FX Trading focus: Risk sentiment correlations dominate as inflation data largely shrugged off

A weak August US CPI print yesterday, with the core month-on-month cooling all the way to +0.1% vs. +0.3% expected, should have triggered a weaker US dollar and driven at least a modest rise in risk sentiment on the implications for Fed policy if the market was heavily anticipating this release. Instead, while we got a brief knee-jerk reaction in that direction, risk sentiment weakened anew in and the USD and especially the JPY rose as US treasuries rallied. That suggests that the market wasn’t particularly invested in the implications of this release and the evidence elsewhere suggests that inflation is less on the brain than other factors. In Sweden yesterday, for example, a very hot August inflation print failed to sustain the SEK rally (importantly as EURSEK 200-day moving average was tested yesterday) despite that number and the highest anticipation of the Riksbank eventually moving to hike rates for the cycle, once risk sentiment weakened later in the day. SEK defaulting to quickly to reacting to a still fairly modest swing in risk sentiment is a fairly feeble performance.

Likewise this morning, where the hottest UK inflation level in over nine years (3.2% year-on-year and 3.1% for core year-on-year) failed to reverse any of yesterday’s reversal in sterling from strength to weakness noted in the GBPJPY chart below.

One day of risk off does not a new trend make, but yesterday’s action requires a nimble stance on the potential for a deepening rout in risk-correlated trades if US data, concern about the implications of Chinese policy moves (note Evergrande behemoth moving toward a more official restructuring) and/or options expiries into Friday in the US could mean volatility remains high here at least in the near term.

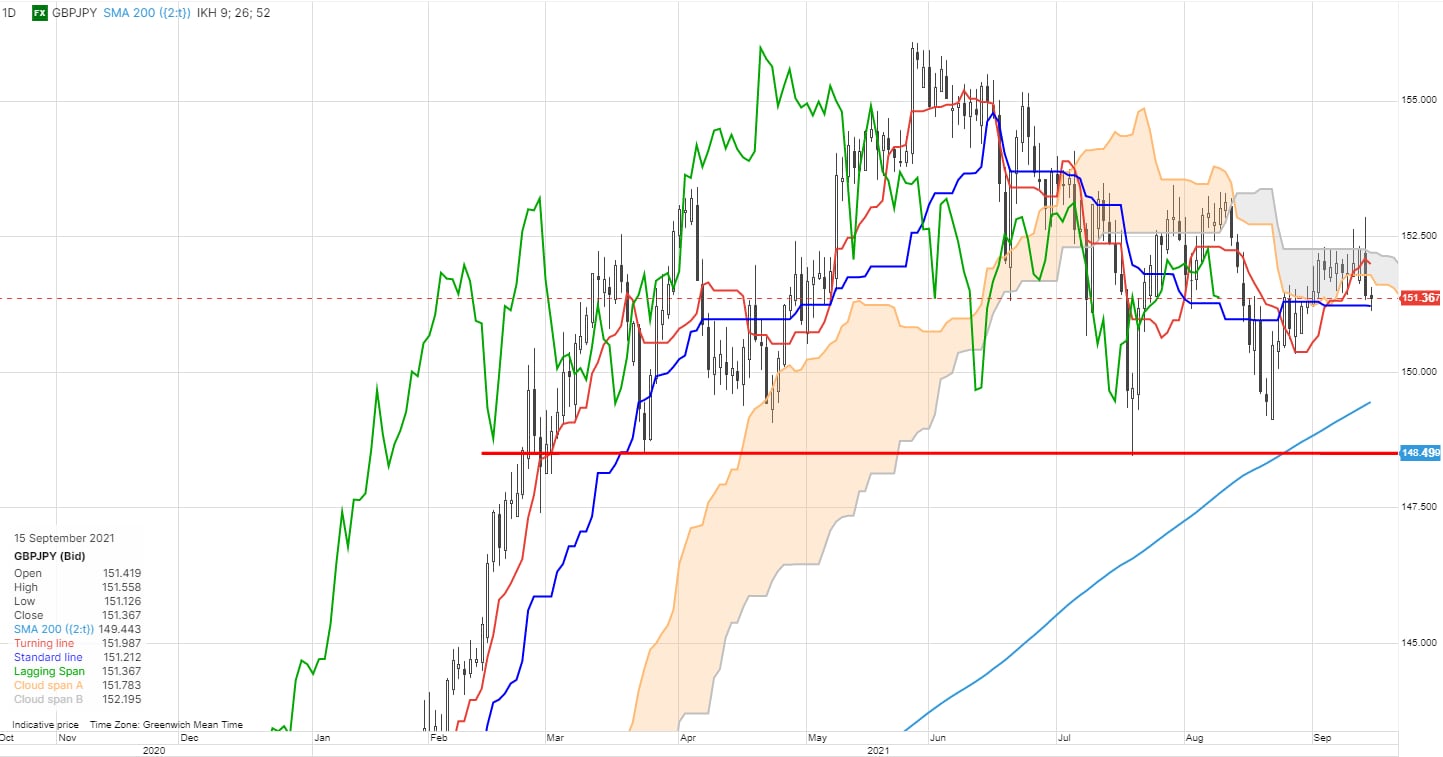

Chart: GBJPY

One of the more interesting technical developments yesterday was in GBPJPY, which went from poking toward a break-out above the Ichimoku cloud that has clearly provided resistance of late and to new 1-month highs to a vicious reversal back lower as US treasury yields dropped in the wake of the US CPI release and the JPY rallied smartly amidst generalize weak risk sentiment. Will have to see how the situation develops further from here – particularly for the JPY around the upcoming Japanese election, but the structure of the chart is rather compelling if the price action bites lower, especially if the neckline-like area of the significant head and shoulders formation comes into view below the 200-day moving average (currently 149.50). The neckline is a bit poorly defined but is at around 148.50 at the lowest. JPY traders should always have one eye on USDJPY as well, where a break of the 109.00 area could generate considerable volatility across JPY crosses.

