FX Trading focus: USD, JPY and CHF reign supreme. Late joiners arrive in race to bottom.

For those missing my normal FX update yesterday, I was engaged elsewhere, penning a piece on the evidence across markets that we are headed for a more significant market setback. This time, as opposed to previous episodes in the post-pandemic outbreak period, it feels like FX is one of the key driving forces, if not the most important one. And on that note, the amplitude of any extension of this move could prove considerable if not alarming. On the other hand, any USD move that accelerates higher will rapidly become so destructive for confidence that it merely brings forward the inevitable official response. In the meantime, we urge caution and find the complacency in FX options volatility in places remarkable – sub 5.5% in EURUSD 1- and 3-month options – still cheap to take a view!

Conditions look dangerous in this market, with FX at the center of things this time, rather than extremely sidelined, which had been the case many times in 2020 and this year until more recent market action.

Elsewhere, while we are still watching the Aussie pushing ever lower, we note that the newcomers in the race of the smaller currencies to the bottom include especially the Canadian dollar as we discuss in the chart below. Also note that the Scandies have come more than a bit unglued over the last couple of sessions: NOK for similar reasons to CAD, and despite Norges Bank assurances yesterday that it is on track for a rate hike in September, while SEK has dropped through key levels as EURSEK trades up above 10.27 and even posted a nine-month high in today’s session.

And then note the UK, where the Retail Sales data for July looks especially sad given that UK holiday makers are cooped up on the British isles as quaranting requirements in destinations elsewhere limit travel. Thinking of my and my better half’s behaviour when traveling, perhaps the spending of inbound tourists in the past has more than compensated for the net huge annual emigration of UK travelers to sunny climes in Southern Europe? After all, when you properly get away from home, spending discipline is nonexistent. Anyway – pure conjecture, but the pound is suffering heavily as GBPUSD approaches the cycle lows below 1.3600 and if those fall, the enormous 1.3500 level.

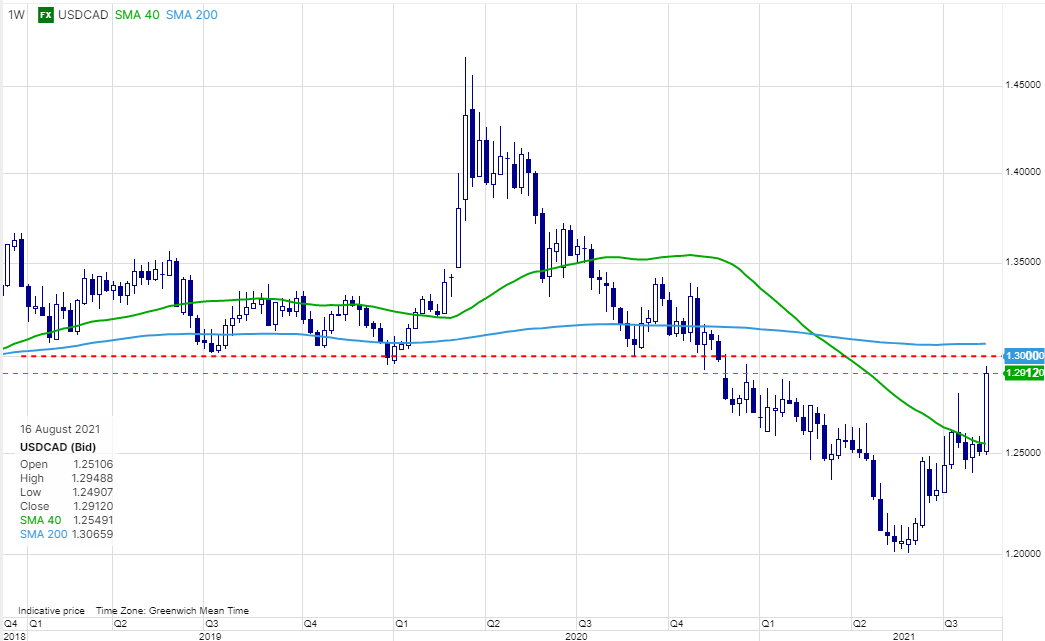

Chart: USDCAD – a very bad week for CAD

The Canadian dollar is finally playing some catch-up with the weakness in commodity currencies elsewhere since yesterday as it has received a real jolt on the latest slide in crude oil prices and on the FOMC minutes encouraging the USD higher as the Fed is clearly beating as hasty retreat on QE as its cautious tendencies will allow. The rate differential story driving the USDCAD push lower actually peaked out in early July, actually well after the lows in USDCAD a month prior. The latest driver here is probably a combination of delta variant concerns driving crude oil lower, but also complacent and probably CAD longs sent for the exits after the 1.2800+ highs from about a month ago gave way with a bang yesterday and overnight. The next critical level is the 1.3000 area, an important level on the way down not only post pandemic outbreak, but also prior to that period in 2019. We’re probably working into solid value territory above that level for pondering CAD longs again, but if we are headed for the kind of more major market correction I discuss in the article I link to above, the risk is prominent of discontinuous moves driven by poor liquidity. In other words, a trader might be better served in waiting for a reversal back lower and wind at the back rather than picking a price point against hot momentum to the upside.

