What is our trading focus?

OILUKAUG20 – Brent Crude Oil (August)

OILUSJUL20 – WTI Crude Oil (July)

XOP:arcx – Oil & Gas Exploration & Production

XLE:arcx – Energy Select Sector SPDR Fund (Large-cap US energy stocks)

____________________________________________________________________________________________________

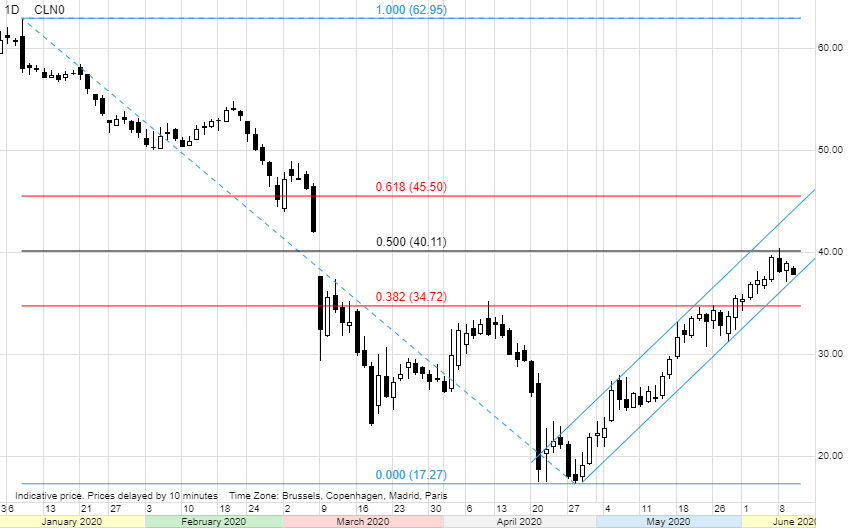

Crude oil’s behavior following the agreement by OPEC+ members to extend the 9.7 million barrels/day production cut until end July, could be signaling the beginning of an overdue consolidation phase. With WTI and Brent crude oil almost having closed the gaps established after the March 6 collapse, when Saudi Arabia began their price war, the question is how much further the price can climb without additional improvements in the fundamental outlook.

Challenging the current price is the risk of non-compliance from members of the OPEC+ group, the risk to demand from renewed flareups in Covid-19 cases and reports that US shale oil producers are already preparing to increase production. Adding to this the risk of how the OPEC+ group, now holding a vast amount of spare capacity, will manage to return supply to market without adding too much too soon.

The July WTI contract managed to retrace 50% of its Covid-19 and Saudi price war related sell-off to reach $40/b, now resistance. With support at $35/b the risk of a 10 to 15% correction has emerged. Hedge funds have been strong buyers of WTI crude since early March with the net-long reaching 380 million barrels in the week to June 2, the largest bullish bet on WTI crude oil since August 2018. While the prompt spread contango has almost disappeared, currently at 25 cents/b compared with $3.5/b on April 28, the temptation to book profit may also weigh on crude oil’s short-term outlook.

The outlook for demand remains challenged by the not yet under control Covid-19 pandemic. The WHO has warned about a ‘worsening’ virus situation worldwide, something that was repeated by Fauci, US leading infectious disease expert, yesterday when he said the pandemic is far from over. While the situation in Europe and China among others have improved, globally it is still worsening with a record 135,000 new cases reported on Sunday with almost 75% of the most recent cases coming from 10 countries – mostly Americas and South Asia.

Cross border travel restrictions by land and air remain in place around the world and with millions of workers unlikely to get their jobs back anytime soon, the recovery in demand may prove slower than expected. Some are even at this early stage beginning to speculate whether global demand reached a peak in 2019 from where it will begin to decline. Going forward we are likely to see a collective change in how we as humans behave and interact with each other. In the latest Covid-19 Report from Rystad Energy, publicly available here, they mentioned some of the changes in preferences and behavior that could create lasting changes in global energy consumption:

- Video conferences to substitute domestic and international business meetings

- Home office accepted to be both convenient and efficient

- Biking to substitute car driving in cities opening up roads exclusively for bikes

- Domestic holidays substituting international

- Preference for domestic services and goods – security of supply back on the agenda

- Preference for online shopping rather than shopping centers

Turning the attention back to the current markets we have two risk events on tap later today. At 14:30 GMT the EIA will publish its “Weekly Petroleum Status Report” while in the US, the FOMC meet to discuss the current economic outlook and will announce its latest decision at 18:00 GMT. This will be followed by Fed Chairman Powell’s statement and press conference where the market will try to figure out what policymakers could do next.

