FX Trading focus: JPY over a cliff, getting overdone. UMich sentiment in the spotlight

USDJPY has continued to soar almost without a hitch, with the 114.50 next major chart resistance swinging into view all at once on the backdrop of soaring commodities prices (Japan totally reliant on commodities imports, particularly so in energy) and despite US long treasury yields that have suddenly been tamed this week. That requires other supportive factors for JPY bears, including the commodities issue noted above, strong risk sentiment, rising yields at least at the front of yield curves if not at the long end, but possibly also due to the political shift here. Namely, Prime Minister Fumio Kishida is sending out signals that he will seek to reduce inequality and spoke out rather strongly against the neoliberalism of Abenomics. This is a currency negative development at the margin, although a capital gain tax proposal has already disappeared after it was floated recently and cratered Japanese equity markets.

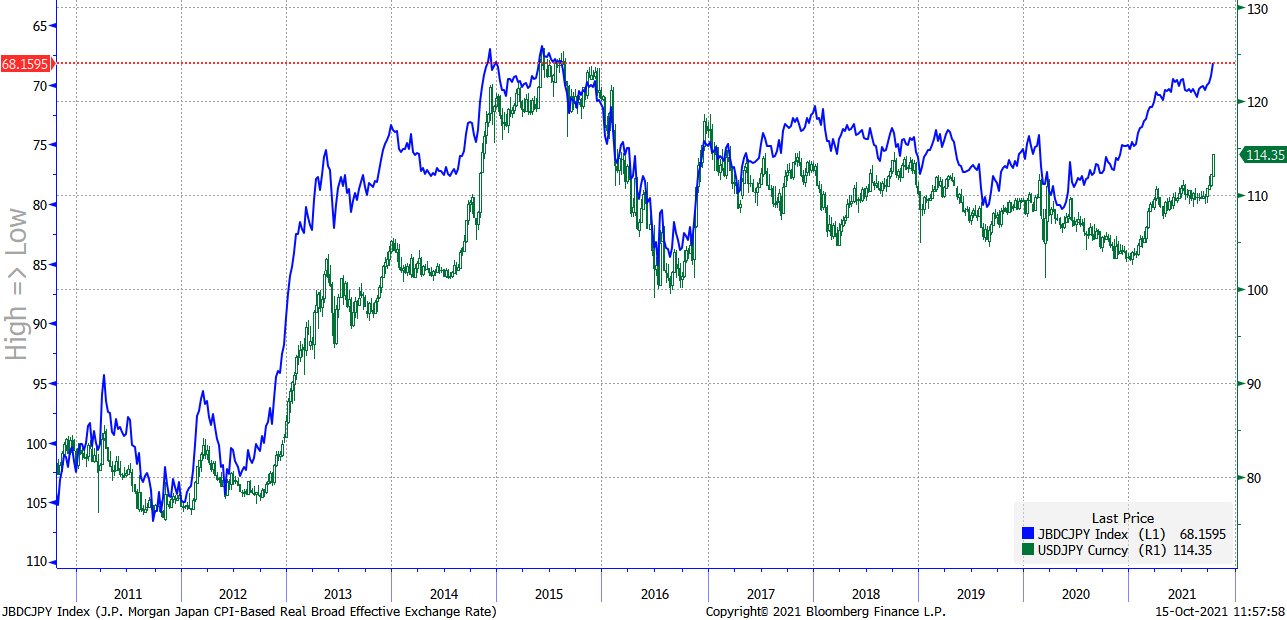

So how low can the JPY go? It is within two percent of the very cheapest level, on a broad CPI-adjusted real effective basis, as shown in the chart below. I suspect it will only firm up on some combination of global credit markets beginning to deteriorate, global yield curves suggesting a recession over the horizon (too early), and importantly, if and when the burst higher in commodities is reversed. By the way, I find the simultaneous rallies in commodities, particularly in energy, and equity markets/risk sentiment entirely incompatible in the medium term. Surging energy prices are often at the root of recessions and we are getting there with the recent price rises if these persist much longer.

Chart: USDJPY vs. JPY REER

The real-effective CPI-adjusted JPY rate is getting toward an historic low (inverted on chart below) as USDJPY soars into the major 114.50 area that capped the action for much of 2017 and 2018. Remember that due to lower inflation in Japan relative to the US, that the “fair value” exchange rate crawls lower over time as long as that remains the case, such that 115 today is similar to 125 back in the 2015 time frame. USDJPY has long history of finding big round numbers sticky psychologically – interesting to see if 115.00 proves similar this time around.

US September Retail Sales and October Preliminary University of Michigan sentiment up today. The US Retail Sales remains in an interesting data series to watch after the crazy surges and retreats of last year and early this year on the series of stimulus checks issued by the US government. We should be mostly clear of that effect, but the “stimulus cliff” means that rising Retail Sales require a confident consumer that is willing to spend out of savings as well as income in the near term. Consensus is looking for a modest month-on-month drop of –0.2% at the headline and +0.4% ex Auto and Gas after the very strong +2.0% gain in the latter in August.

Also worth watching, more than in many years, is the University of Michigan sentiment index, which has stumbled badly in recent months and actually posted a worse reading in August than during the worst initial phase of the pandemic outbreak before bouncing very slightly in September. Is this on popular concerns about rising prices or ongoing covid irritations and even disruptions caused by supply shortages and even vaccine mandates or all of the above? The initial October reading today is expected near unchanged, and possibly most compelling to watch is whether the 5-10 year inflation expectations in the survey are becoming unanchored. In September, this survey rose back to the decade high at 3.0% at the median, while the “average” 5-10 year inflation expectations are at multi-decade highs, save for a brief period in 2008 when oil prices were ramping above 100 dollars/barrel for the first time.

