FX Trading focus: Scandies on the bid, USD rolls over ahead of CPI release today

The Scandies, NOK and SEK, are both on the move to the upside, the NOK with the support of strong energy prices (particularly natural gas, as discussed in yesterday’s report), but also as the Norwegian election results yesterday largely cleared away any uncertainty over the eventual shape of a majority coalition as the three largest center/center-left parties have a five seat majority and won’t have to seek support from the Red and/or Green parties trying to leverage extreme positions in a difficult minority coalition scenario. The government platform that emerges is unlikely to bring new policy drama that affects the Norges Bank’s hiking intentions or fossil fuel production in the near future.

The latest August Sweden CPI data has administered the Swedish krona a jolt this morning as it came in far hotter than expected, at +0.5%/+2.1% for the headline and +0.5%/+2.4% MoM/YoY for the core, the latter versus +0.2%/+1.9% expected. This has the EURSEK probing below a key support, as noted in the chart discussion below, as the Riksbank will eventually have to respond, and on that note, 2-year Swedish swaps have pulled 1.5 bps higher to their highest level for the year.

Chart: EURSEK

EURSEK is attempting to punch below the 200-day moving average and local support today in the wake of a very hot CPI print, together with stable risk sentiment in Europe that has failed to track the US sell-off. The euro bounce yesterday is an additional support for SEK, as we watch whether this move below the 200-day moving average can hold and set up a run back at the huge 10.00 level that provided support back at the beginning of the year.

US August CPI today – there are four numbers to watch in today’s US CPI release – the headline CPI and “ex food and energy”, or core CPI, for both month-on-month and year-on-year rises. Traders should focus most of their attention on the month-on-month releases. The pickup in core US CPI data in April through June was the most remarkable acceleration in core inflation in decades, but even with the year-on-year core CPI rate very high in July at 4.3%, the “team transitory” observers and economists who believe that inflation will calm again were relieved to see the month-on-month core US CPI print for July plunging to 0.33% after averaging near a stunning 0.8% in Apr-Jun. The August expectations are for core CPI readings of 0.3% month-on-month and 4.2% year-on-year. Besides the US dollar itself, we’ll watch the reaction in the US treasury yield curve, with the most interesting outcome higher US yields that don’t really support the US dollar outside of perhaps USDJPY and perhaps USDCHF. A weak US CPI print would likely prove a more straightforward affair, but US yields could yet head higher nonetheless. Note that EU sovereign yields are on the move higher this morning as well, with the 10-year German Bund inching up toward what I would argue is the pivotal -25 bps level that would really begin to reverse the focus back higher for yields (current -30.5 basis points).

RBA doing all it can to throw Aussie under the bus after Governor Lowe was out overnight voicing disapproval of market bets that the RBA would eventually move to hike rates before the time frame the RBA has forecast, explicitly expressing that “I find it difficult to understand why rate rises are being priced in next year or early 2023.” The RBA wants to be sure that rising wages are a prominent feature of the recovery before updating guidance, but I wonder if the central bank is indulging in a policy mistake. The Q2 housing price change suggest they are, with prices leaping 16.8% year-on-year, the fastest pace of appreciation in the history of the survey since 2004 save for one quarter in 2010. Is it not a given that Australia is fully as post-Covid as it can be within a couple of months of further vaccine roll-out?

Regardless, despite fairly crowded speculative AUD shorts on the US futures exchange (-70.5k contracts – a level only exceeded on a handful of occasions since 2013 and not for long) the Aussie managed to weaken in the crosses again, with AUDNZD etching new local lows and challenging the significant 1.0300 area now. AUDUSD is struggling a bit this morning as well after the coming off the peak of the strong rebound from the 0.7106 low. The 0.7336 level was near the low yesterday and is the 38.2% retracement, and the last important support is the 61.8% retracement at 0.7248.

