FX Trading focus: JPY pushing on big levels. Clouds over the kiwi

This week started with the yen bolting out of the gates as it seemed to absorb the further drop in US yields from Friday in the Monday session yesterday. While USDJPY has lurched into a notable reversal after teasing back higher toward 111.00, the more interesting technical developments are to be found in the crosses like EURJPY, where the 200-day moving average gave way for the first time since June of last year and even slightly below the lows since March, while a classic risk proxy like AUDJPY has shown a similar movement, having broken its 200-day moving average back in July and finding resistance there recently before the acceleration lower yesterday that also sees it testing the lows since the beginning of this year. The next major levels are 127.00-50 in EURJPY (very well defined zone) and 78.00-78.50 in AUDJPY if we are to see a more profound breakdown here. Some time back I opined that the JPY was getting insufficient respect on its “real yield” credibility relative to most of the rest of the world, and this idea seems to be playing out, although there is a clear and simple correlation with generally falling nominal yields as well. A dose of proper weak risk sentiment – something we have only really experienced in little single-day or single-week bursts over the past few months, could even accelerate the move precipitously for the JPY, with the USD more-than-likely showing directional sympathy in such an event.

Chart: EURJPY

JPY crosses have lurched into a new sell-off to kick off this week and we have EURJPY testing the lows since a January-February as the market seems to have given up on the idea that EU yields can ever rise meaningfully and the real-yield differential weighs hard on the euro in relative terms, given how high this pair has risen from the 115-120 zone before and shortly after the pandemic outbreak to the highs above 134.00 in early June, actually almost two weeks after German Bund yields toyed with the idea that a 0% yield for ten-year German paper was a conceivable. Now that latter yield has dropped to a sorry -49 basis points (actually a couple of basis points above the lows from earlier this month). From here, it is worth watching the 127.00-50 area for whether a more profound breakdown is set to unfold and to watch how the German election shapes up – the team will have more on that latter subject shortly.

NZD knocked down on lockdown from single Covid case

The New Zealand government has taken the extreme measure of locking down the entire nation for three days and the largest city Auckland and a nearby area for at least a full week due to the discovery of a single Covid case from “community” spread, i.e., not a traveler who was isolated before contact with the rest of the population. The traveler apparently was infectious as far back as last Thursday and had traveled a bit between Auckland and Coromandel some distance to the east and stopped in at least 23 locations. This was the first community spread case since February. The temptation previously might have been to think that New Zealand can quickly get on top of this outbreak as it has previously done with its extreme tracking and lockdown approach and its geographic isolation, but the Delta variant (not yet known whether this was a delta case) is a different beast, as recent experience elsewhere has shown, and NZ has been resting on its laurels with a total vaccination rate of only some 20%, the lowest of any advanced economy. The timing is impossibly difficult for NZD longs, which were sent through a very small exit overnight as we all ponder how the RBNZ treats this. Do they suspend any plans to hike until more is known (will take at least a few days to find whether/how many new cases are out there) or go ahead and hike and make the future course of policy contingent on the virus not impacting the economy beyond the shortest of time frames. I think it is bad optics to hike now and would expect a statement saying that the previous set of market expectations seemed appropriate, provided there is no extended lockdown and this outbreak quickly fades between now and well before the next meeting, but there are arguments in either direction – safe to say that the guidance will be secondary to the actual news in the coming days, even if there will be a further kneejerk on tonight’s announcement. Helmets on!

“Weak” US Empire manufacturing – this one is undeserving of the adjectives in the headlines, after the absurd and unsustainable all-time high of 43 (everything above 0 is an improvement) in July yielded to a reading still above 18, historically a quite positive reading. Remember that diffusion surveys are comparative. On that note, the more interesting bit of data in this survey was the “prices received” index throwing off a reading of 46, the fourth record high in five months and suggesting that producers are able to pass along higher prices to some degree (prices paid was an even higher 76.1, dipping slightly again after posting the highest ever 83.5 in May.

US Jul. Retail Sales up next today – and are a more easy-to-gauge measure of consumer confidence and activity on the ground than the various surveys, including the shocker of a preliminary University of Michigan sentiment reading on Friday. But keep in mind that the latter was for the first part of August, which brought with the mounting concern on the delta variant outbreak and the Afghanistan debacle – two issues which might – might! – fade quickly. In any case, a slight month-on-month dip in July Retail Sales is expected, which is still pretty respectable given the June surge in sales.