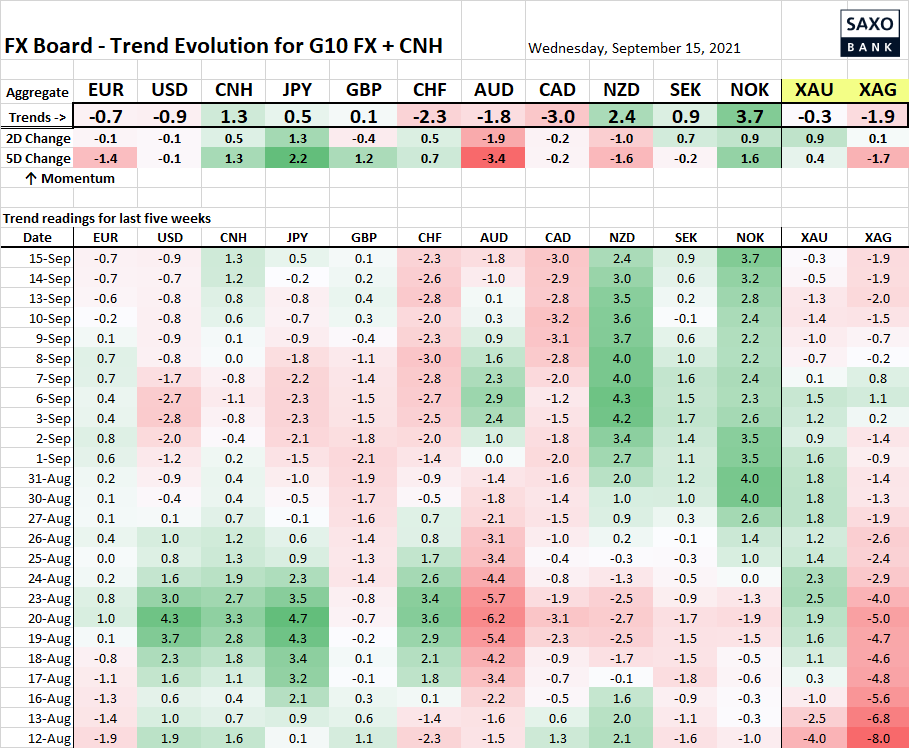

Table: FX Board of G10 and CNH trend evolution and strength

CAD is limping despite high oil prices and ahead of today’s Canada CPI data, quite a contrast with NOK, which is coming back bid in the wake of the Norwegian election and despite yesterday’s wobble. Note the firm CNH as banks have been told that Evergrande won’t pay interest on debt next week.

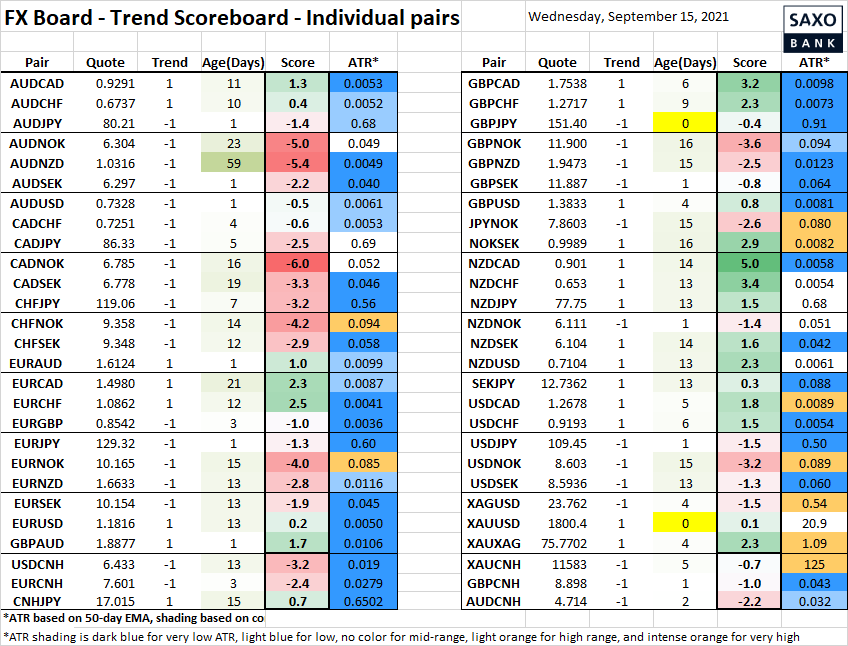

Table: FX Board Trend Scoreboard for individual pairs

Sterling pairs yesterday went from tilting into breakouts to the upside to rather significant bearish rejections, in the case GBPUSD and GBPJPY. Gold is trying to flip higher for the umpteenth time, but needs to break chart resistance to signal interest – just as EURUSD needs to close significantly lower, at least below 1.1750, to signify fresh downside pressure.

Upcoming Economic Calendar Highlights (all times GMT)

- 0900 – Euro Zone Jul. Industrial Production

- 1230 – ECB’s Schnabel to speak

- 1230 – US Sep. Empire Manufacturing

- 1230 – US Aug. Import Price Index

- 1230 – Canada Aug. CPI

- 1300 – Canada Aug. Existing Home Sales

- 1315 – US Aug. Industrial Production / Capacity Utilization

- 1500 – ECB’s Lane to speak

- 2245 – New Zealand Q2 GDP

- 2350 – Japan Aug. Trade Balance

- 0130 – Australia RBA Bulletin

- 0130 – Australia Aug. Unemployment Rate / Employment Change