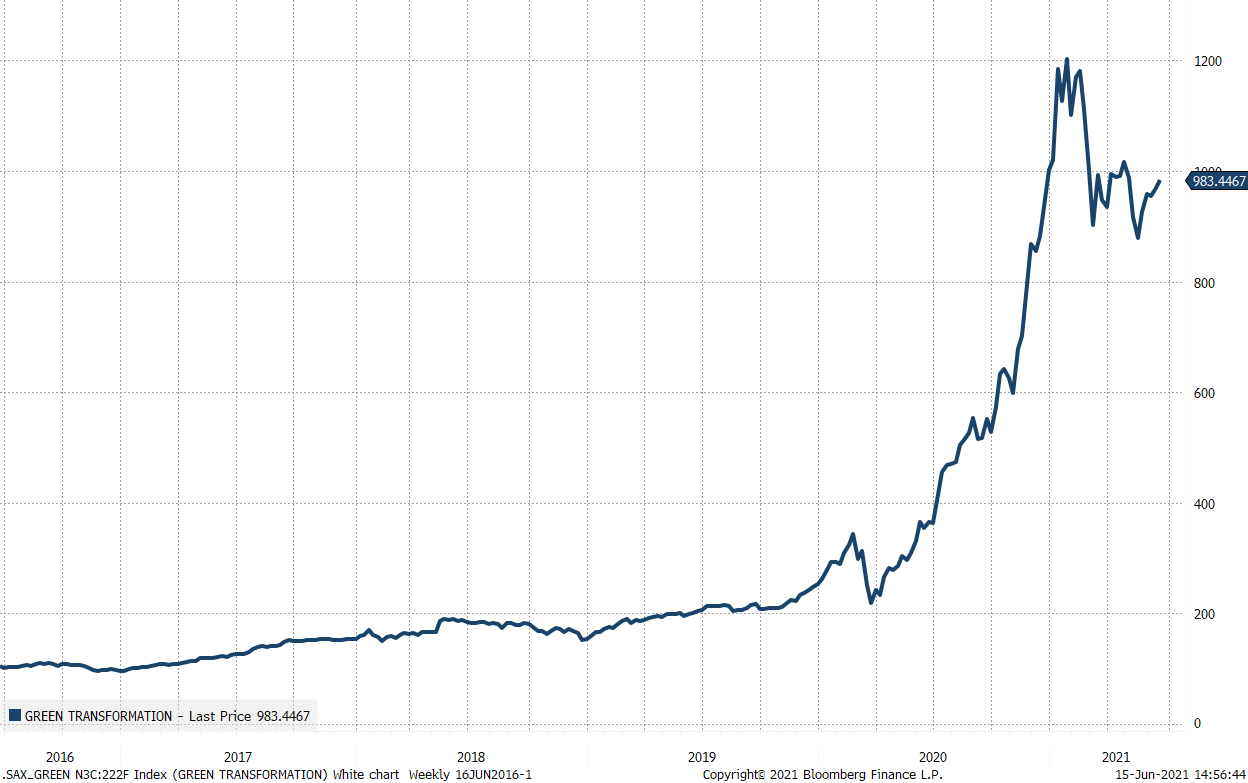

As we alluded to in our Saxo Market Call podcast this morning, our green transformation basket is staging a comeback from the recent lows following a 27% drawdown from the all-time highs. We touched on this theme a month ago in our research note The second collapse of green vs traditional energy where we showed that oil and gas majors had outperformed clean energy companies by 45% from the recent relative peak. What happened in green transformation companies is a bit like what happened during the dot-com bubble. Investors got carried away by the outlook and managements failure to correctly align investor expectations with the outlook (because they have the best insight into a potential disconnection), caused a temporal bubble and subsequent burst.

However, the burst could still be ongoing, but the past couple of weeks we have noticed a strong recovery in green transformation stocks coinciding with lower inflation expectations and consensus moving towards the transitory inflation view. Raging commodity prices were seen as a potential toxic risk source for green transformation companies as they rely heavily on low input costs from commodities. Our green transformation basket is up 12% in the past five weeks. It seems investor demand is coming back as the demand outlook for green technologies looks to be incredibly high in the decade to come as the world tries to decarbonize.