Sterling shakes off BoE dovish push-back. Sterling was unable to fully participate in the full court press against the US dollar late yesterday. While key resistance in GBPUSD above 1.3670 did give way and the pair traded all the way to 1.3734 yesterday, the gains were capped and the pair closed weakly back below 1.3700. Similarly, EURGBP traded to new local lows and down toward the post-Brexit low of 0.8450, but rallied back into the range late yesterday – an interesting sign of weakness despite the supportive backdrop of strong risk sentiment. The culprit was two Bank of England officials (Mann and the very dovish Tenreyro) out late yesterday suggesting that talk of an imminent rate hike is premature, reversing some of the recent rise in short UK rates. The sterling softness has been quickly neutralized today as UK short yields have steadied and on the backdrop of strong risk sentiment, which is probably the most important driver for GBP here anyway.

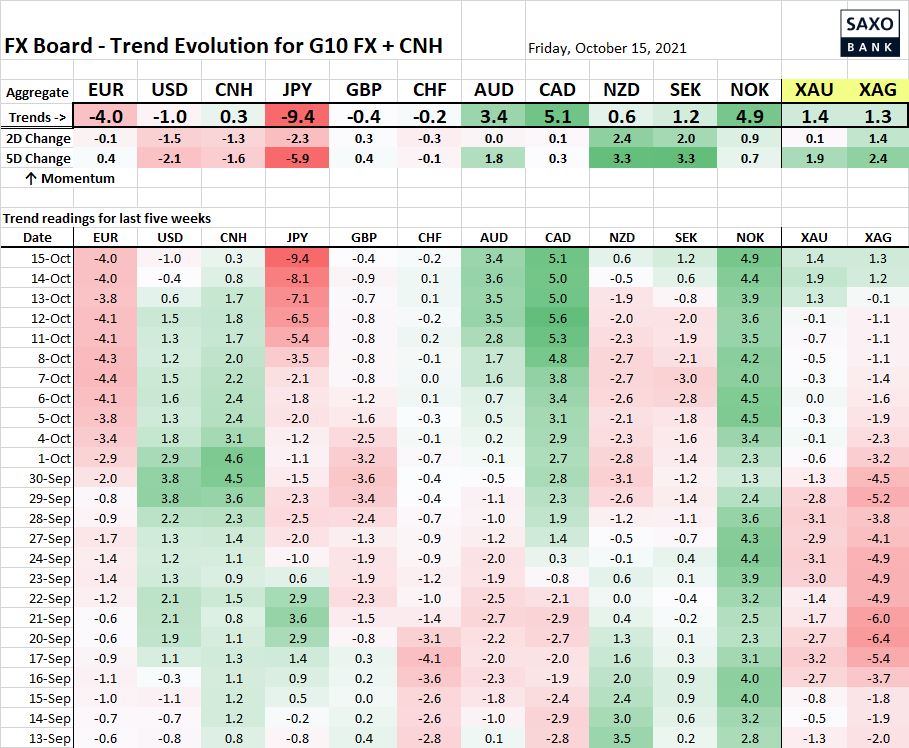

Table: FX Board of G10 and CNH trend evolution and strength

The negative JPY trend has reached a remarkable extreme into a Friday – next week to provide more two-way action as 115 in USDJPY approaches?

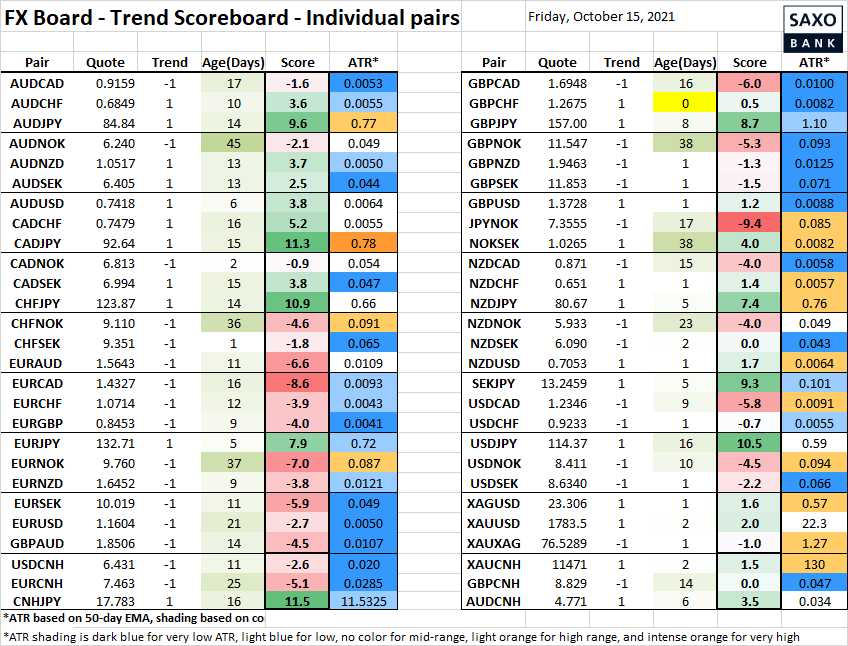

Table: FX Board Trend Scoreboard for individual pairs

Will watch whether flip to negative USD trend in many places holds into early next week – also note the extreme reading for some of the JPY crosses, at 11+ in some cases.

Upcoming Economic Calendar Highlights (all times GMT)

- 1230 – US Oct. Empire Manufacturing

- 1230 – US Sep. Retail Sales

- 1230 – US Sep. Import Price Index

- 1400 – US Preliminary Oct. University of Michigan Sentiment/Inflation expectations

- 1545 – US Fed’s Bullard (non-voter) to speak

- 1620 – US Fed’s Williams (voter) to speak