FX Trading focus: USD surges on modest yield rise, suggesting

The US dollar was higher yesterday as US yields surged in the wake of a much stronger than expected Retail Sales report, particularly for the robust ex-Auto and Gas core reading of +2.0% month-on-month vs. 0% expected (even if it was flattered significantly by a -0.7% downward revision of the July data). The USD popped higher on the news, particularly against the lowest yielding CHF and JPY, but with EURUSD also dropping to the lows of this consolidation. The sensitivity to the single data point perhaps reveals where the market is more sensitive to next week’s FOMC (much more below on that) than to the specific scale of the surprise in this data. Later today, will watch the preliminary US September University of Michigan survey with interest after the terrible August reading that came in below the worst pandemic outbreak months early last year. As noted in today’s Saxo Market Call podcast.

Elsewhere, the unfolding Chinese situation should demand considerable attention, and the fairly strong CNH is interesting relative to the negative news flow and weak performance of Chinese assets. There is some talk of tightness in funding driving CNH strength due to the contagion from property developer Evergrande’s woes and the PBOC overnight offered more liquidity in a repo operation than it has in a while. But given China’s policy directions laid out in recent months and the implications for whole categories of equities, it is difficult to drum up a positive narrative for the currency – could we have seen the lows in USDCNH for now?

Chart: USDCHF

Yesterday’s session saw USDCHF suddenly vaulting clear of the recent range highs that had held back prior attempts higher, though there a prior range high still blocks the open area toward the major 0.9475 area pivot from back near April 1 – not coincidentally the day of the highest long US treasury yields as those were sharply repriced during Q1. Interesting on that note to see that this move is “outperforming” the sharp rise in the US 10-year treasury yield yesterday as we have a break higher in the price action here even with the US yields bogged down in the range. A major contributing factor to the CHF weakness here is likely the situation in EU yields rising to new local highs and EURCHF slipping above 1.0900 – a local high and coincidentally at the 200-day moving average as well.

Initial preview of FOMC meeting next Wednesday. The highlight of the week next week is the FOMC meeting on Wednesday, which will see the latest set of Fed projections on inflation, employment, GDP and rate forecasts in the dot plot. To recall, the June FOMC meeting saw a sharp shift higher in Fed expectations on the fed forecast dot plot shift and the general sense that the Fed is moving in the direction of tightening. Since the June FOMC meeting, expectations have triangulated to the very middle of the range established back before and after the June meeting, suggesting that the market is not leaning in either direction at all and thus perhaps that the bar to a hawkish surprise is quite low, with that stance in part encouraged by Fed Chair Powell’s dovish Jackson Hole speech in late August. I suspect we are set for a decent hawkish surprise as the Fed would like to get this taper rolling to have a more nimble stance next year if employment surges into the end of the year.

A long list of additional central banks next week. Besides the Fed next week, we have the BoJ also up next Wednesday, with little expected there as interest in Japan will likely only pick up on new fiscal initiatives on the other side of the election set to take place on or before November 28. More important in terms of the potential to affect price action are the Riksbank meeting on Tuesday (guidance after the hot August Sweden inflation data) and the Norges Bank meeting on Thursday – with a 25-bp rate hike expected, with further guidance the key after this hike has been flagged. The Bank of England is also up on Thursday, with a heavy lean from the market on anticipation of further guidance in the direction of removing accommodation sooner rather than later. (BoE expectations out in 2022 at the highs for the cycle here). EM watchers should note the Hungarian Central Bank meeting on Tuesday, China’s PBOC Wednesday, Brazil late Wednesday, Turkey on Thursday and South Africa on Friday.

CAD not fretting the election on Monday. Canadian prime minister Justin Trudeau’s gambit to take advantage of apparent popularity in the polls and reap a ruling majority in a snap election has backfired badly, with oddsmakers about 50-50 on whether Trudeau’s liberals or the now more centrist Conservatives will win the election, with a minority government likely in either case and the Conservatives turn toward the center on climate likely meaning less contrast, particularly with a minority government, than outcomes in past elections.

