FX Trading focus: Market very extended in spots

As mentioned in Friday’s update, this market looks very extended on recent themes of commodity strength and JPY weakness. On Friday I pointed out that the Japanese Yen real effective exchange rate (adjusted for CPI inflation) is nearing its lowest ever from the 2015 time frame and this morning on the Saxo Market Call podcast I pointed out the remarkable advance in NOKJPY as an example of how extended that specific pair looks after ripping more than 10% higher in the space of less than two months. At the start of this week, we theoretically have fresh ammunition for JPY bears as US 5-year yields are rushing to new highs since just before the markets were cratered by the pandemic last year, while 10-year yields are back toward the recent cycle highs from last week. But note that 30-year US yields are still at the lower end of the range and an interesting counterpoint as the US yield curve from 5 to 30 years flattens aggressively. Certainly, USDJPY has reached a major chart point by having risen to the 114.50 area that provided resistance for much of 2017 and even parts of 2018.

Elsewhere, the kiwi got a big boost overnight on a very hot CPI reading – more in the NZDUSD chart below. And ECB President Lagarde at the weekend still wants to call inflation risks transitory, while Bank of England Governor Bailey said the bank “will have to act” on rates to counter inflation, further boosting short UK rates after a huge rise last week. He also said, by the way, that central bank policy doesn’t have the tools to deal with supply chain issues and that he still viewed the recent rise in inflation as temporary.

Tomorrow I am hosting an FX Update webinar, you can sign up here.

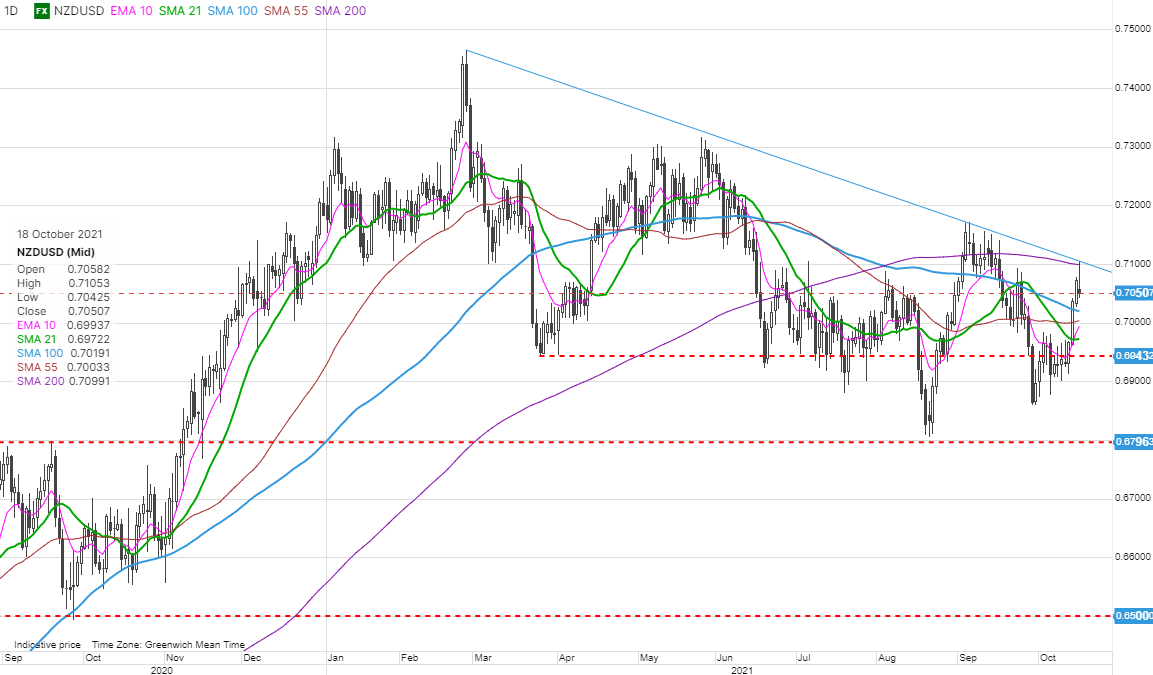

Chart: NZDUSD

After the very hot New Zealand Q3 CPI reading of 2.2% QoQ in particular (vs. +1.5% expected) and +4.9% year-on-year, the market expectations overnight for the November 24 RBNZ meeting ripped higher, taking expectations to about 50/50 of a 50 basis point move at that meeting. At the same time, we have covid restrictions in Auckland extended for another two weeks, though this doesn’t seem to affect RBNZ expectations. NZDUSD rallied sharply to the 200-day moving average and 0.7100 area before retreating on weak risk sentiment overnight, with the latter likely in control for whether the pair can break out of the choppy downtrend of the last many months.

The macro calendar for the week ahead is fairly quiet, with interesting bits and pieces, however.

- Today, we get a look at Poland’s Sep. Core CPI reading, the latest US Industrial Production data point and one of the more leading indicators on the US housing market, the NAHB Housing Market survey, which has remained strong relative to pre-pandemic years, but is well off the peak readings of late last year.

- Tuesday: We have Hungary’s rate decision up tomorrow after the central bank surprised with a smaller than expected the last time around and with EURHUF poised near the top of the range. By the way, a challenger, Peter Marki-Zay, won a primary election to face off against Viktor Orban under the banner of a united opposition in the spring 2022 election. Polls shows the opposition is in a dead heat with Orban’s Fidesz, which has dominated Hungary’s politics for more than a decade and has the country in hot water with the EU over rule-of-law issues. The prospects for a transfer of leadership could have considerable influence on HUF in coming months of the polls begin to tilt in favour of the opposition. Also up tomorrow are US September Housing Starts and Building Permits.

