FX Trading focus: USD firms again, especially against the Aussie

US treasury yields pushed back lower yesterday and the megacaps among US equities celebrated a US judge tossing out two antitrust suits against Facebook yesterday. In general, the shape of Fed expectations that has developed in the wake of the FOMC meeting suggests that the market is recognizing the risk that the Fed will bring forward the start of a tapering of QE purchases and eventual rate hikes, but that the Fed’s “terminal policy rate” will likely prove lower than was expected just a couple of months ago. It all points to a fairly complacent view that an inflationary spiral is unlikely.

The G10 smalls and sterling were the biggest losers on the day this morning versus the USD and a JPY also on the rise, although SEK is trying to pull back against the euro as of this writing despite the fuss over the failed government and uncertainty on the composition of whatever new coalition emerges as parties have four attempts to put together a new coalition of whatever stripes before an election must be called. A similar episode followed the late 2018 Swedish election, but there was no notable Swedish volatility during the drawn out process that ended in the current weak government that has now failed. And given how evenly divided the political blocs are in Sweden according to the polls, the potential for new policy drama is low, although at the margin this uncertainty could keep the Riksbank on the dovish side, although it is doubtful. A Riksbank meeting is up on Thursday, by the way.

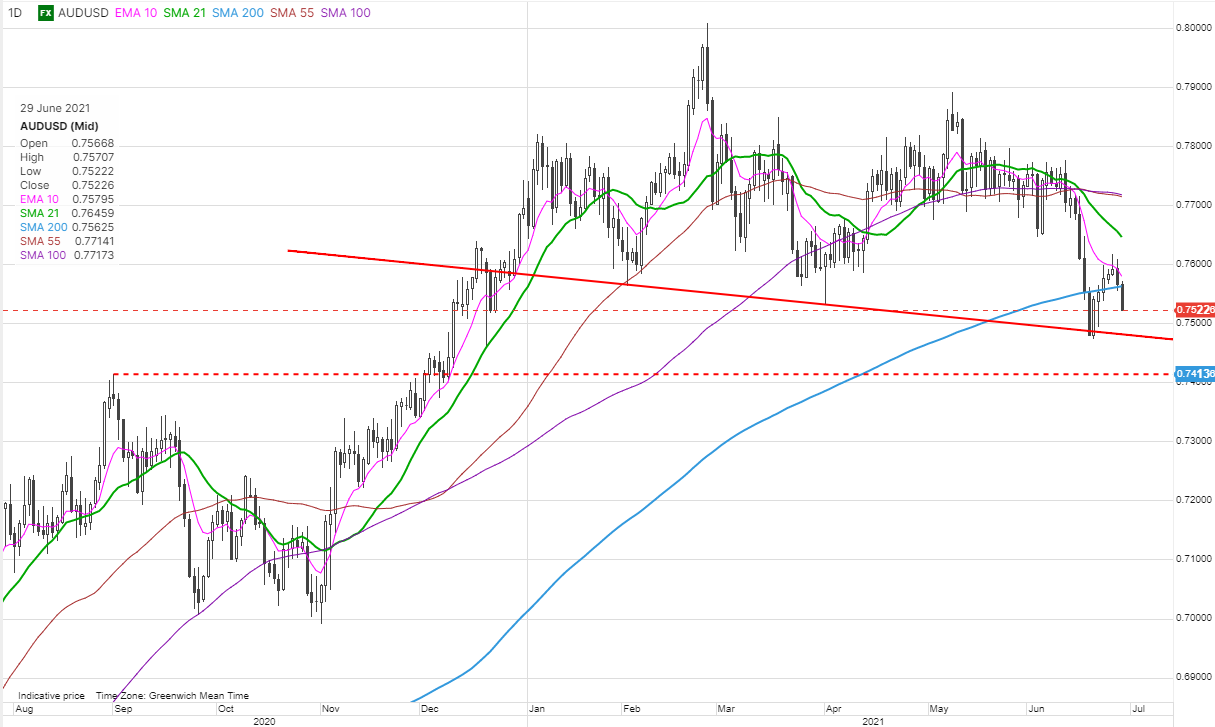

The Aussie has been one of the weakest currencies this week due to the struggles with the Delta Covid variant outbreak causing widespread new lockdowns that could theoretically have the RBA choosing the more dovish option of shifting the 0.1% yield cap policy forward to the Nov ’24 bond from the current April ’24 target. While AUD is lower, yield shifts at the front end of the Australian yield curve don’t suggest . I wonder whether background concerns on the trajectory of China and Australia’s trade relationship with that very important country for Australia’s exports may be weighing more in the background than anything else. Regardless, AUDUSD has retraced about half of the way back to the lows of last Monday, as we analyze in the chart below.

The Friday US June jobs and earnings data are the tactical pivot for whether the USD can find the energy for a follow up move higher as some of the complacency noted above on the outlook is eroded. Alternatively, we could end up with another multi-week bout of doldrums. Some minor interest as well, as indicated in this morning’s Saxo Market Call podcast, in the quarter-end up tomorrow and whether US Treasury yield volatility picks up.

