FX Trading focus: Bank of England fails to clear hawkish surprise, JPY crosses peaked?

The Bank of England meeting produce an upgrade to the 2021 GDP forecast and the admission that inflation could rise above 3% in the near term, but the position that inflation will likely prove transitory and the lack of any shift in the guidance on asset purchases deflated the mild buildup of hawkish expectations and took sterling back lower in the wake of the meeting, as it is clear we’ll need to wait for more incoming data to get a more notable adjustment in the bank’s guidance.

Chart: GBPUSD

Sterling is consolidating sharply lower as not only did the Bank of England not wax particularly hawkish, it more or less declared itself in wait and see mode for now, with potentially more drama to come at the August meeting if UK numbers continue to pick up from here and the Delta variant of Covid scare fades. Rate hike expectations for mid-2022 have been downgraded a few notches and the wind is coming out of sterling’s sails, while the strong USD move is trying to stick after the very sharp rally post-FOMC was partially unwound until yesterday’s turnaround. The next level of import besides the 1.3707 pivot low is the range low of 1.3670, toward which the 200-day moving average is also crawling higher.

JPY crosses peaked? I noted yesterday that it was difficult to cheer on dramatic new highs in USDJPY unless long US yields were to rise back towards the highs of the cycle. Today I would add that this includes JPY crosses in general. And while US 10- and 30-year yields have bounced, they’re far from the cycle highs. A bit more discussion on interpreting long US yields shrugging off the FOMC meeting last week below. For now, like USD pairs yesterday, JPY pairs have pivoted slightly today after their sharp bound this week that erased half or more of the JPY rally late last week. Looks pivotal, and I lean for the potential for another wave of JPY strength here, but

Long US yields – what gives? It is interesting to observe analysts’ wildly diverging interpretation of the reasons behind long US yields actually dropping for a time in the wake of the FOMC last week, a development so different from the “taper tantrum” experience of 2013, when Bernanke’s mere suggestion that tapering would one day be needed triggered a massive rout in treasuries and a wipeout in EM currencies. This time around yields have settled out to more or less flat, while EM currencies have consolidated a bit lower, but have been trying to make a comeback this week while the sun of very low volatility (especially in EM credit spreads) continues to shine.

The explanations run from those we have included in recent days:

- That there is some market dysfunction caused by the Treasury’s running down of its general account that is generating a huge demand for treasuries due to all of the liquidity forced on banks. I.e., the price discovery is partially or entirely non-existent until we get back to more normal market circumstances, possibly around August 1, the Treasury’s target date for completing its shifting of funds.

- A “sign of health” according to the more optimistic of two scenarios presented in a recent column by the WSJ’s Fed reporter Jon Hilsenrath, who thinks that it could be because the market now knows what tapering looks like after trying it in the last cycle and that the treasury market has had a head start in having anticipated the Fed shift as rates rose off their lows from latelast year.

- A sign that the Fed can never achieve notable lift-off or normalize rates. This would be the view of deflationistas like SocGen’s Albert Edwards, whose latest piece hit my inbox today and is titled “The Fed’s amibitions to normalize rates can never be achieved”. Oh dear…. Some support for at least tilting toward this idea if not wholly endorsing it is the shape of reaction in Fed expectations since the FOMC that we have pointed out in recent days: the fact that 4-5 year Fed expectations actually dropped even as the nearer term expectations for 2022 and 2023 rose.

Tomorrow’s May US PCE inflation data point is the next key test for USD pairs on the themes off the back of the FOMC meeting. Can’t help but get a bit worried about another weekly initial jobless claims print coming in above 400k today – that’s not how this recovery is supposed to shape up.

Czech Republic hikes – EURCZK punches back to cycle lows. The Czech central bank hiked 25 bps to take the policy rate to 50 bps as expected, with one hawkish dissenter wanting more and the Governor Rusnok saying he couldn’t rule out a hike at all of the four meetings for the balance of the year. CZK was sharply higher yesterday, but has unwound a good portion of the move today after EURCZK punched toward the cycle lows yesterday.