- Wednesday: China to make a decision on rates, with no signs that the PBOC is climbing down from its tight monetary policy. The UK CPI is up as the last inflation reading ahead of the November 4th BoE meeting, with most of a 25-bp rate hike priced in as of today and after Bailey comments at the weekend (see above). We also have the US Fed’s Beige Book, where the anecdotal reporting on the degree of labour shortages and supply chain issues could make for interesting reading. Canada’s September CPI is up as the market is pricing BoC liftoff for as early as January of next year, with higher odds at the April meeting.

- Friday: UK Sep. Retail Sales and the global flash October PMI’s, including those that get the most attention from the market in Europe.

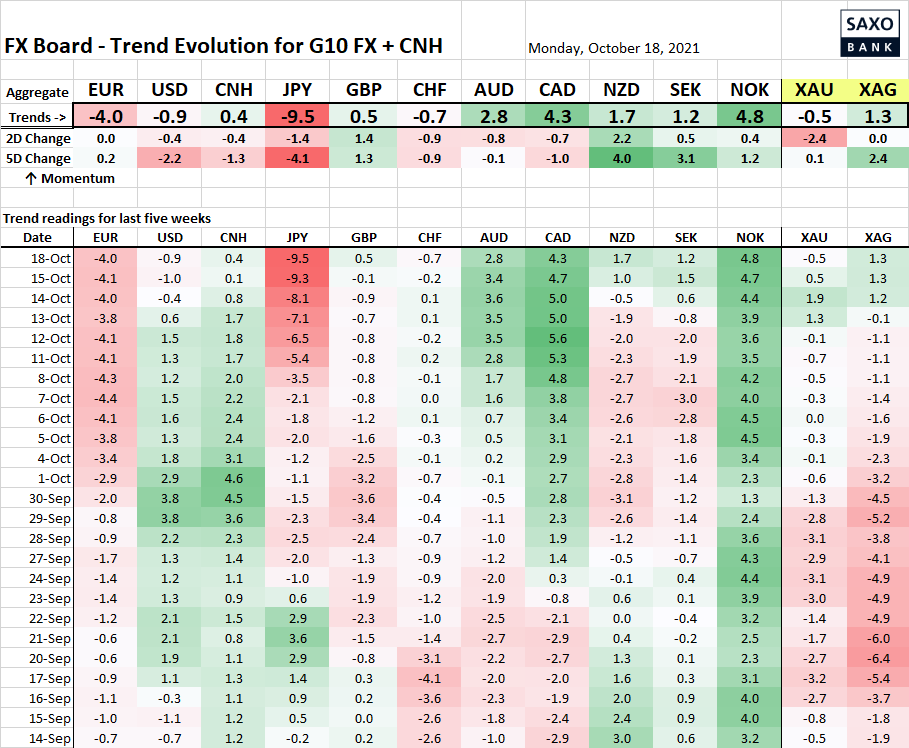

Table: FX Board of G10 and CNH trend evolution and strength

As noted above – the JPY reading is at a remarkable extreme – has the market overplayed its hand there in the near term, given that it is coming with the JPY near all-time “real effective exchange rate” lows? Elsewhere, note gold losing altitude badly late last week.

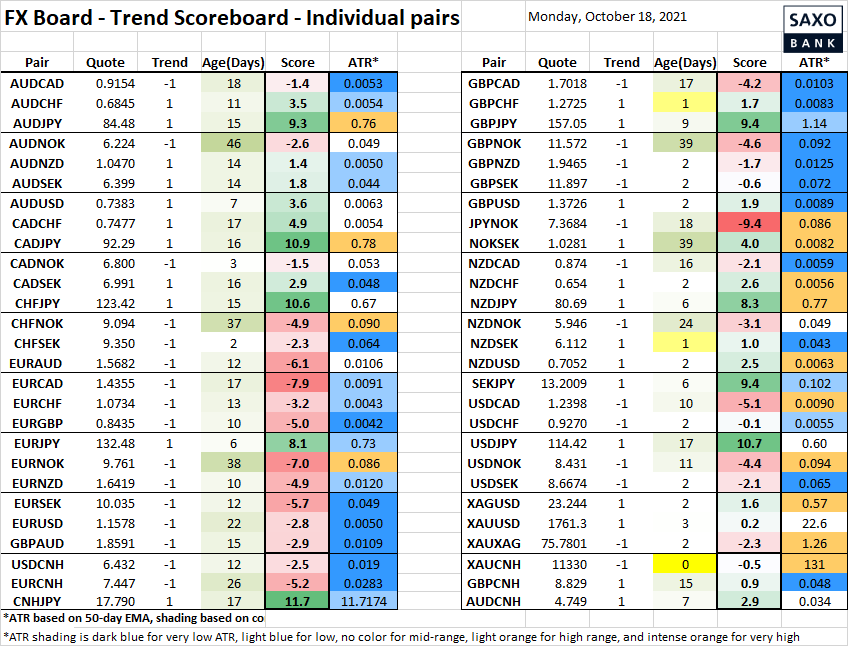

Table: FX Board Trend Scoreboard for individual pairs

Little new of note here as we watch whether new USD downtrend flips hold, like in AUDUSD, NZDUSD, USDCHF and GBPUSD.

Upcoming Economic Calendar Highlights (all times GMT)

- 1200 – Poland Sep. Core CPI

- 1215 – Canada Sep. Housing Starts

- 1315 – US Sep. Industrial Production / Capacity Utilization

- 1400 – US Oct. NAHB Housing Market Index

- 1430 – Canada Bank of Canada Q3 Business Outlook

- 0030 – Australia RBA Meeting Minutes 1620 – US Fed’s Williams (voter) to speak