FX Trading focus: Long treasury, Bunds yields pop. Pivotal German election Monday

The reaction to the FOMC meeting largely fizzled yesterday as the market was able to absorb a sharp, if relatively modest adjustment higher to Fed expectations for the approximate time frame of liftoff (June 2022 EuroDollar STIRs are unchanged relative to before the FOMC meeting, Dec. 2022’s are down about 7 ticks around and Dec 2023’s are down around 11 ticks). Risk sentiment decided that the FOMC meeting outcome was sufficiently benign to dive back into recent beaten down equities, the US dollar headed sharply lower versus the usual risk-on crowd of currencies.

Later in the day and overnight, however, a jolt higher in US treasury yields at the long end of the curve after a long period of range bound limbo has suddenly seized our attention and has sent the Japanese yen into a tailspin. Sympathetic moves were seen elsewhere in German Bunds and UK gilts, with the yields for 10-year Gilts poised at a key resistance level after the massive shift higher all along the UK yield curve yesterday after the BoE meeting, and the German 10-year Bund yield now up through what looks to be a pivotal -0.25% yield level. The German election outcome discussed below will potentially add further energy to the yield moves in Europe.

For now, whether this yield move is merely the beginning of a further rise in yields to come should dominate our attention, as any sort of momentum will keep a negative spotlight on the JPY and potentially CHF and will inevitably impact risk sentiment at the margin and quite broadly if we poke back all the way to the highs for the cycle in the US 10-year Treasury yield at 1.75%.

