FX Trading focus: FOMC preview: easy to clear bar of surprise, especially for EM?

In terms of daily closing prices, US treasury yields and Fed rate expectations ironically bottomed out last Thursday, on the very day that the US printed its highest core inflation reading since the early 1990’s (and 3-month annualized since the early 1980’s!). By Friday’s close, yields had picked up a bit and the USD was sharply stronger on the day, a move that looked a bit odd relative to other markets’ rather calm session, and one that hasn’t followed through today. But the firming USD could suggest that the USD bears are a bit wary of the message that the Fed will deliver this Wednesday, even if the equity and treasury markets seem quite comfortable.

Given that strength of recent US data, particularly on inflation but also on signs that the jobs market is being held back by the lack of qualified workers and sufficiently high wage offers relative to public benefits, not by the underlying state of the economy, the Fed will need to roll out more two-way guidance. At minimum, we’ll have to see a more robust mention of eventual asset purchase tapering (surely MBS reduction first), given the huge surge in the size of the Fed’s reverse repo facility making it obvious that the Fed’s treasury purchases aren’t productive. As key Fed members like Clarida have successfully teased the market that a tapering discussion will one day take place without any major market “tantrum” across markets, this may embolden the Fed to given a firmer signal at this meeting.

And then there are the “accompanying materials” that will be published at this meeting, containing the staff economic projections and the policy forecasts, which could speak louder than the statement in delivering or not delivering the message that the Fed’s confidence that this recent inflation spike will blow over because it is transitory.

In terms of market reaction to a more hawkish than expected Fed, I am a bit reluctant to call for serious drama in the wake of the meeting, especially because I am at a loss to see how the excess US dollar liquidity situation changes quickly here, given that the US treasury will likely draw down another $200 billion or so in funds held at the Fed over the coming weeks, adding to liquidity, as it reaches its target of taking the “general account” down under $500 billion by August 1.

The corner of the currency market that has seen the most dynamism is in EM, as the backdrop of risk conditions has been extremely favourable for EM in recent weeks and months (discussed in my latest FX Webinar from June 10 – see down below on the page for the replay link. The EM discussion starts around 34 minutes). We have seen macro developments that are supportive for individual EM countries as well, including South Africa and Mexico achieving current account surpluses (although Mexico’s dipped back to deficit in Q1).

In fact, ZAR has seen the best performance of any major EM currency over the last 12 months at some 28% carry-adjusted versus the US Dollar. But recent price action suggests the long EM trade may be overextended in the strongest performers: Mexico has been unable to sustain new gains below 20.00 after Mexican president AMLO lost at super-majority at the recent election, the platinum rally has fizzled for some time now, reducing support for a very aggressive ZAR move, and the 50-bps hike in Russia on Friday with guidance for more hikes seems to have been fully priced, as USDRUB is actually higher today from Friday’s closing level. 72.60 is an important level for USDRUB.

The two more recent bright spots in EM have been BRL, where the fading pandemic focus has supported BRL from woefully cheap levels, and USDTRY has staged a sharp comeback after it ripped up through the key 8.50 area ten days ago after Turkish president Erdogan commented on the need for rate cuts. He will Erdogan to meet US President Biden today.

If there are to be any fireworks in the USD post-FOMC, they may be most dramatic in EM.

