FX Trading focus: USD follows US yields higher in the wake of Powell getting nod for 2nd term

The US dollar strengthening in the wake of President Biden’s announcement that he would tap Jay Powell for a second term as Fed Chair extended modestly yesterday and into this morning, somewhat tempered by a strong US 7-year treasury auction taking the steam out rises in yields yesterday – with the 7-year benchmark actually notching new highs for the cycle before retreating in the wake of the auction. The more widely tracked 10-year US treasury yield benchmark is still rangebound below the October pivot high of 1.7% and the post-pandemic outbreak high of 1.75% from the end of March. This has kept USDJPY from extending notably above the sticky 115.00 area of the moment.

Elsewhere, the euro remains relatively weak despite ECB Vice President de Guindos out speaking and hinting some concern on inflation rises: “the ECB is continuously pointingout that the inflation rebound is of a transitory nature….However, we have also seen how in recent months these supply factors are becoming more structural, more permanent.” But just this morning we also have the ECB’s Holzmann out saying that inflation is likely to slow from next year. Later today we will get the expected German government coalition deal (SPD’s Scholz as Chancellor with Green’s Baerbock reportedly set for the foreign minister post and importantly, the liberal LDP’s Lindner set to lead the finance ministry), with a press conference set for 3 p.m. EURJPY and EURUSD are heavy this morning and note that the 128.00 level in EURJPY is a well-defined range low, while EURUSD doesn’t have notable support until well below 1.1200 and arguably not until psychological levels like 1.10. With covid spiking and a galloping energy crisis, I don’t envy the new German leadership.

Overnight, the Reserve Bank of New Zealand waxed a bit more cautious than was expected by the market, and not only by raising the rates 25 basis points rather than the 50 basis points that a minority were expecting to see. In the central bank’s new statement, the bank strikes a more cautious tone: yes, clearly further rate hikes are set for coming meetings, but the bank is clearly in a wait and see mode, given the tightening of financial conditions already in the bag and that which the market has already priced in: “the Committee expressed uncertainty about the resilience of consumer spending and business investment….(and) also noted that increases in interest rates to householdsandbusinesses had already tightened monetary conditions. High levels of household debt, and a large share of fixed-rate mortgages re-pricing in coming months, could increase the sensitivity of consumer spending to these interest rate increases.”

Later today, we have a stack of US data releases crammed into today because of the Thanksgiving holiday tomorrow (and for most, Friday as well). The most important of these is the October PCE Infation data print. Not expecting much from the FOMC minutes later as all eyes are on whether we are set for an acceleration of the QE taper at the December FOMC meeting, with some arguing that Powell and company have more room to move and administer a bit more hawkish message, if they so desire, as the nomination news is out of the way and this reduces hyper-sensitivity to bringing any message that could risk cratering market sentiment.

Chart: AUDNZD

The 2-year yield spread between Australia and New Zealand has risen sharply in recent days and especially overnight, where the more cautious than expected tones from the RBNZ inspired a 14 basis point drop in 2-year NZ yields. The price action in AUDNZD was sympathetic with the rally back toward local resistance near 1.0450, though the rally needs to find legs for a move up to 1.0600 at least to indicate we may have put a structural low in with a double bottom here. A brighter relative outlook for Australia could be in the cards if China is set to stimulate and raise steel output, the anticipation of which has already sharply lifted iron ore prices this week, a key indicator for the Aussie.

No notable expectations for the Riksbank tomorrow – as the central bank is expected to wind down its balance sheet expansion next year, while the policy forecast is thought to be in play (perhaps a late 2024 lift-off built into expectations, though the market is ahead of that as 2-year Swedish swap rates have risen close to 30 basis in recent weeks. This is the area where the Riksbank can surprise in either direction relative to expectations). The EURSEK rally has now reversed the entirety of the prior sell-off leg and double underlines the very weak sentiment on Europe, which remains “non-existential” in nature, i.e., so far the market is keeping this about policy divergence and dark clouds over the economic outlook, not about the longer term viability of the EMU, etc…, which in the past 2010-12 crisis inspired SEK upside as a safe haven.

