FX Trading focus: Aussie rates jolt on CPI, UK fall budget statement and Bank of Canada dead ahead

The Aussie traded a bit firmer overnight after the release of the Q3 Australia CPI data. The headline numbers were +0.8% QoQ and +3.0% YoY versus +0.8%/3.1% expected, respectively, but the “Trimmed Mean” received more attention as it came in at +0.7% QoQ and +2.1% YoY vs. +0.5%/+1.8% expected. Interestingly, while rates reacted violently to this development – sending terminal 2022 expected rates more than 25 basis points higher, the Aussie reaction was muted – sticking a bit higher versus the weakest G10, but sharply lower this morning again from overnight highs versus the US dollar and especially the Japanese yen.

It is a very loud grinding of the gears for an analyst to see a move like that overnight and to see AUDJPY tumbling sharply this morning after such an adjustment to the RBA expectations curve. Metals prices dropping of late and extending lower still overnight, not to mention a partial collapse in Chinese thermal coal prices after a recent major spike, may be contributing factors, just as declining long yields this morning are putting some overdue pep in the yen’s step as the last sell-off over-reached relative to developments in global fixed income. As well, we have end of month coming up on Friday after a historically bad month for the JPY and a Bank of Japan meeting tonight, so some of this is likely simply an adjustment of near-term stretched positioning and a dose of rebalancing. Nonetheless, it is a remarkable development and we’ll have to see how the price action picks up on the first of the month on Monday to see in hindsight whether this is a one off consolidation. For now, the lid remains on AUDUSD as long as recent highs to the 0.7600 area hold as well.

UK Fall Budget Statement up today. I have covered this in my previous update, but the general outlines here are that Chancellor Sunak is looking to cut outlays wherever he can while announcing a flurry of measures that nonetheless don’t add up to much. The fiscal deceleration could weigh on sterling from here, and expectations of a Bank of England rate hike at next Thursday’s Bank of England meeting have pulled back a tad further – now just barely above 50/50 odds of a move. Watching 1.3650-1.3600 as the key pivot zone that divides a simple “further consolidation” scenario from the risk of a new rout back to the lows of the cycle. GBPJPY, given the above, may prove higher beta this week to sterling direction, given the comments above.

Chart: AUDJPY

Despite the Q3 Australian CPI overnight triggering a major repricing of even 2022 rate expectations from the RBA (25 bps higher by end of next year relative to before the release), the Australian dollar was unable to hold its rally overnight and was especially weak this morning against a resurgent Japanese yen, which has likely risen on the factors mentioned above. Plenty more room for a sharp consolidation into month-end if safe haven yields push lower still, but given the scale of the recent JPY sell-off, it would take some doing to reverse this recent rally, perhaps a move all the way back below the 200-day moving average, currently near 82.65.

Bank of Canada meeting later today. This meeting will feature a new set of forecasts for the economy, including inflation, and a press conference with Governor Macklem. No rate hike expected as the guidance at the previous meeting repeated the July policy assessment, which anticipated that the Canadian economy still has significant excess capacity and that the time frame for hiking rates won’t arrive until the second half of next year. But the time frame of the rate hike guidance could be pulled forward (hawkish) with the market already predicting a hike as early as the March or April meeting, so a repeat of the “second half of 2022” time frame would be nominally dovish. CAD is soft ahead of the meeting.

Significant Brazil rate hike anticipated tonight – The exploding Brazilian budget deficit on new welfare spending initiatives, likely not coincidentally ahead of an election set for October of next year, together with much higher than expected inflation (October CPI reported at over 10% year-on-year) has the market anticipating a large rate hike of some 150 basis points to take the Selic rate to 7.75%. The Brazilian real has weakened toward the range high this year in USDBRL near 5.80 before a slight strengthening as the Brazilian Central Bank is under pressure to defend the value of the currency. At the same time the political situation is getting toxic as president Bolsonaro has vowed that “only God can take me from presidency” and a number of Senators are trying to indict the president on charges of crimes linked to his handling of the pandemic even one for “crimes against humanity”.