Chart: AUDUSD

The AUDUSD chart is similar to a number of other charts of USD pairs in that we have seen a significant USD rally that has yet to either follow through or find itself rejected. Additionally, for this pair we have an unresolved head-and-shoulders-like situation in which the neckline was completed after an extremely wide right shoulder formed in recent weeks. But we have not yet properly breached the neckline. Looking lower, another major prior price point not much further to the downside is the prior major high near 0.7415. If the current complacency about the Fed outlook is shattered by US data or other developments intrude to send risk appetite and/or commodities on a further steep retreat, we could be set for a more major consolidation lower in AUDUSD after the pair has gone absolutely nowhere for more than half a year, possibly one that extends all the way to 0.7000.

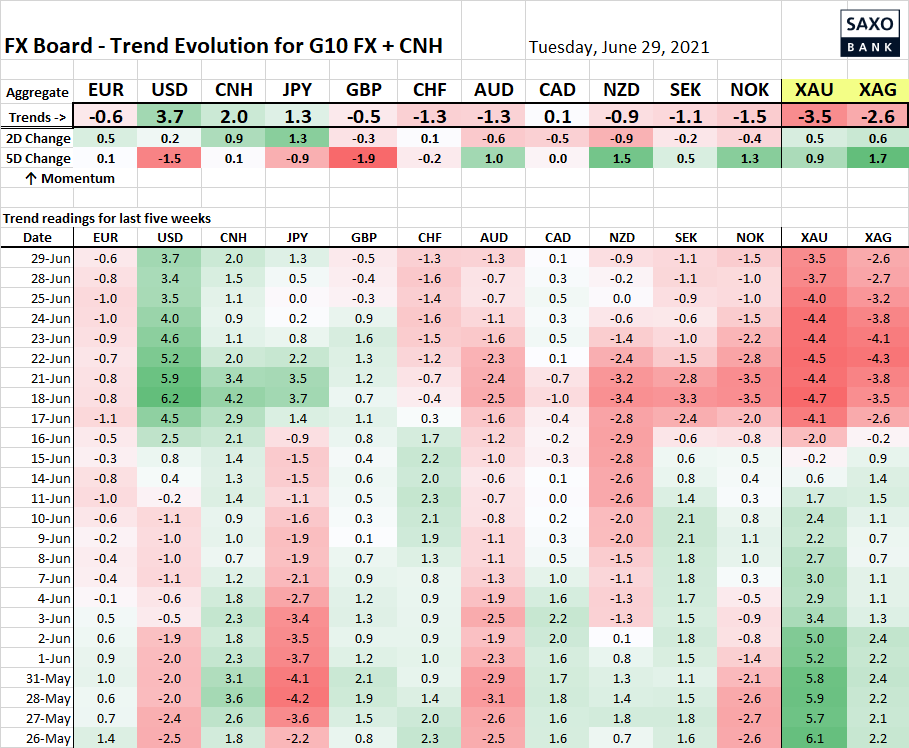

Table: FX Board of G10 and CNH trend evolution and strength

Note in the broad trend readings for each currency that the JPY has managed to pull itself back into positive territory while the G10 smalls ex CAD are all on the defensive.

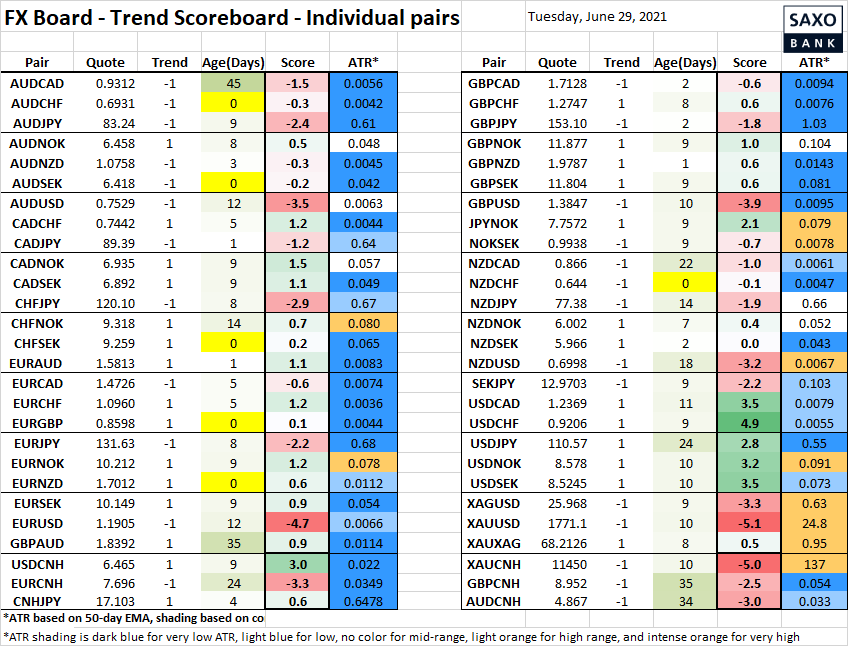

Table: FX Board Trend Scoreboard for individual pairs

We discussed SEK pairs yesterday, but the most important of these, EURSEK, is still in limbo after failing to stick a lower close yesterday.

Upcoming Economic Calendar Highlights (all times GMT)

- 1200 – Germany Jun. Flash CPI

- 1300 – US Apr. S&P CoreLogic Home Price Index

- 1340 – ECB President Lagarde to speak

- 1400 – US Jun. Consumer Confidence

- 2350 – Japan May Industrial Production

- 0100 – China Jun. Manufacturing and Non-manufacturing PMI