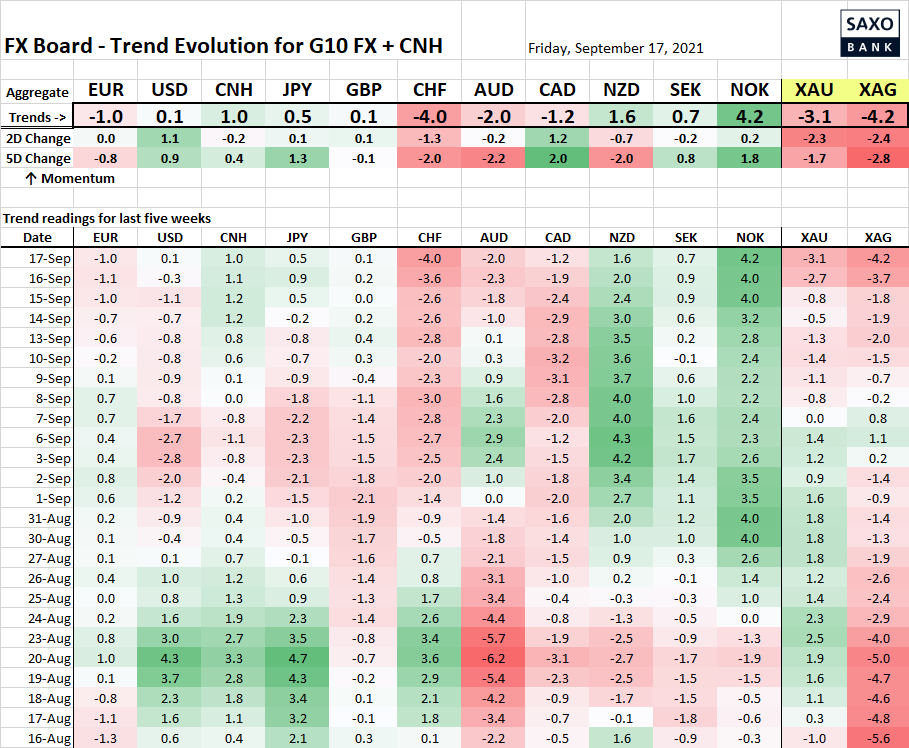

Table: FX Board of G10 and CNH trend evolution and strength

The loss of momentum in NZD this week despite supportive GDP data prompting new highs in the yield outlook suggest that kiwi outperformance is in danger of failing from here. Watching NZDUSD closely next week as the attempt above the 200-day moving average over the last two weeks has failed. Interesting to note the CHF weakness as noted above, and wondering how long JPY can remain out of synch with that development.

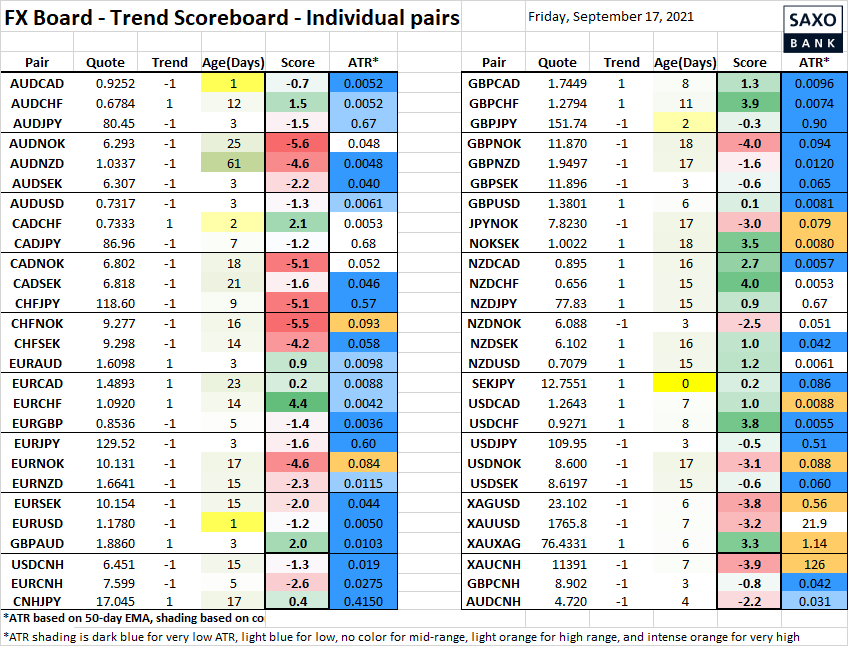

Table: FX Board Trend Scoreboard for individual pairs

EURUSD has rolled over again, looking heavy if yesterday’s lows fail, but probably needing an additional jolt from the FOMC meeting next Wednesday to lurch into a proper new downtrend that takes out the 1.1664. Note that GBPUSD is toying with turning lower as well, though the technical situation is quite rangebound there, with a clearer downside break signal only arriving if the pair sustains a break below 1.3725-00 post-FOMC (and BoE) next week.

Upcoming Economic Calendar Highlights (all times GMT)

- 0800 – ECB’s Hernandez de Cos to speak

- 0900 – Euro Zone Final Aug. CPI

- 1400 – US Sep. Preliminary University of Michigan Sentiment & Inflation Expectations