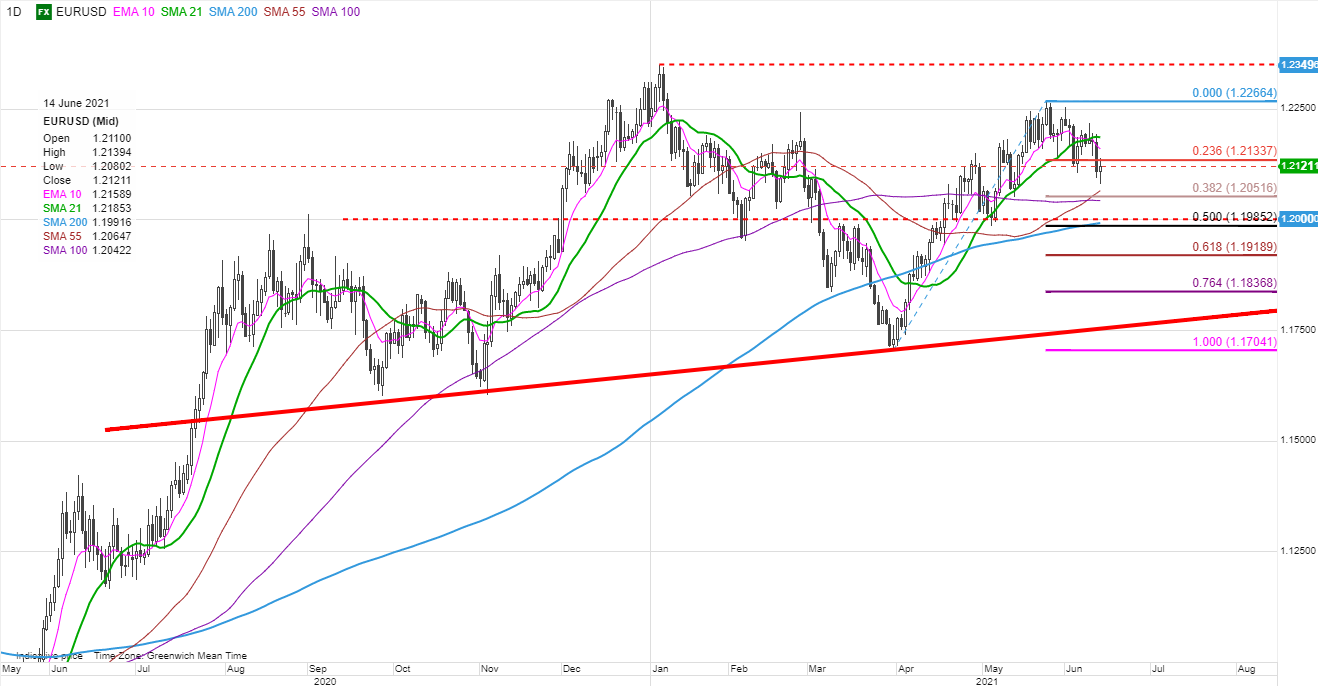

Chart: EURUSD and the 1.2000 level

EURUSD will be one to watch over the FOMC meeting as the excitement in watching EU yields rise has faded and, as we discuss extensively in our upcoming Q3 outlook, as we await key political signals in the wake of the German election. Hard to cook up a huge rise in volatility unless Fed expectations receive a real jolt at Wednesday’s FOMC meeting, but 1.2000 is the key downside pivot area that has been a notable pivot level since February, both as support and resistance, and coincidentally is also near the 200-day moving average. But if the selling goes toward 1.1900, technicians will begin warming up head-and-shoulders discussion in the neckline noted with the thick red line on the chart below. I am reluctant to go there now, but will keep an open mind…

