FX Trading focus: FOMC sparks a USD rally that may have legs

Two initial thoughts about positioning yesterday’s FOMC meeting. First, while I got the direction right in thinking that we would get a hawkish surprise, I am a bit surprised at the degree to which the market reacted to what the Fed actually delivered, which was fairly modest on the surface. Second, while there is a mismatch in scale to the reactions across markets, the way in which nearly everything moved in the same direction suggests notable volatility risk from here if the reaction sticks.

Now, in terms of what actually happened and didn’t happen at the FOMC meeting last night:

The “dot plot” shift headline grabber: the clearest outcome was the surprisingly large shift forward in when the median fed forecaster sees the Fed achieving lift-off, with the median now suggesting two hikes by the end of 2023, a shift from March, when the median forecast was still for no lift-off until 2024. There is some risk of over-interpretation (especially as Fed Chair Powell clearly disdains the dot plot), as the dots don’t differentiate where the Board of Governors voted versus regional Fed members, etc. Still, a generally higher set of policy forecasts despite very modest longer term inflation forecast adjustments (more on that below) suggests a general weakening of the Fed’s confidence in is belief that inflation will prove transitory. It’s a signal.

Statement changes: few, but “progress“ noted on vaccination – given the use elsewhere that the Fed will consider tapering when “significant further progress” has been made toward its goals, this is maybe more significant than I picked up on at first glance.

Economic forecasts: the GDP and unemployment forecasts are too trivial to mention, but the huge upward revision in the 2021 inflation forecasts is notable, if only because the Fed couldn’t keep the forecast due to price rises already in the bag. The 2022 and 2023 forecast rises were only 0.1% and 0% for the 2023 core inflation forecast – direction more important than size, perhaps, and arguably, even shifting them at all suggests current inflation levels are bleeding into forward forecasts.

Q&A – tapering, labor market, and inflation expectation observations – Powell said in the Q&A that the game of “talking about talking about tapering” is in the rear view mirror and that taper talk is happening, even if there was no commitment to a time frame (maybe even the July meeting for exiting the unnecessary MBS purchase programme but nearly 100% for September FOMC?). There were some interesting exchanges on the status of the labor market as well, with some analysts arguing that Powell’s comments on labor force demand (remember massive April JOLTS survey, for example, suggesting 9.2M job opening) being high while there have been a “slew of retirements”. This suggests a demand/supply mismatch that, between the lines, could mean employers will need to bid up for workers. As the great Fed watcher Tim Duy tweeted (@TimDuy) last night: “Powell is totally backing off his conviction that the economy can return to pre-pandemic LFPR” [LFPR=labor force participation rate). As well, Powell noted the rise in inflation expectations, which used to be very prominent in Fed inputs.

What now? The USD is rallying hard and has room to run for a while if this move sticks as the market needs to make a significant adjustment in recognizing that at least a shadow has been cast over the Fed’s “transitory” scenario, with the market poorly positioned for that fact. As expected, EM has corrected sharply and could have the most to adjust to the new reality, but besides the EURUSD noted below, we are also noting the breakdown in GBPUSD below 1.4000 and AUDUSD down threatening the “neckline” like area near 0.7550. A break of this latter one could set up quite a run lower to something like 0.7000 in Q3.

