FX Trading focus: What if FOMC doesn’t really matter?

Of course the FOMC will matter if the FOMC comes out with a decidedly hawkish tilt this evening, but I consider that highly unlikely, even if a few dots on the dot plot could continue to highlight the widening divide in views on the desirable course of Fed policy and the median lift-off time frame could shift forward another quarter with more dispersion in forecasts. Elsewhere, we are likely to get a more hawkish outcome than the market has been looking for in recent weeks on the taper message, though others have convinced me that this is now becoming the consensus view, taking the sting out of the potential for a market reaction to the Fed indicating a desire to get going asap with tapering purchases and possibly even at a relatively rapid pace of 20 billion or more reduction per month. This doesn’t mean we won’t get a market reaction, just that what happens in the wake of tonight’s meeting may have little to do with what Powell and company say and forecast in the accompanying materials, whether marginally more hawkish or significantly more dovish than expected.

That’s because I suspect that the medium term questions that this market is grappling with have little to do with Fed policy at the margin, and far more to do with the course of inflation and massive headwinds for real growth due to snarled supply chains and constraints in the labour market. And more immediately, we have the concern over the US debt ceiling and risk of a US government shutdown and US Congressional brinksmanship that is drawn out until December or even later. Then there are the implications of even an orderly Evergrande wind-up, etc. And as we head into 2022, we will have a US treasury that will need to play catchup on issuance, potentially spiking US yields higher as the Fed is stepping away from its support, while a fiscal “cliff” lies ahead next year if the dysfunctional US Congress can’t put together a significant stimulus package, one that, even if passed, would risk feeding straight into inflation anyway rather than real GDP growth, given the constraints noted above.

Chart: EURUSD

The euro may trade with relatively low beta to the US dollar direction in the wake of tonight’s meeting. If US long yields come a bit unglued and trade sharply higher, however, whether due to what the FOMC brings to the table or because the market is looking forward at other issues from here, the euro and yen could weaken more sharply versus the US dollar than otherwise, trading with high beta to any rise in US treasury yields. Regardless, the level to watch in EURUSD remains the low of 2021 down at 1.1664, a break of which on the close today opens up for a test toward perhaps 1.1500 in the days to weeks to come. Looking lower, a massive level is the 1.1290 area 61.8% Fibo level of the rally wave from the lows early last year to the 1.2350 area high posted in the first week of this year.

GBP struggles despite forward market expectations for the Bank of England at the high of the cycle. The natural gas disruptions in the UK and implications for industry, together with labor shortages may be dampening prospects for significant UK-bound investment save for in existing assets. We have GBPUSD trading rather hard down toward the key 1.3600 area and EURGBP up trading with locally pivotal 0.8600 and above – room for more pain there unless the Bank of England takes a strong stand tomorrow, and really anything they say can’t address the issues plaguing the UK growth potential here.

Weak PLN as EU showdown stakes rise. Yesterday, a high EU court ordered Poland to pay a EUR 500k daily fine for continuing to operate a lignite (low energy, highly polluting, “brown coal”) mine in the far southwest corner of Poland, closer in proximity to Czech and German population centers than any towns of note in Poland and used as feedstock for some 7% of Poland’s power generation. Poland has refused to shut down the mine or pay the fine and is hot under the collar, especially at Czech Republic, which it sees as driving the case to this outcome. It is yet another sign that the country is at odds with the EU on top of other issues like the independence of the judiciary. The zloty is close to the cycle lows versus the Euro and the central bank in Poland is dragging its feet in indicating a willingness to hike rates. If Germany sees a Red-Green government, the outlook for EU recovery fund disbursement to Poland next year and a deepening showdown are dead ahead.