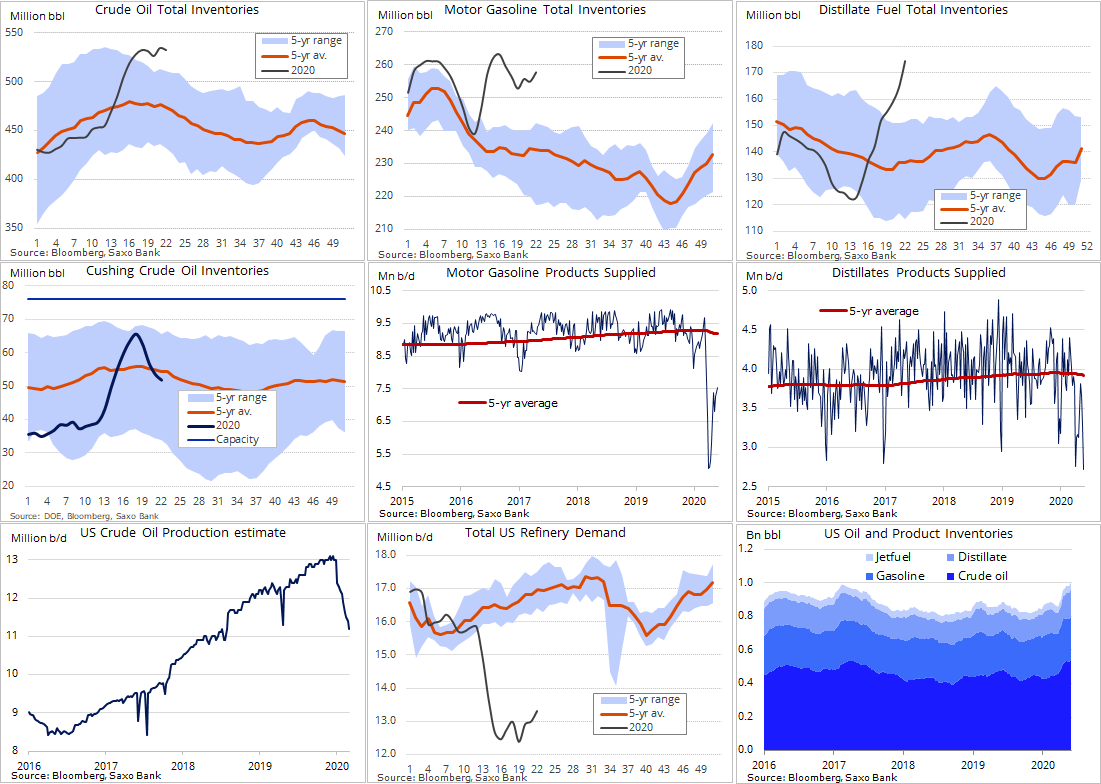

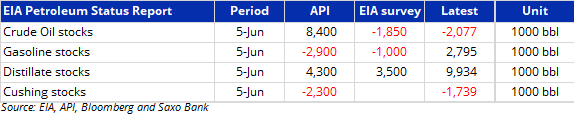

Last night the American Petroleum Institute surprised the market by reporting a 8.4 million barrel rise in US crude oil stocks, thereby contradicting surveys pointing to a near 2 million barrel decline. Something that is highlighting the still uneven and patchy road to rebalancing. Gasoline stocks are expected to fall as demand from motorists continue to improve, while the current Achilles heel, distillates which among other comprises diesel and jet fuel, may see another chart bursting rise to a fresh record.

Demand for products and crude oil production may end up attracting most of the interest in today’s report. Last week distillate supplied, a measure of consumption, collapsed to a 21-year low as demand for diesel and jet fuel remain patchy. Production in response to the recent surge in WTI is expected to find a plateau soon from where it will start to recover. As per usual I will post the result and charts on my Twitter profile @ole_s_hansen.