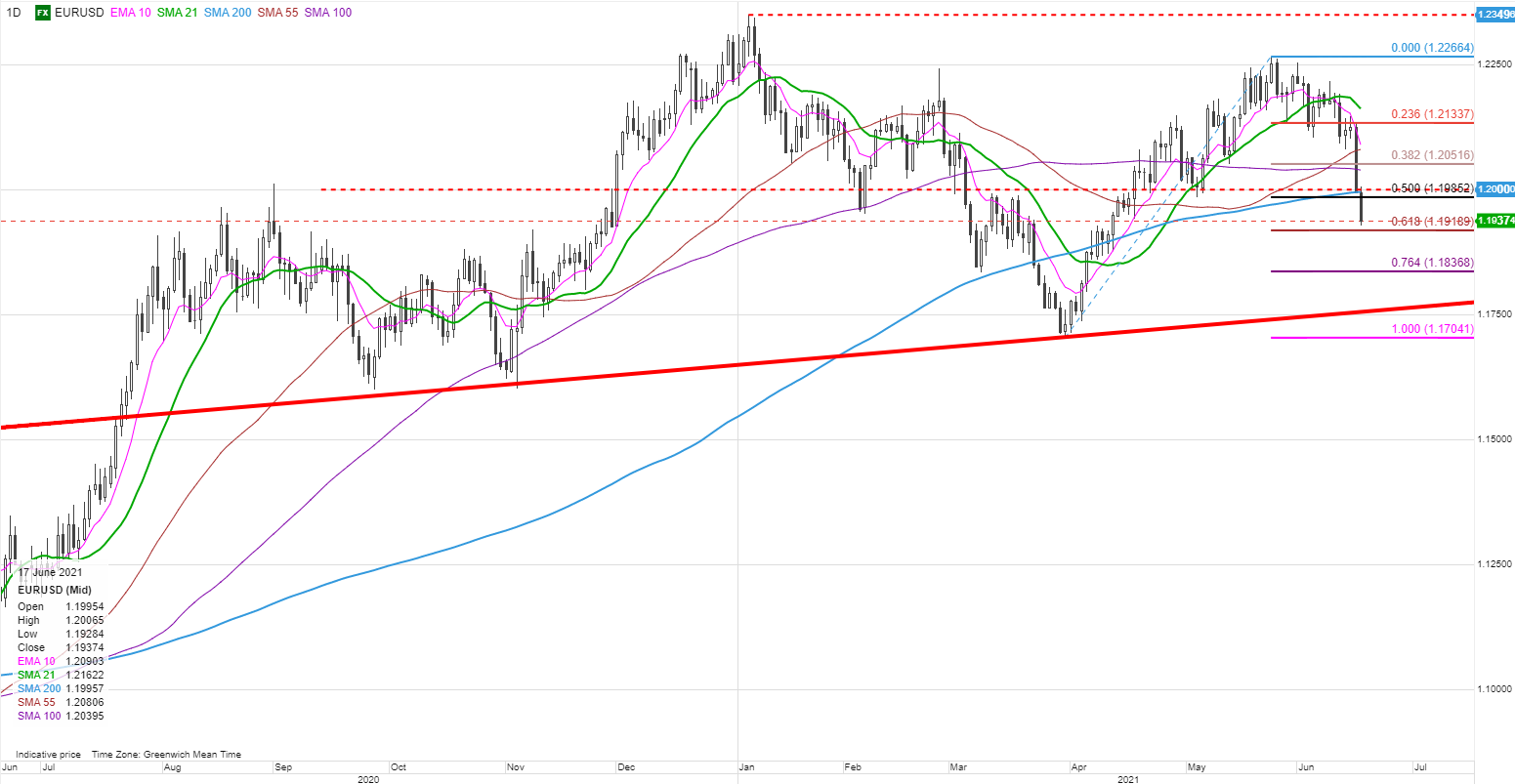

Chart: EURUSD as a proxy for what is next for USD

EURUSD broke down through 1.2000 without much afterthought and the ease with which it did so suggests there may be enough momentum here for more downside still, as the ECB is undergoing no such shift in its stance. Next steps here for EURUSD are 1.1920, which is the 61.8% Fibo of the rally to the recent top, a break of which could cascade the price action toward the head-and-shoulder neckline around 1.1750, and a break of that could bring at least 1.1500 into play, although we’ll take this one step at a time. The bulls’ only hope right here is that we see an immediate reversal of this sell-off – a difficult hurdle, to say the least.

Norges bank flags September rate move. Norwegian rates are sharply higher and NOK has firmed after yesterday’s deep sell-off as the Norges Bank delivered a strong message at today’s meeting, pointing to a September rate hike and more hikes to come through next year. Interesting to see the strength, which will face tough headwinds if US real yields continue rise on the back of this FOMC meeting, crimping risk appetite. It is an important long term fundamental support for the currency, however – will look at fading EURNOK upside eventually if the pair doesn’t reverse fully back lower already today.

Turkey – not the time to talk rate cuts at central bank meeting today. The Turkish Central Bank is not expected to cut rates today, and we should hope that it generally keeps quiet on that front, especially given the timing after yesterday’s FOMC meeting and with the backdrop of USD strength and EM weakness.

Australia – very strong jobs report sets up July “tightening” from RBA in July. The May Australia jobs report The RBA’s resolve to hold out its expectation for no tightening until 2024 will surely be in for a reality check at the July meeting, where it will surely choose to keep the April 2024 Australian government bond as its yield curve control target. Eventually, the RBA will have to abandon the yield-curve-control policy entirely and just hike rates already (STIR futures are already pricing this, and the RBA will feel more comfortable with any adjustments at that July meeting now that other central banks are moving ahead of them), but the Aussie is weak for now in the face of the very strong US dollar. Watching the 0.7550 area closely in AUDUSD.

