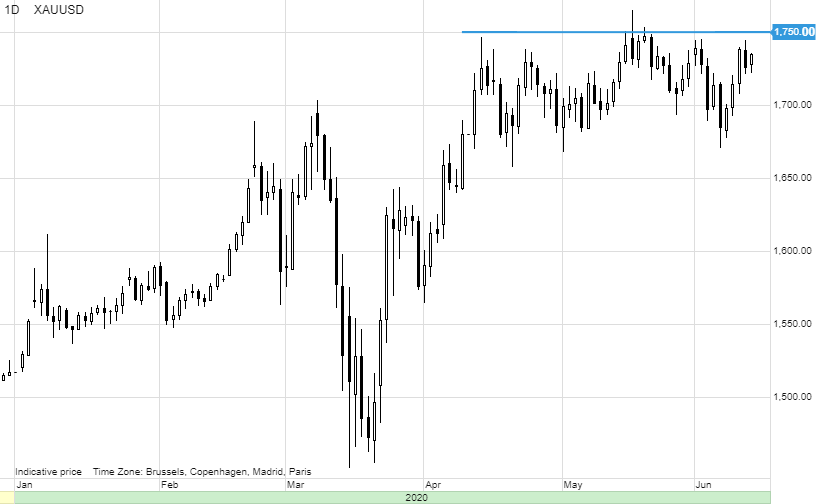

Precious metals: Gold’s inability, following the dovish FOMC meeting, to find a way through resistance above $1750/oz helped trigger some profit taking before renewed stock market and Covid-19 worries helped provide fresh support. While not offering any new initiatives, such as yield-curve control, the FOMC did provide a supportive outlook for gold. Official rates expected to be kept at zero through 2022 while robust monetary support will be provided through the continued buying of bonds.

We maintain our bullish outlook for silver and not least gold now that its premium to silver has narrowed. The main reasons why we expect to see a minimum move to $1800/oz in 2020 and a fresh record high over the coming years are:

- Gold acts as a hedge against Central Bank monetization of the financial markets

- Unprecedented government stimulus and political need for higher inflation to support debt levels

- The inevitable introduction of yield controls in the US forcing real yields lower

- A rising global savings glut at a time of negative real interest rates and unsustainably high stock market valuation

- Raised geo-political tensions on Covid-19 blame game ahead of U.S. November elections

- A weaker U.S. dollar

Base metals: HG Copper was only surpassed by gold this week as it raced higher to reach $2.71/lb, the highest level since January before drifting lower as virus focus returned. The recent break above $2.50/lb, a key level of support-turned-resistance, finally saw hedge funds join Chinese speculators and turn bullish on the metal. Apart from the fresh accumulation of speculative longs, the rally from the March nadir has been driven by improved industrial demand in China, virus-related supply disruptions in South America and more recently a steady decline in stocks held at exchange-monitored warehouses, both in London and not least in China