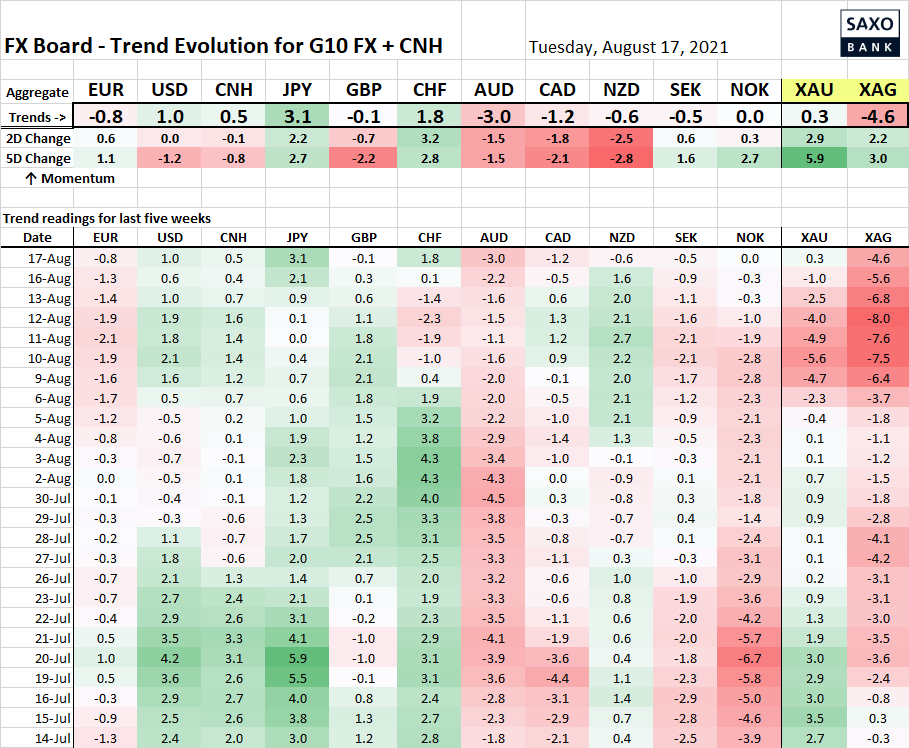

Table: FX Board of G10 and CNH trend evolution and strength

The trend evolution picture reflects what is written above: a significant surge in the JPY and a solidly established trend there in many crosses (see below) while the NZD has lost massive altitude over the last session and the CHF is showing a momentum shift in sympathy with the JPY move. The Aussie remains relatively weak after the RBA minutes underlined the central bank’s commitment to further measures should the Covid outbreaks cloud the outlook.

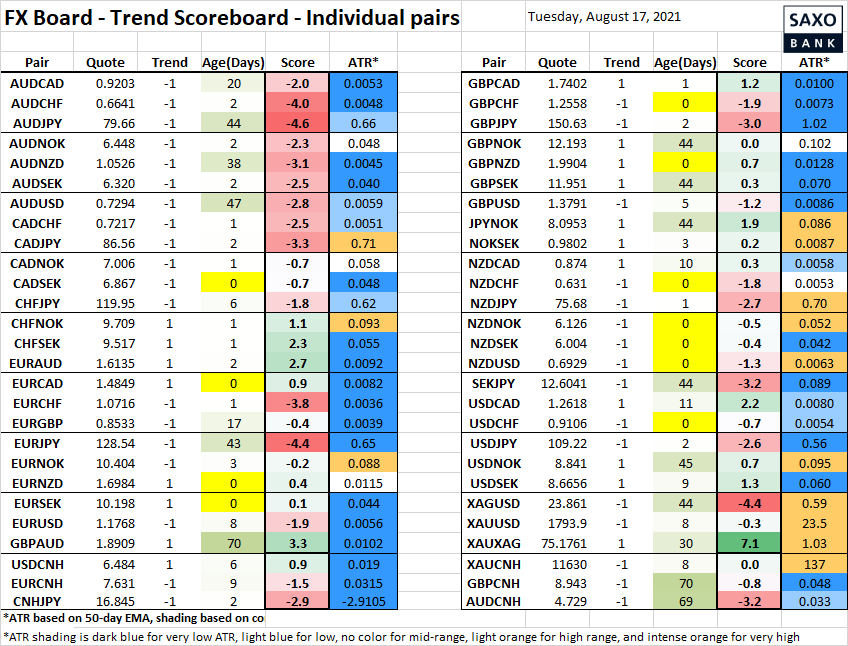

Table: FX Board Trend Scoreboard for individual pairs

The low volatility is nearly everywhere in evidence outside of precious metals and a few random pairs, but note the length of the JPY trend in places like AUDJPY (44 days since the flip to negative) and similar elsewhere, although the bad sterling stumble after its recent strong rise has caught GBP longs offside in recent days, with GBPJPY flipping negative on Friday and GBPUSD doing so a week ago after its run on 1.4000 and subsequent choppy retreat.

Upcoming Economic Calendar Highlights (all times GMT)

- 1215 – Canada Jul. Housing Starts

- 1230 – US Jul. Retail Sales

- 1315 – US Jul. Industrial Production and Capacity Utilization

- 1400 – US Aug. NAHB Housing Market Index

- 1730 – US Fed Chair Powell Town Hall Discussion with Educators

- 1945 – US Fed’s Kashkari (non-voter) to speak

- 0130 – Australia Q2 Wage Price Index

- 0200 – New Zealand RBNZ Official Cash Rate announcement