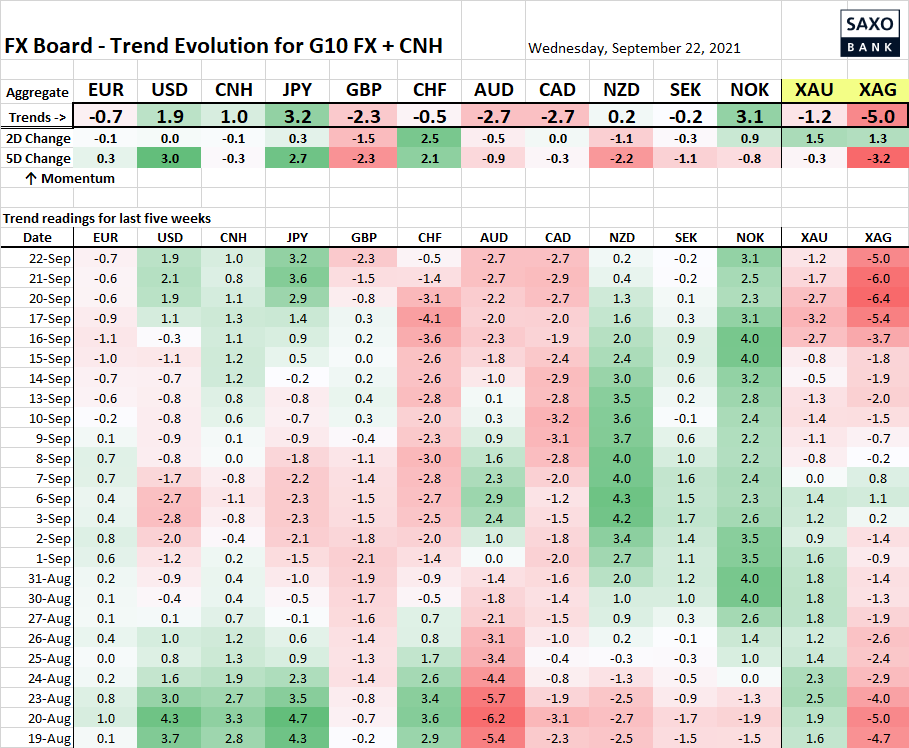

Table: FX Board of G10 and CNH trend evolution and strength

Note sterling really starting to slip in trending terms to outright negative, which could risk deepening if the BoE can’t save the pound tomorrow. Also, the commodity dollars are increasingly in synch, with the kiwi a bit unfairly resilient, given a stumble in rate expectations this week. NOK outperformance at risk tomorrow if the Norges Bank guidance isn’t sufficiently hawkish and risk sentiment doesn’t continue to improve.

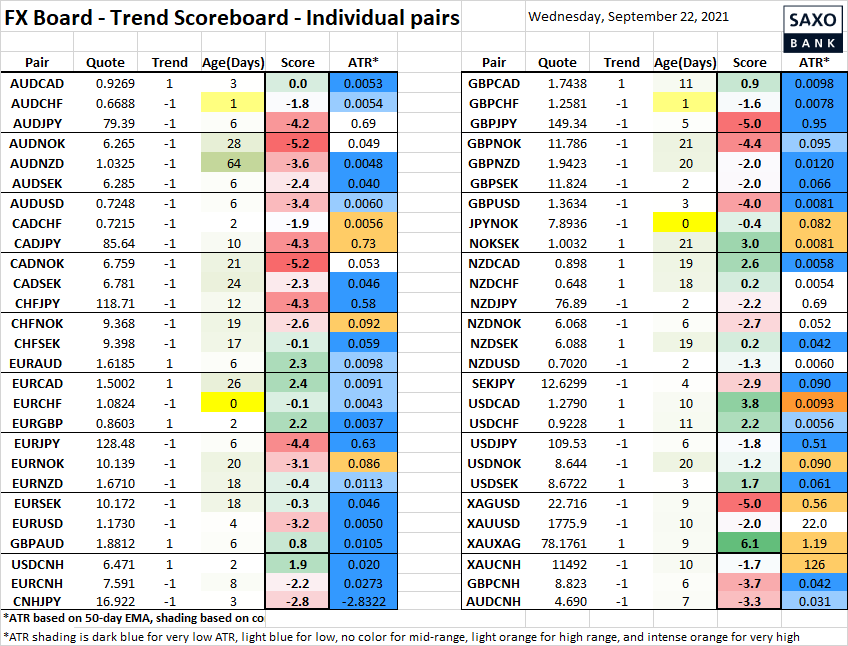

Table: FX Board Trend Scoreboard for individual pairs

EURCHF is tilting back lower after the head-fake and break of all manner of resistance to the upside recently – further confirmation of this reversal needed post-FOMC (CHF sensitive to yield direction). SEK in danger of limping to the weak side if risk sentiment stays wobbly, especially after a very dovish Riksbank – note EURSEK struggling to stay negative.

Upcoming Economic Calendar Highlights (all times GMT)

- 1400 – US Aug. Existing Home Sales

- 1430 – US DoE Weekly Crude Oil and Product Inventories

- 1600 – UK Bank of England’s Woods to speak at Mansion House

- 1800 – US FOMC Meeting

- 1830 – US Fed Chair Powell Press Conference

- 2100 – Brazil Selic Rate Announcement