FX Trading focus: Market brushes off fairly hawkish FOMC. Only eyes for Evergrande?

The FOMC meeting yesterday – or at least the Fed Chair Powell press conference – proved somewhat hawkish relative to expectations. The new FOMC policy statement contained very few changes, the chief one being a hint at the coming taper that has long been expected: “if progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted.”

Elsewhere, the new Fed projections showed two more Fed forecasters (and now nine versus seven in June and therefore fully half of forecasters) pulling their forecast for rate lift-off into 2022. In the economic forecasts, core PCE inflation forecasts were raised 0.2% for 2022 and 0.1% in 2023 to 2.3% and 2.2% respectively, while the unemployment rate forecasts for next year and 2023 were left unchanged (3.5% projected for 2023 and initiated at 3.5% for 2024). This combination saw the US dollar knee-jerking slightly lower and the rate outlook largely unchanged, like chiefly due to the lack of a shift in the unemployment rate forecast, as full employment and signs of a wage/price spiral initiating are seen as key for initiating actual rate hikes.

But it was Fed Chair Powell’s press conference that saw the more hawkish developments as Powell indicated more explicitly that he and many on the Fed are ready to start tapering soon and that it makes sense to complete the taper by the middle of next year, with the pace determined by incoming data. By the end of the press conference, rate expectations had edged some few basis points higher for the Fed funds rate by the end of 2022.

Only eyes for Evergrande for the moment? In the reaction to the above, the USD managed to pull a bit higher and EURUSD traded solidly below 1.1700, etc.. until the news flow overnight and especially in the European session seems to suggest that for the very short term, the market finds the Evergrande story more of a distraction, with a seeming celebration in late Asia and early Europe on a Chinese liquidity injections and the announcement that China told Evergrande to avoid defaulting on near-term USD bonds. Later in the session, we have seen a wobble as China is apparently telling local governments to be ready in the event of an Evergrande fail, and as of this writing, holders of Evergrande’s USD debt have yet to be paid their coupons due today. (a Bloomberg article indicates that covenants allow 30 days delay from the coupon due date before a default is declared.)

Euro Zone and UK flash September PMIs were disappointing today. Markets are holding breath for German elections on Monday, with an interesting vote to be held in Berlin on Sunday which has been dubbed an “expropriation referendum”, as the city’s voters will decide whether to enact an even more widespread effort to force the largest apartment-owners, companies that snapped up formerly state-owned apartments in the 90’s and early 2000’s, to sell these apartments back to the city to provide affordable housing.

Chart: EURGBP

An interesting test of sterling sentiment today as the prior drumbeat of rate expectations ratcheting higher generally failed to support sterling ahead of today’s BoE meeting, which further raised the anticipation for BoE rate hikes early next year. EURGBP recently traded toward key cycle resistance in EURGBP just above 0.8600 before today’s meeting. The BoE was about as hawkish as conceivable (see more below), but is central bank policy relevant to the structural issues that are plaguing the UK right now? In any case, today’s closing levels look important for whether the pair can maintain the range below 0.8600, with the 0.8500 area pivot the next area of interest.

Bank of England. The Bank of England meeting today was sufficiently hawkish to bring further forward the anticipated lift-off date to as early as late Q1 next year. The recent weeks and even months of rising expectations have done little to support sterling even if it is trying to piece together a solid rally on today’s meeting. The vote on rates was unanimous but 7-2 on keeping the asset purchase target unchanged. The forecast of slightly higher inflation with slightly lower growth this year underlines the central bank’s futility – supply side constraints that it can do nothing about, including labour shortages and the risk of a spiraling natural gas debacle if supplies aren’t secured a t a reasonable cost this winter. Let’s see where GBP closes today – would like to suspend judgment, given that rising rate expectations have thoroughly failed to support the pound recently. As well, an interesting test for the economy lies ahead, with the furlough scheme enacted during the pandemic set to expire this month: arguably, tightening rates does no good if growth continues to stumble and wages fail to match inflation trends. Sterling could prove more sensitive to labour market data from here.

Norges Bank achieved lift-off as expected today with a rate hike of 25 basis points and indicated a bias to hike again in December. Norwegian rate expectations took off further only to fade a bit later in the session, while EURNOK managed local new lows below 10.10 and likely needing a full recovery in risk sentiment (most of the way there in Europe if still rather far from it in the US) as well as new highs for the cycle in Brent crude oil to punch down to the massive 10.00 level and beyond.

Turkey cut 100 bps, surprising consensus. The signals where there from the Turkish central bank’s new leadership that it was looking for an excuse to cut rates by focusing on the lower core inflation levels rather than the headline inflation rate which was still slightly above the 19% policy rate. But hardly anyone, including myself, dared believe that they would actually cut rates today. But cut they did, and by 100 bps and the TRY was immediately slammed for steep losses. This could get messy as the country’s political leadership ones again wades into the situation.