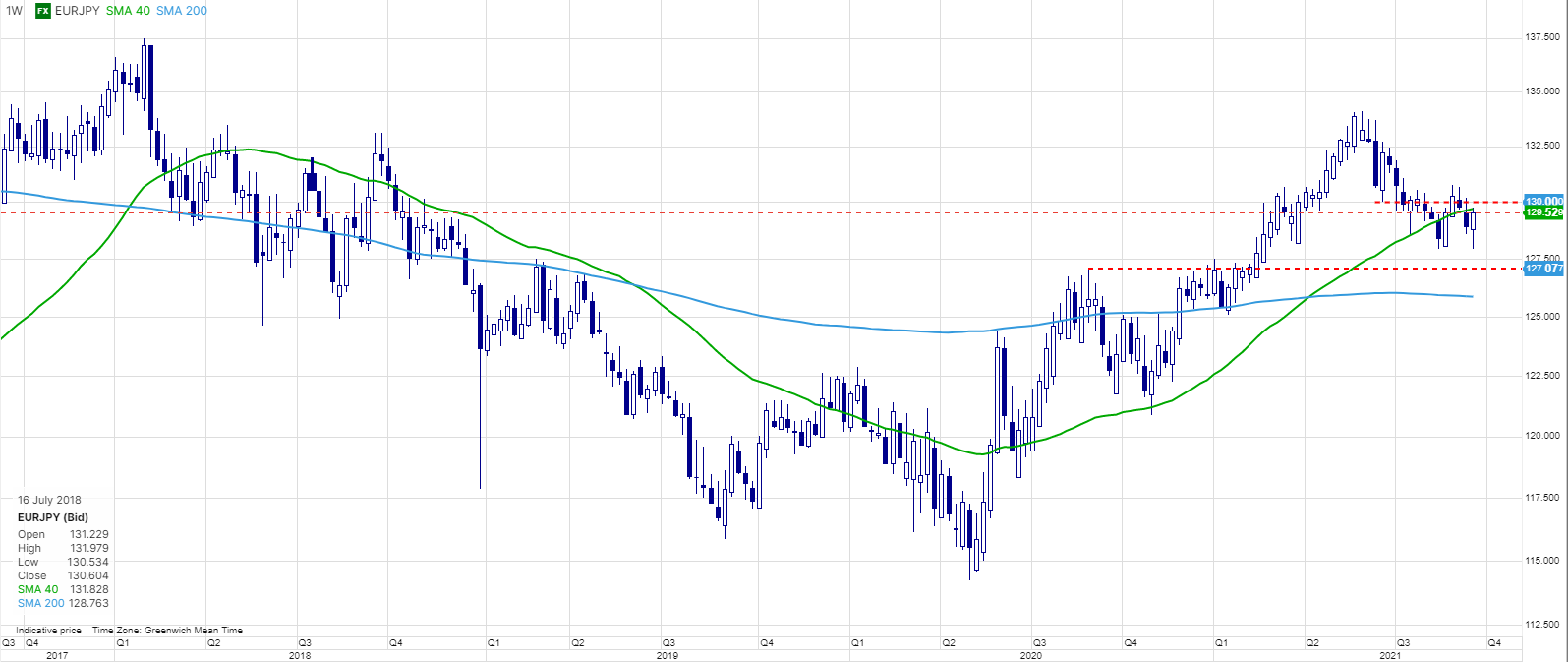

Chart: EURJPY weekly

EURJPY launched a sharp rally yesterday on the risk in long yields, which also affect EU fixed income, as Bund yields. The stronger the mandate the likely center-left coalition gets in the German election outcome, the greater the potential for EU yields to rise and EU yield curves to steepen, supportive for the euro and a headwind for the JPY, especially as Japanese fiscal plans are seen as less JPY supportive and more likely to crimp Japan’s real yields, which have so far somehow escaped the developments elsewhere, but can’t defy gravity forever if energy prices continue rising. In any case, EURJPY deserves watching here as a function of the ability of the EU yield curve to continue to steepen in sympathy with any possible developments in the US yield curve and as a function of the German election outcome. We present the weekly bar as today’s close offers could see a weekly hammer candlestick.

German election dead ahead Will cover this issue more in detail on Monday, but have a listen to today’s Saxo Market Call podcast for a partial discussion on the likely outcome and the potential difficulties in forming a majority ruling coalition in the wake of the German election. Since the advent of the AfD and its 10+% result in the polls in 2017 and a likely similar result tomorrow, majority coalitions are tough to build when neither side of the center is willing to consider working with the AfD. The “stoplight” coalition idea is much discussed, but the “yellow” FDP has a traditional liberal/supply side focused platform that looks incoherent compared to the Red/Green focus on higher wages and significant fiscal outlays.

In terms of how to trade the German election, the likely difficulty in forming a ruling coalition could make this a slow burn issue for months, but EURCHF upside optionality is still fairly inexpensive at 4.25% implied volatility for 3-month tenors if we get a surprisingly strong result and mandate for the Greens/Reds and a repricing much higher of EURCHF in the weeks and months to come.

Crunch time for debt ceiling and key US fiscal packages starting next week. The situation is simply too complex to reduce to a few lines here, but the basic outline is that some progressive Democrats are engaging in brinksmanship over the smaller, bipartisan $1 trillion infrastructure bill passed by the Senate but not yet by the House.Progressive Democratic House members have declared they will not vote in favour of the infrastructure deal unless the progressive $3.5 trillion (spread over 10 years) mostly climate- and social spending bill is tied to the infrastructure deal. In other words, the risk is of a failure of both bills and a complete failure of the domestic Biden agenda, with the kicker that the Republicans could retake the house in mid-term elections next fall. Meanwhile, the debt ceiling issue has not been addressed, with the US treasury needing to enact emergency measures after September 30 (end of the budget year next Thursday) if no stop-gap funding bill is passed and a theoretical default possible “some time in October” according to US Treasury Secretary Yellen if nothing is done. Of course something will be done, but a government shutdown and a shadow over the markets could result from this nonetheless in coming weeks.