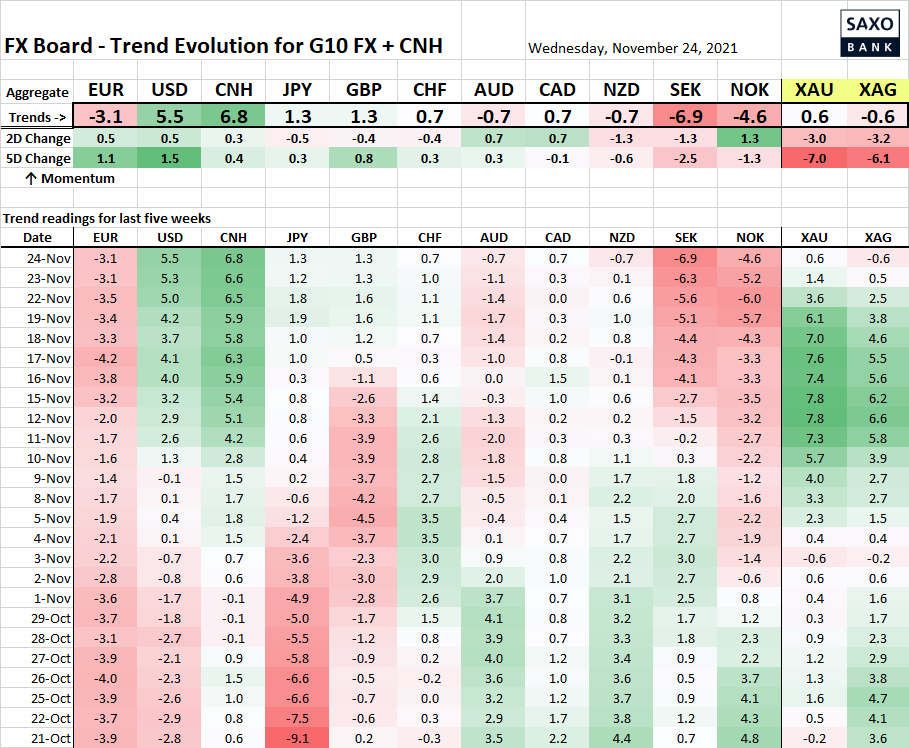

Table: FX Board of G10 and CNH trend evolution and strength

A bit of a relative pick-up in petro-currencies in the wake of yesterday’s oil rally, as the market bought the fact of US President Biden announcing a release of barrels from strategic reserves. Elsewhere, the NZD is losing relative altitude and the USD and especially CNH reign supreme.

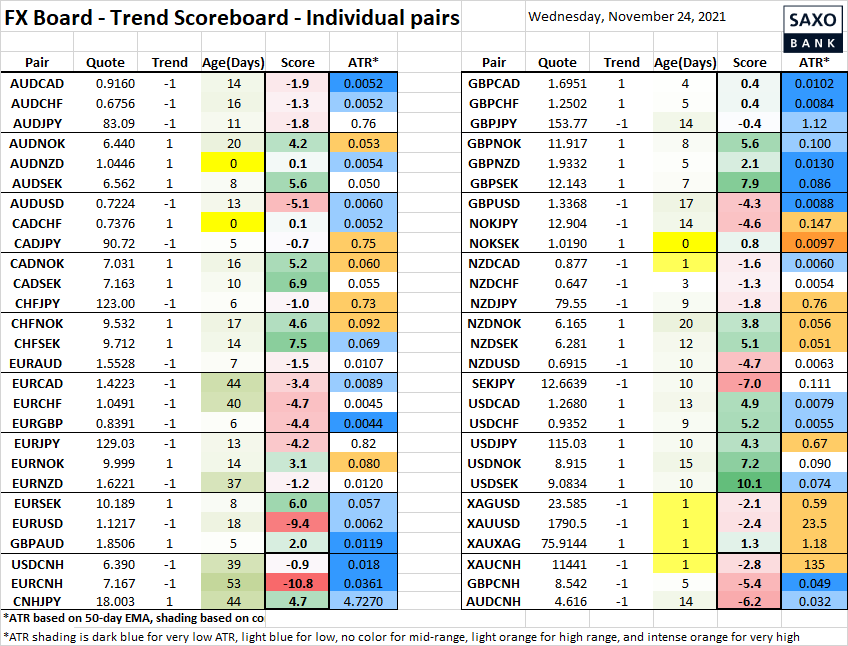

Table: FX Board Trend Scoreboard for individual pairs.

Here, note AUDNZD flipping back to positive – a move that would be “confirmed” by a close solidly above 1.0450. Also note NOKSEK trying to flip positive on the latest oil rally, although beware the Riksbank meeting up tomorrow there.

Upcoming Economic Calendar Highlights (all times GMT)

- 1330 – US Weekly Initial and Continuing Jobless Claims

- 1330 – US Oct. Advance Goods Trade Balance

- 1330 – US Q3 GDP Revision

- 1330 – US Oct. Durable Goods Orders

- 1430 – UK BoE’s Tenreyro to speak

- 1500 – US Oct. PCE Inflation

- 1500 – US Final University of Michigan Sentiment Survey

- 1500 – US Oct. New Home Sales

- 1900 – US FOMC Meeting Minutes