Looking ahead to next week, we note that preliminary PMIs for the Euro Zone and elsewhere are up already on Monday, while the real highlights of the week are the Fed Jackson Hole Symposium scheduled to start very late on Thursday, with US PCE inflation for July up on Friday, as is the final version of the University of Michigan sentiment survey that shocked with the initial read last Friday.

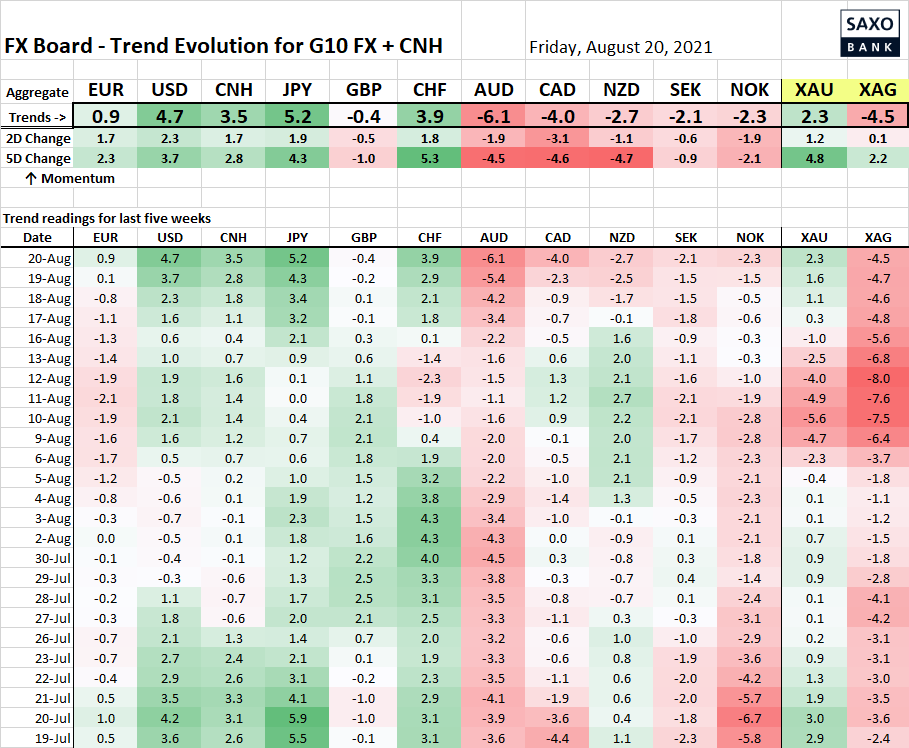

Table: FX Board of G10 and CNH trend evolution and strength

The FX trend readings show the deepening AUD down-trend, with CAD now rushing to catch-up, and NZD and NOK looking weaker as well in momentum terms this week, while gold is catching a relative bid, and JPY, the USD and CHF vie for the top spot.

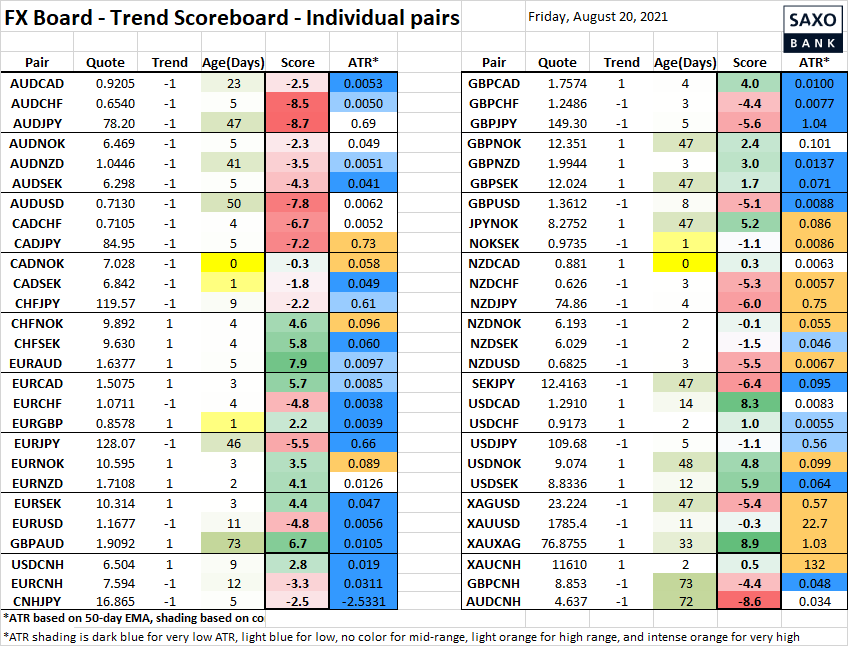

Table: FX Board Trend Scoreboard for individual pairs

Among developments of interest note that the EURGBP trend reading flipping back to positive is a blow to sterling bulls, but is likely simply correlated with risk-on, risk-off as the more liquid euro offers more resilience when positioning goes on the defensive.