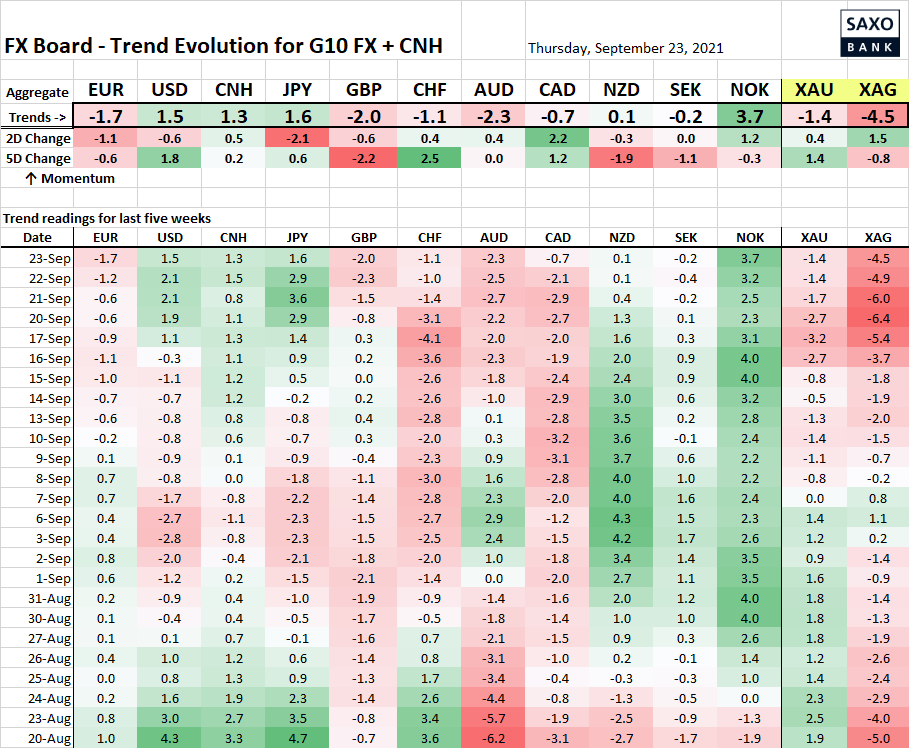

Table: FX Board of G10 and CNH trend evolution and strength

Sterling is making a stand today after its recent bout of weakness but that will take some time to even show up on the momentum indicators here, NOK upside has extended on today’s Norges Bank.

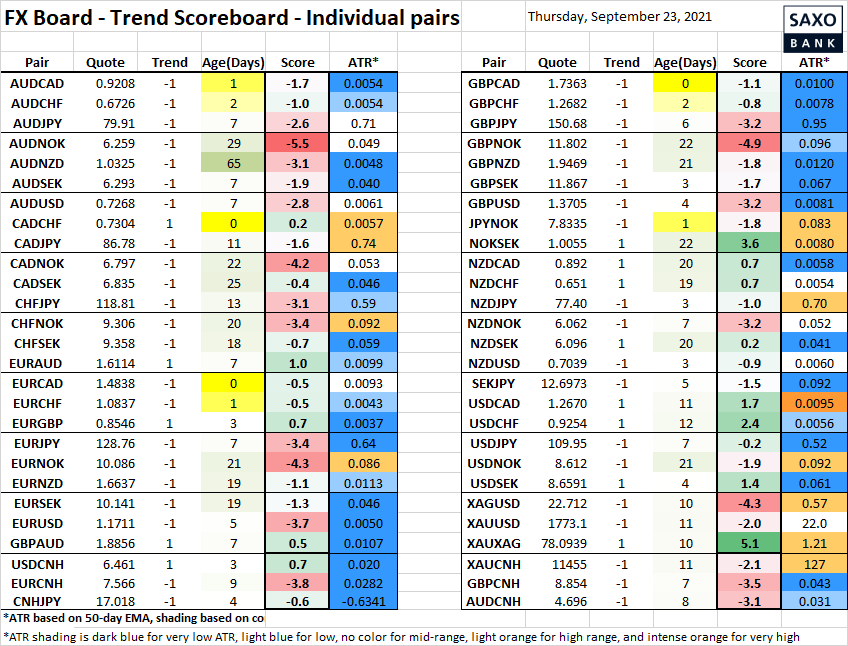

Table: FX Board Trend Scoreboard for individual pairs

Presented below without comment – plenty of trending questions in flux here.

Upcoming Economic Calendar Highlights (all times GMT)

- 1230 – US Aug. Chicago Fed National Activity Index

- 1230 – US Weekly Initial Jobless Claims

- 1230 – Canada Jul. Retail Sales

- 1345 – US Sep. Flash Markit PMI

- 2245 – New Zealand Aug. Trade Balance

- 2330 – Japan Aug. National CPI 1830 – US Fed Chair Powell Press Conference

- 2100 – Brazil Selic Rate Announcement