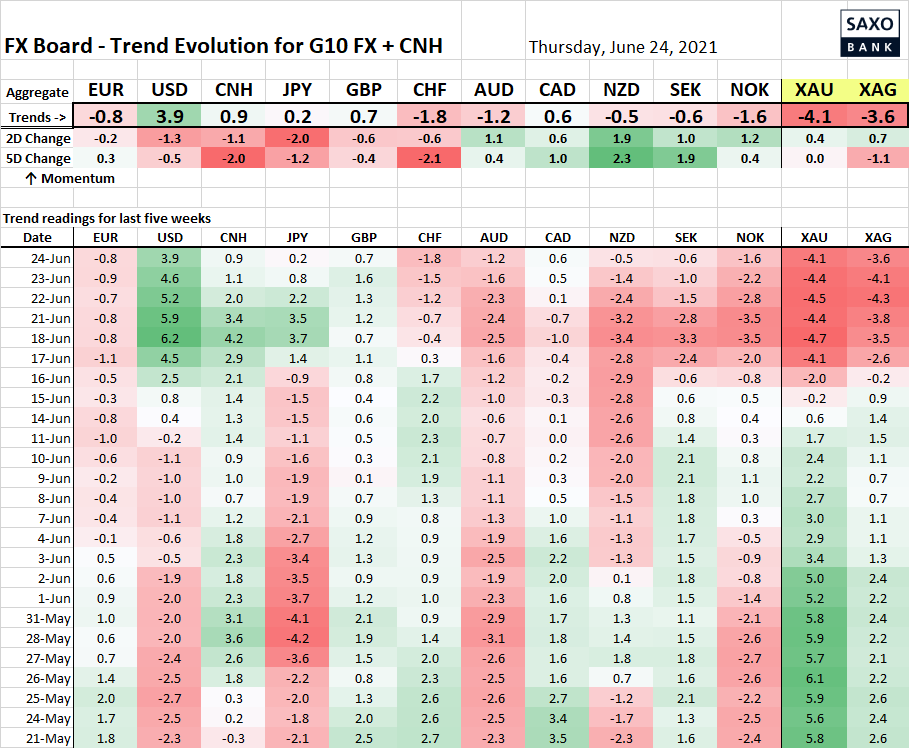

Table: FX Board of G10 and CNH trend evolution and strength.

The USD move off the back of the FOMC is still there, but fading fast unless it gets new life in the coming session or two. Almost everything else very muddled and low energy.

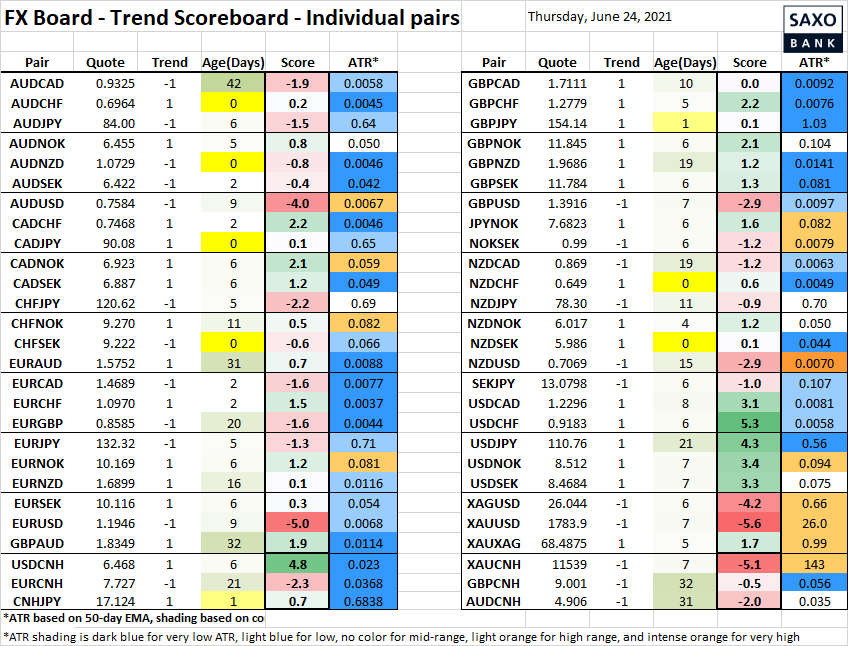

Table: FX Board Trend Scoreboard for individual pairs

In the individual pairs, the JPY crosses are beginning to flip back higher if the JPY doesn’t take a stand as noted above, while NZD is trying to get bouncy again.

Upcoming Economic Calendar Highlights (all times GMT)

- 1500 – US Jun. Kansas City Fed

- 1500 – US Fed’s Williams (voter) to speak

- 1700 – US Fed’s Bullard (non-voter) to speak

- 1700 – US Fed’s Kaplan (non-voter) to speak

- 1800 – Mexico Central Bank Rate Announcement

- 2000 – US Fed’s Barkin (voter) to speak