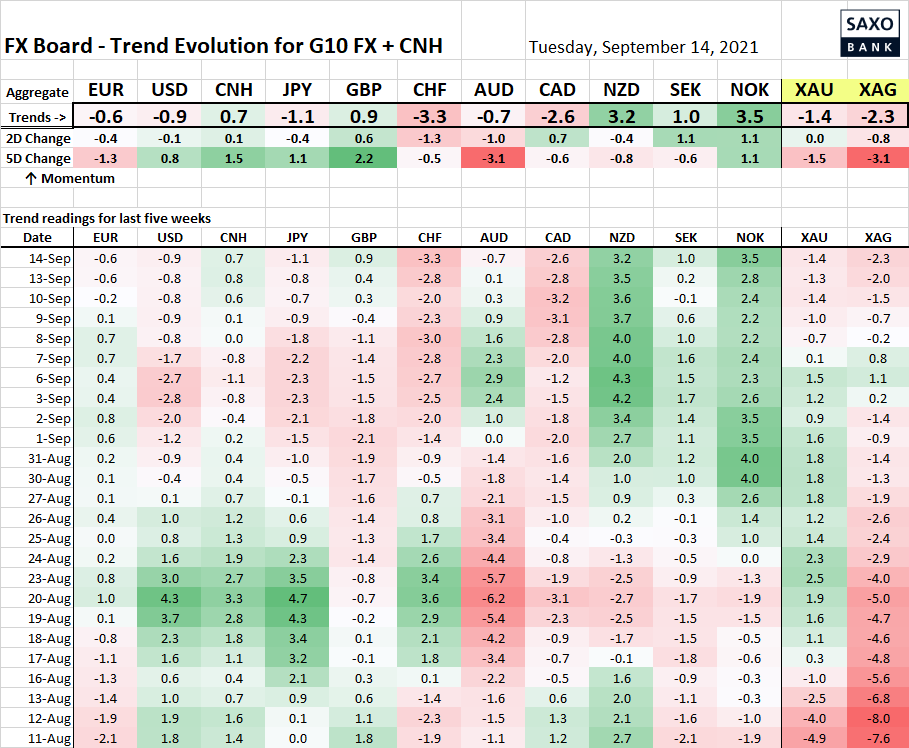

Table: FX Board of G10 and CNH trend evolution and strength

Watching for the SEK to add to the Scandie trending potential to the upside here as we note the momentum shift on today’s Swedish CPI release. Also, will today’s strong UK employment market and earnings data, together with BoE rate expectations near the high of the cycle, help sterling spread its wings again? Note that August UK CPI is up tomorrow morning.

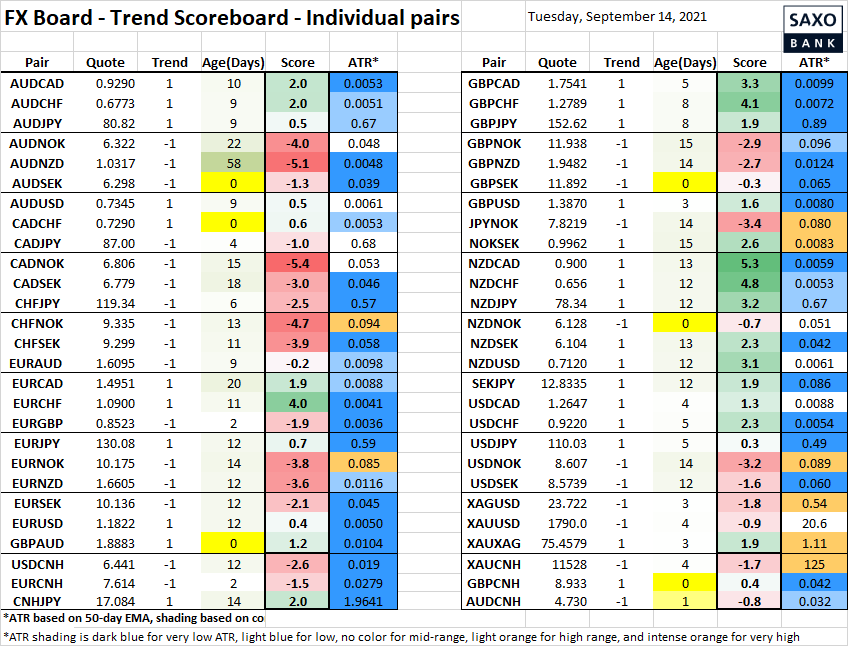

Table: FX Board Trend Scoreboard for individual pairs

Regarding the recent switch back to the upside for GBPUSD, note that the pair is trading near resistance with US CPI up later today and UK CPI up tomorrow, with the UK certainly winning the rate spread race all year.

Upcoming Economic Calendar Highlights (all times GMT)

- 1000 – US Aug. NFIB Small Business Optimism

- 1230 – Canada Jul. Manufacturing Sales

- 1230 – US Aug. CPI

- 1300 – UK BoE Governor Bailey to speak

- 2030 – API Weekly Reports on Oil stocks, supply and demand

- 0030 – Australia Sep. Westpac Consumer Confidence survey

- 0200 – China Aug. Retail Sales / Industrial Production