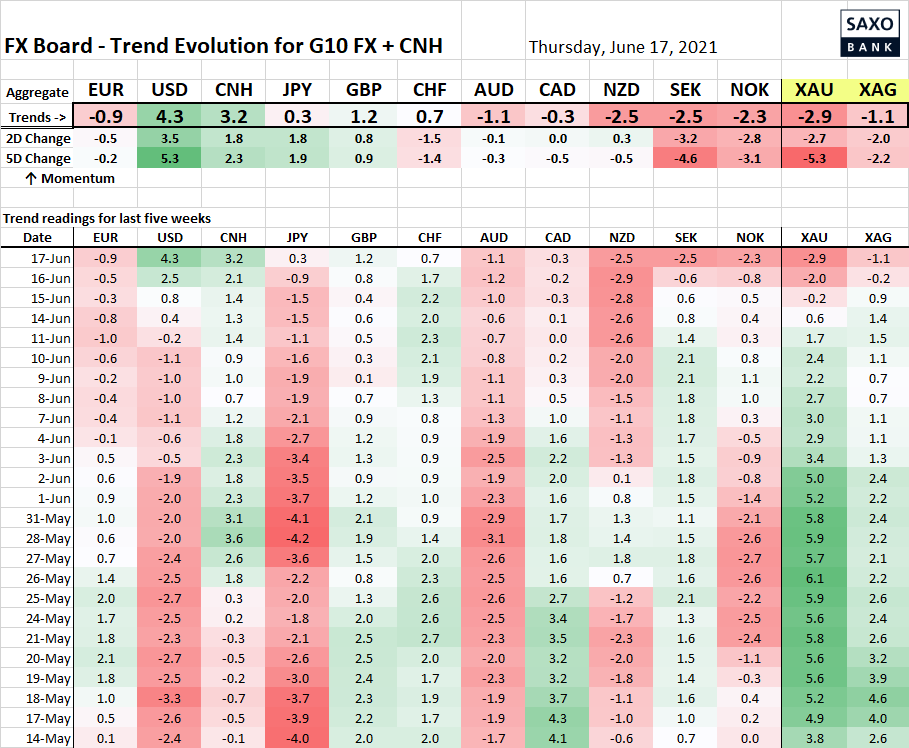

Table: FX Board of G10 and CNH trend evolution and strength

Not much analysis needed here – the USD is gunning higher, the CNH tends to hang on to the big dollar’s coattails and the currencies suffering the most are interesting EUR and CHF. Note the JPY slightly resilient – more on that in tomorrow’s update.

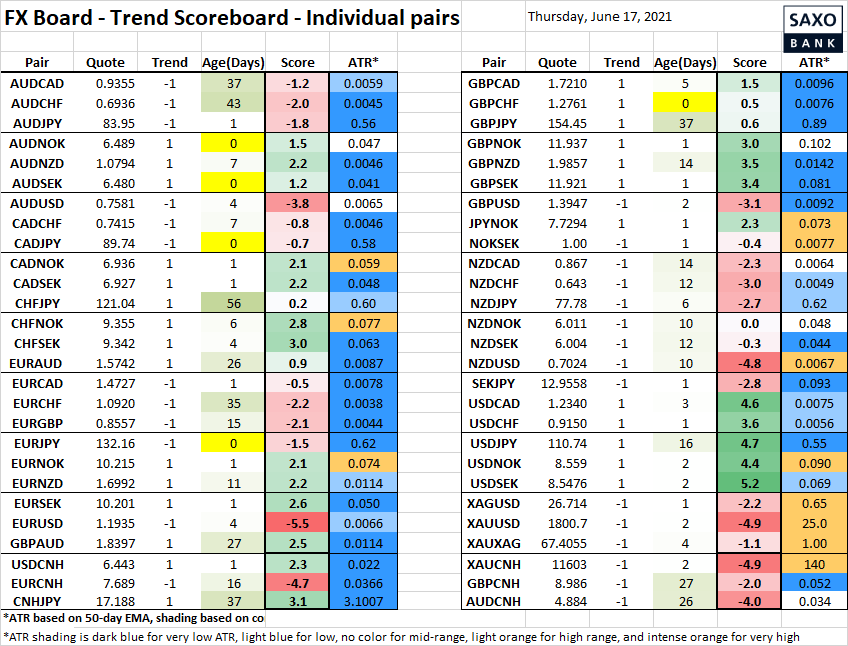

Table: FX Board Trend Scoreboard for individual pairs

Lots cooking here now, with the USD moving into positive territory across the board now and confirming recent upside breaks, while we are curious whether the JPY shows directional sympathy in the crosses – note EURJPY and CADJPY possibly crossing over today to negative trends and AUDJPY did so yesterday.

Upcoming Economic Calendar Highlights (all times GMT)

- 1230 – Canada May Teranet/National Bank Home

- 1230 – ECB Chief Economist Lane to speak

- 1230 – US Jun. Philadelphia Fed Survey

- 1230 – US Weekly Initial Jobless Claims

- 1430 – US Weekly Natural Gas Storage Change

- 2330 – Japan May National CPI

- Bank of Japan meeting