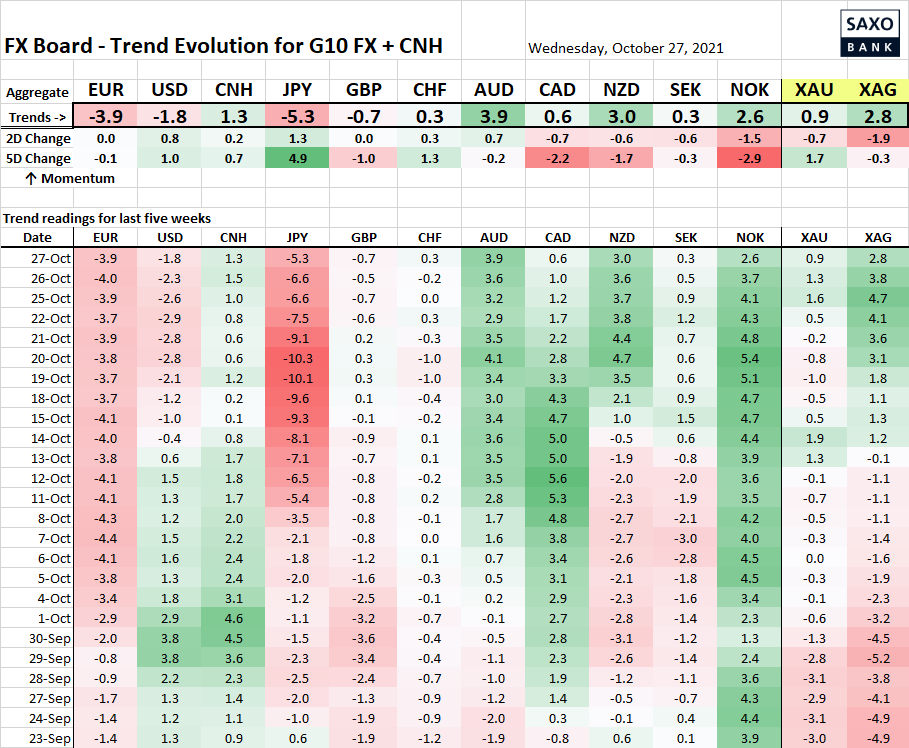

Table: FX Board of G10 and CNH trend evolution and strength

The momentum shift in the JPY is extreme over the last five days – perhaps not a surprise given the incredible pace of its recent weakness. Note the US dollar trying to make a stand here, while the Euro remains in the doldrums.

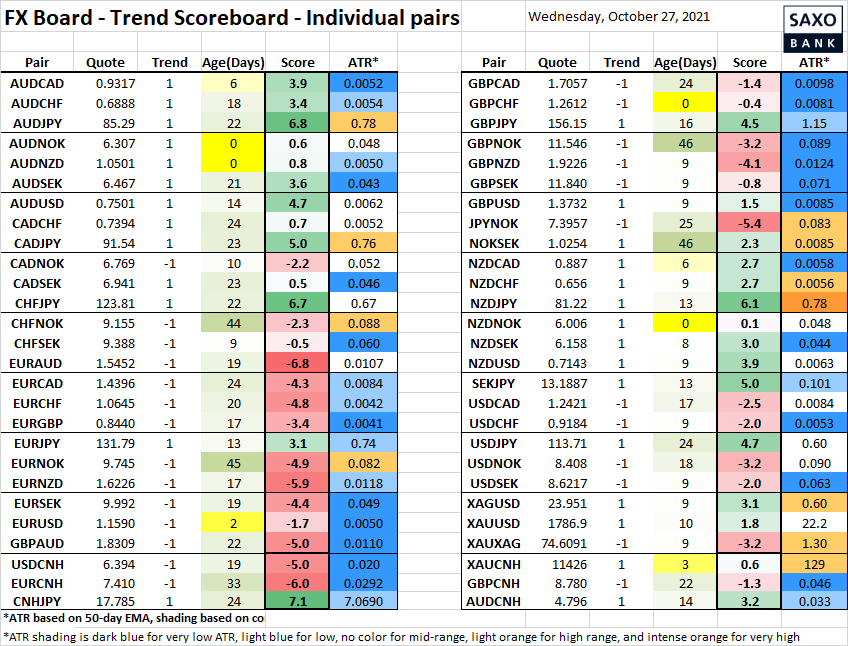

Table: FX Board Trend Scoreboard for individual pairs

EURUSD is tilting back lower, GBPUSD would only threaten a flip lower on a move and hold well south of 1.3700 into next week beyond today’s budget statement. AUDNZD trying to make noise with a flip back higher, but is perhaps too embedded in the range to trust at the moment.

Upcoming Economic Calendar Highlights (all times GMT)

- 1130 – UK Chancellor Sunak to deliver Budget Statement

- 1230 – US Sep. Advance Goods Trade Balance

- 1230 – US Sep. Preliminary Durable Goods Orders

- 1400 – Canada Bank of Canada Rate Decision

- 1430 – US Weekly DoE Crude Oil and Product Inventories

- 1500 – Canada Bank of Canada Governor Macklem Press Conference

- 2130 – Brazil Selic Rate Announcement

- 2340 – Australia RBA speakers Debelle, Bullock

- 2350 – Japan Sep. Retail Sales

- Japan Bank of Japan Meeting