FX Trading focus: USD sell-off sticks. What now?

The biggest reaction to the very weak April US Nonfarm Payrolls Change release on Friday, in terms of what has stuck, is the USD moving lower. On Friday, I wrote that traders should keep one eye on the long end of the US yield curve, as a reversal seemed underway after the knee-jerk reaction, a reversal that might impact the US dollar move as well – but this has proven somewhat misguided, at least so far. There are perhaps at least two ways to interpret what is going on, and the path for the USD from here. I will outline three scenarios for how the market could shape up from here:

- It’s straightforward: the USD is headed lower. We get some kind of stagnation in the US yield curve and a reasonably large extension of the USD lower, as the narrative goes that this weak jobs report has taken Fed taper fears off the table through at least the June FOMC meeting. (We have plenty more weekly claims data, a May jobs report, etc. between now and that June 16 meeting, but nonetheless, two-three weeks of possible daylight if no data spikes concerns back in the opposite direction). Still, the long end of the US yield curve is still key to track, as any new aggressive move higher there relative to yields elsewhere and/or relative to inflation expectations would provide headwinds for bears: recall that it was the US real yield back-up that saw the USD consolidation for most of Q1).

- The USD move lower could run out of steam fairly soon. There are two ways that a USD move lower could run out of steam: risk sentiment suffers an ugly and deep correction on grinding further confirmation that we face stagflationary outcomes – something that this ongoing spike in commodities, if it extends, will guarantee anyway – the question is when and where the Eureka moment comes on that front. A more positive scenario that sees the USD selling curtailed would be data later this week, including the CPI on Wednesday, jobless claims on Thursday and the US Retail Sales data Friday that suggests to some degree the weak jobs report Friday was just noise. It would seem unrealistic to expect this latter scenario to play out already this week unless we get some shock indication from Fed Vice Chair Clarida on Wednesday that there is some weakening of Fed commitment to the scale of its monthly MBS purchase (Extremely doubtful, but this one part of Fed policy looks particularly excessive relative to the underlying fundamentals of a house market spiking and lumber prices completely out of control.)

- It’s complicated – nominal yields rise, but real yields fail to do so, keeping USD weak. In this scenario, we get fresh yields rises in the US at the longer end of the yield curve and new cycle highs coming into view rather soon, but this fails to support the US dollar as commodities inflation and inflation expectations outpace the implications, a cycle that would be unlike the one that supported the US dollar in Q1 – where nominal yields moved more quickly higher than inflation expectations. This would be very novel and could come into play later this year if inflation expectations become embedded and commodities and other inflation pressure signals fail to ease by late summer. This should be the long term consequence anyway of the US running its looser dual monetary and fiscal policies, provided long US rates don’t back up sharply to compensate.

By the way, fascinating story out of the US, where the governors of Montana and South Carolina will wind down their acceptance of federal unemployment benefits in June rather than accepting them to Labor Day in September as the Biden administration has allowed. The argument is that benefits are too generous and resulting in labor shortages.

Chart: AUDUSD

AUDUSD has been a strong gainer after the weak US payrolls numbers on Friday, but also on industrial metals prices screaming to new highs to open the week, with copper solidly above 10,000 dollars/ton for the first time ever and iron ore futures going limit up in Dalian, China. The price action finally took the pair out of the impossibly tight previous range, breaking above the 0.7800-25 range and putting the 0.8000 top within reach. The next chart point is not much higher at just above 0.8100, with generous blank space higher still if commodities can continue gunning higher without destabilizing risk sentiment. At some point, the commodity price rise will force volatility, risk aversion and even credit risk in the wrong direction – hard to know how long the current goldilocks can be maintained.

Sturgeon stumble sends sterling surging

The SNP enjoyed a strong Scottish Parliament election at the weekend, but fell short of the absolute majority that was expected for her party, which very likely keeps any real change for a new independence referendum to take shape somewhere far over the horizon, perhaps giving Boris Johnson a chance to throw some more of the spending and job-creation largesse north of the English border in the years to come. Yes, the Greens are nominally also in favour of leaving the Union and gained two seats, but the market is telling us that the issue is now way off on the back burner for now and likely to stay that way. Sterling is back to outperforming and I would suspect is weakly positively correlated with risk sentiment as some of the relief/sterling upside is linked to capital flows eyeing UK assets that see significant relief on this issue.