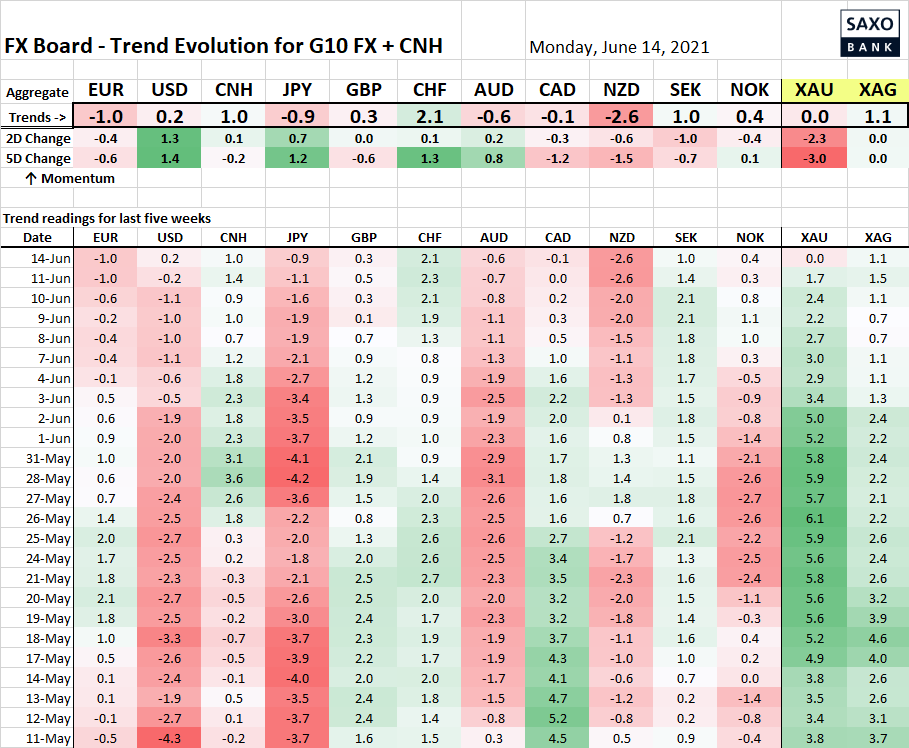

Table: FX Board of G-10+CNH trend evolution and strength

Interesting to watch the SNB this week for any discomfort as CHF has traded back below 1.0900 in EURCHF terms and against the USD is firmly sub-0.9000. NZD downside is notable, but is so far mostly just been about an unwind of the strength on the back of the most recent RBNZ meeting that led nowhere. JPY weakness has unwound and that currency is on a neutral footing in trending terms.

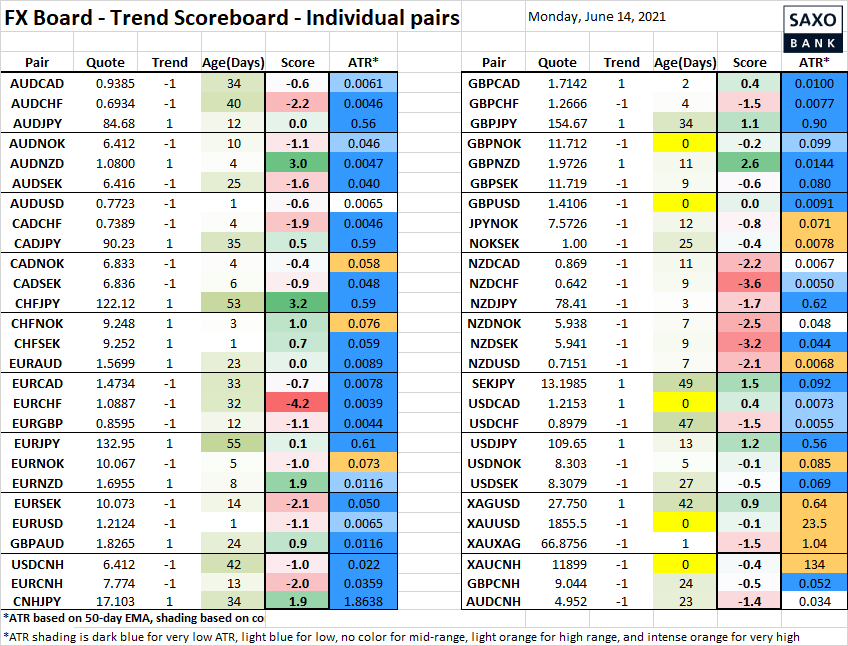

Table: FX Board Trend Scoreboard for individual pairs

The most interesting development in the individual pairs is perhaps USDCAD trying to look at an upside range breakout and the trend moving into positive today on a close near current levels or higher. That and GBPUSD and XAUUSD (spot gold) also pointing to USD strength risk here.

Upcoming Economic Calendar Highlights (all times GMT)

- 1230 – Canada Apr. Manufacturing Sales

- 0130 – Australia RBA Meeting Minutes