While pockets of weakness have started to emerge across the metal and agriculture sectors, crude oil remains in demand on a supportive combination of rising demand and OPEC+ keeping supplies tight. Halfway through June and the Bloomberg Commodity sub-indices are showing losses across all sectors with the exception of energy. Agriculture commodities trade softer with several regions upgrading their production forecasts due to improved weather conditions. Scraping the bottom in terms of sector and individual commodity performances we find industrial metals and copper which is trading at a six-week low and down 7% this month.

Apart from the loss of momentum since April, industrial metal prices are weaker in a continued response to Chinese authorities stepping up their efforts to curb commodity prices. The latest order coming the State-owned Assets Supervision and Administration Commission which have ordered state enterprises to control risks and limit their exposure to overseas commodity markets. In addition, the National Food and Strategic Reserves Administration will soon start to release national reserves of copper, aluminum and zinc which will be sold in batches to fabricators and manufacturers.

In response to these developments copper fundamentals have softened with the cash discount to the three-month contract on LME rising to the highest contango in a year, a sign of rising supply. Chinese importers meanwhile are currently paying the smallest premium over LME in more than five years. Adding to this the recent loss of momentum have seen speculators cut bullish bets on high grade copper to a one-year low. We see higher prices over the coming years on rising demand from the green transformation push, but in the short term the price has – as mentioned – run out of fundamental support, and until they start to reverse copper and industrial metals in general may trade defensively.

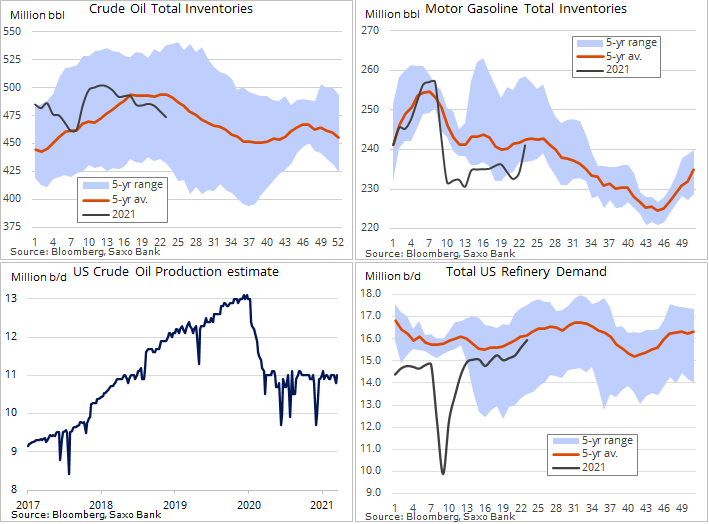

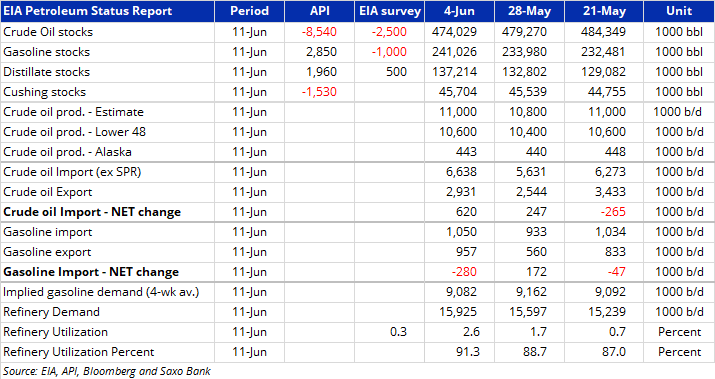

Returning to crude oil where speculators remain strong buyers in the belief downside risks are limited with OPEC+ keeping supplies tight at a time of rising demand. A demand growth that according to the IEA could rise to post pandemic levels late next year. An additional bid reached the market last night after the industry-funded API said crude oil stocks fell 8.5 million barrels last week, if confirmed by the EIA later today it would be the largest drop since January and the fourth consecutive decline. Somewhat offsetting is the outlook for another weekly rise in product stocks as refineries gear up for a summer of strong demand.

Adding to crude oil’s current bid are forecasts from the world’s top commodity traders, all speaking at the FT’s Global Commodity Summit, that oil prices could return to $100 over the coming years as investment in new supplies slows down with oil majors diverting capex towards renewables instead of continued oil and gas production. It highlights a potential rising dilemma where politicians and investors want to move towards renewables at a much faster pace than actual changes can be made. Thereby creating the risk of a supply shortfall before demand eventually begins to slow towards the second half of this decade.

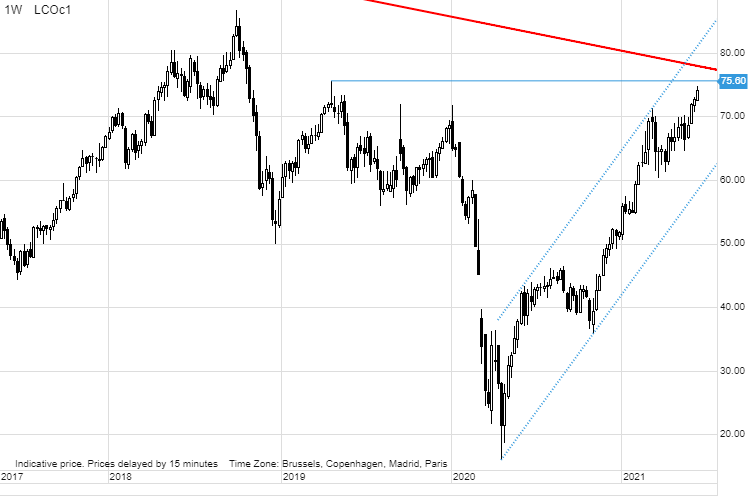

Brent crude oil has set its sight on the 2019 peak at $75.6 ahead of the downtrend (red line) from the 2008 peak. Some focus on today’s FOMC meeting which may yield a change in the interest rate outlook while the market seeks further clues about the Fed’s view on inflation, and with that the need for inflation hedges through long commodity exposure.