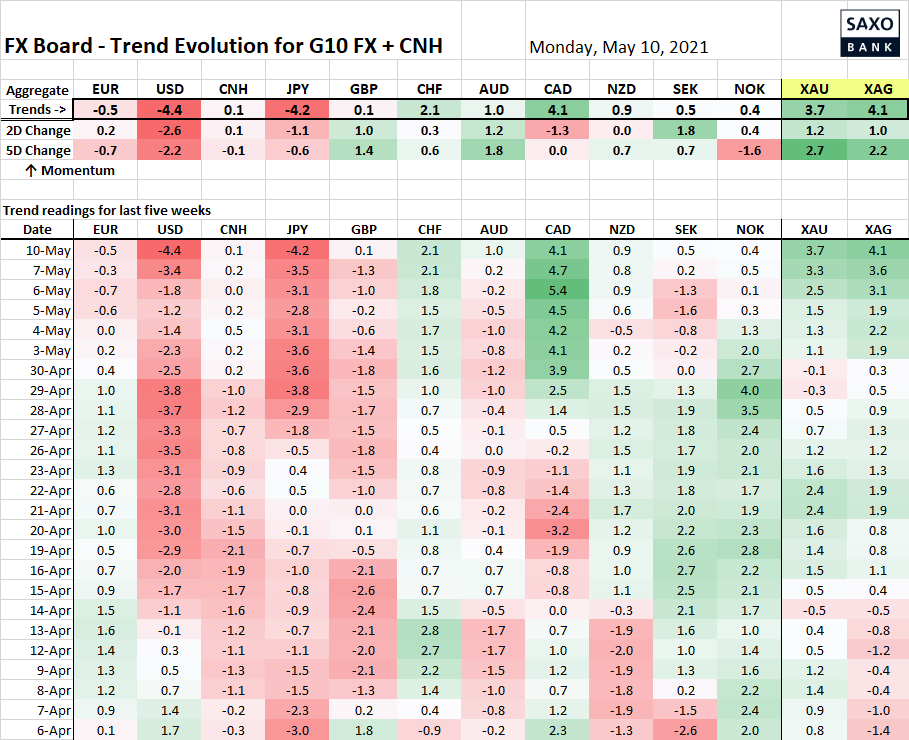

Table: FX Board of G-10+CNH trend evolution and strength

The blistering CAD performance seems to have run ahead of yield spread and crude oil fundamentals in broad terms, and Bank of Governor. In the meantime, the themes are quite clear, with commodity currencies doing well and AUD finally turning more positive, broadly speaking.

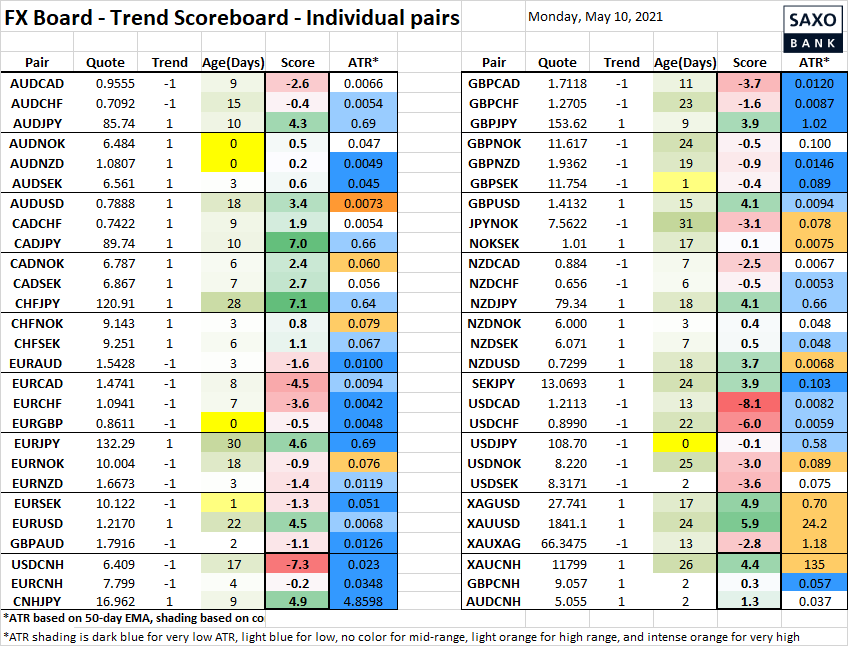

Table: FX Board Trend Scoreboard for individual pairs

Here, note AUDNZD trying to turn positive again today, a move that is certainly supported by developments in industrial metals moves. A move above 1.0800-50 starts to re-heat the bullish potential on the chart. Elsewhere, USDJPY is trying to flip negative, but both of those currencies are weak, although sideways to lower US yields with a bit of risk off could suddenly bring JPY up a couple of notches as the pair looks pivotal mid-range. Also note USDCAD reading -8.1, that is an extreme reading and will be tough to maintain – wondering whether we get any BoC Governor Macklem pushback at a speech on Thursday.