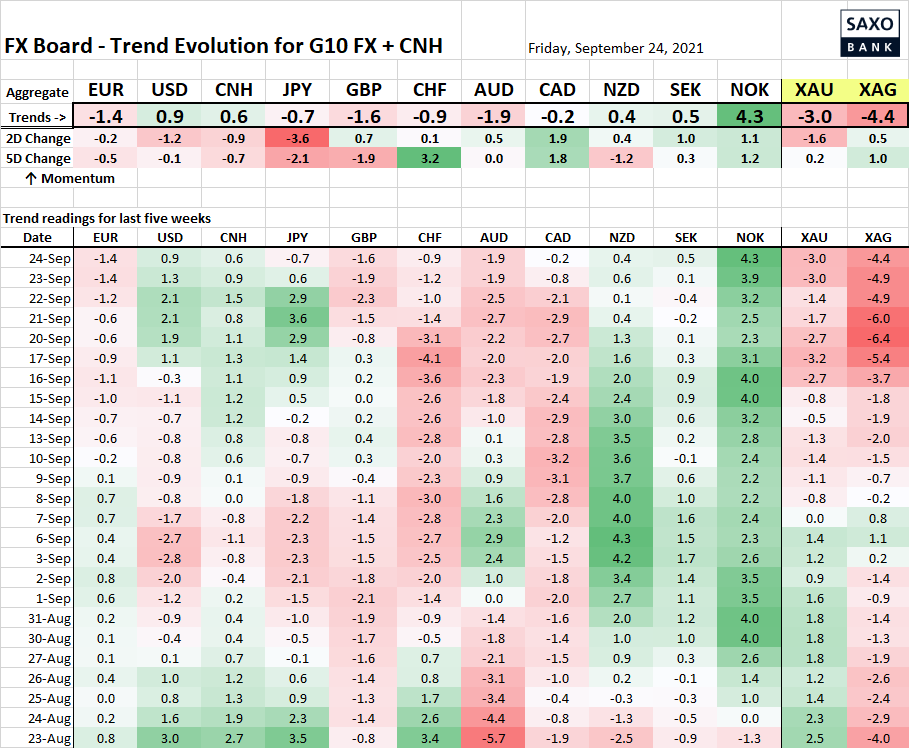

Table: FX Board of G10 and CNH trend evolution and strength

Note the pickup in NOK and GBP after respective central bank meetings, although from the Norwegian yield curve reaction, most of the message was in the price so NOK will quickly revert to tracking risk sentiment and energy prices. The momentum reading for JPY for the last two days is a stunning -3.6, quite a jolt.

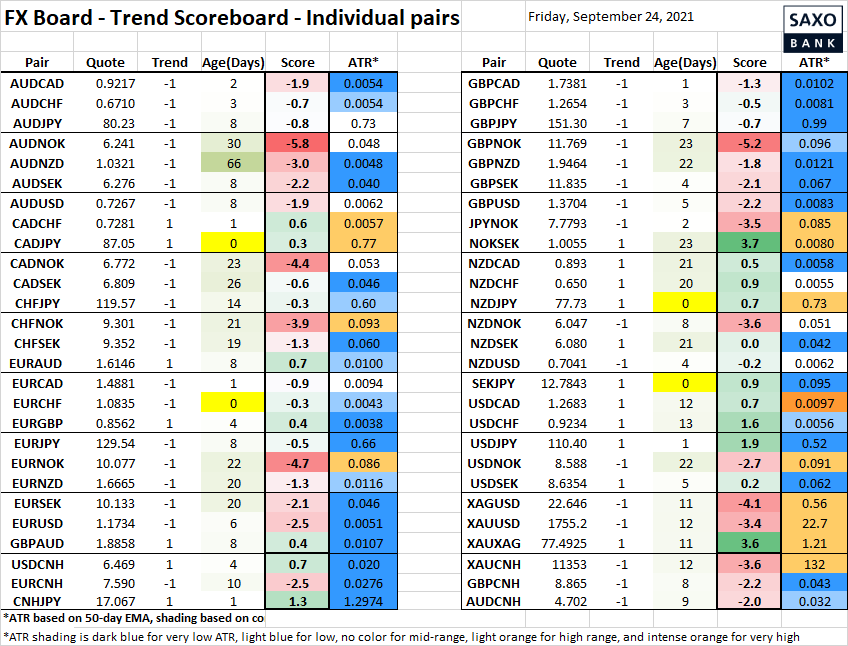

Table: FX Board Trend Scoreboard for individual pairs

Oddly, EURCHF still sucking wind despite the big yield moves yesterday – is that hedging the German election? Could see significant volatility in that pair next week – would prefer long upside volatility there. Elsewhere, note additional JPY crosses already changing direction back to the upside, including NZDJPY, SEKJPY and CADJPY if these close near current levels today.

Upcoming Economic Calendar Highlights (all times GMT)

- 1245 – US Fed’s Mester to speak on economic outlook

- 1315 – ECB’s Lane to Speak

- 1400 – US Aug. New Home Sales

- 1400 – US Fed’s Powell, Clarida to speak

- 1405 – US Fed’s George (non-voter) to speak