The table below shows our global green transformation basket and in our upcoming Q3 Outlook we will present a European decarbonization list with 40 companies that provide good exposure to the current policy trajectory on decarbonization. As the table shows, analysts are not budging much on their estimates and price targets with the median price-to-price-target being 19% with the fuel cells & hydrogen segment seeing the most aggressive price targets and thus expectations.

| Name | Technology | Mkt Cap (USD mn.) | Sales growth (%) | EPS growth (%) | Diff to PT (%) | 5yr return |

| Panasonic Corp | Battery & energy storage | 28,214 | -10.6 | -25.6 | 23.4 | 62.6 |

| Ganfeng Lithium Co Ltd | Battery & energy storage | 25,266 | 18.9 | 3.3 | 5.0 | 436.5 |

| Albemarle Corp | Battery & energy storage | 19,649 | -7.9 | -24.3 | -1.3 | 126.8 |

| Alfen Beheer BV | Battery & energy storage | 1,911 | 32.1 | 91.6 | 0.2 | NA |

| Carbios | Bioplastic | 526 | 13.3 | -50.2 | 28.5 | 260.4 |

| Avantium N.V. | Bioplastic | 189 | -28.6 | 3.9 | 70.1 | NA |

| Good Natured Products Inc (*) | Bioplastic | 189 | 94.3 | -67.3 | 77.8 | 603.2 |

| Symphony Environmental Technologies PLC | Bioplastic | 48 | 18.7 | 46.4 | NM | 234.8 |

| Aker Carbon Capture ASA (*) | Carbon capture | 1,239 | NA | NA | 25.2 | NA |

| Tesla Inc | Electric vehicles | 595,040 | 38.1 | 2617.1 | 0.1 | 1,317.2 |

| NIO Inc | Electric vehicles | 76,273 | 202.3 | 37.9 | 29.0 | NA |

| XPeng Inc | Electric vehicles | 34,185 | 216.9 | NA | 13.5 | NA |

| Zaptec AS/Norway | Electric vehicles | 354 | 40.4 | NA | 97.9 | NA |

| Blink Charging Co | Electric vehicles | 1,723 | 105.8 | -62.1 | 2.3 | 105.2 |

| Waste Management Inc | Environmental services | 59,191 | 0.7 | -4.8 | 1.4 | 145.0 |

| Veolia Environnement SA | Environmental services | 18,331 | -4.3 | -50.1 | 16.2 | 63.0 |

| TOMRA Systems ASA | Environmental services | 7,933 | 3.8 | 36.0 | -14.9 | 437.7 |

| Cleanaway Waste Management Ltd | Environmental services | 4,179 | -1.1 | 42.0 | -0.5 | 303.1 |

| Plug Power Inc | Fuel cells & hydrogen | 17,373 | NA | -314.3 | 54.5 | 1,646.9 |

| Ballard Power Systems Inc | Fuel cells & hydrogen | 5,304 | -14.2 | -35.1 | 37.3 | 1,201.5 |

| Bloom Energy Corp (*) | Fuel cells & hydrogen | 4,356 | 19.0 | 67.8 | 27.0 | NA |

| NEL ASA (*) | Fuel cells & hydrogen | 3,139 | 12.0 | NA | 45.0 | 820.7 |

| ITM Power PLC | Fuel cells & hydrogen | 2,910 | -82.3 | -37.2 | 55.5 | 1,967.0 |

| Ceres Power Holdings PLC | Fuel cells & hydrogen | 2,712 | 23.5 | -33.4 | 80.7 | 1,016.3 |

| China Yangtze Power Co Ltd | Hydro | 72,582 | 17.4 | 18.0 | 17.8 | 101.1 |

| Verbund AG | Hydro | 31,959 | -35.4 | 27.9 | -19.0 | 573.9 |

| Brookfield Renewable Partners LP | Hydro | 18,871 | 2.5 | -182.8 | 5.0 | 240.0 |

| Meridian Energy Ltd | Hydro | 9,747 | -2.4 | -56.1 | 2.1 | 192.6 |

| Enphase Energy Inc | Solar | 20,036 | 19.3 | 41.3 | 30.0 | 7,245.8 |

| Xinyi Solar Holdings Ltd | Solar | 16,889 | 35.4 | 82.9 | 3.2 | 511.7 |

| Sunrun Inc | Solar | 9,411 | 19.6 | NA | 65.2 | 665.3 |

| SolarEdge Technologies Inc | Solar | 12,623 | -9.6 | -35.5 | 22.1 | 1,067.6 |

| First Solar Inc | Solar | 8,357 | -2.6 | 32.7 | 6.1 | 62.5 |

| Scatec ASA | Solar | 4,409 | 42.2 | NA | 19.9 | 595.1 |

| Orsted AS | Wind | 59,503 | -27.2 | -86.3 | 16.6 | 280.5 |

| Vestas Wind Systems A/S | Wind | 36,738 | 15.0 | -24.4 | 6.3 | 184.1 |

| Siemens Gamesa Renewable Energy SA | Wind | 21,469 | 1.3 | NA | 23.2 | 84.7 |

| China Longyuan Power Group Corp Ltd | Wind | 13,479 | 4.1 | 18.6 | 4.8 | 151.5 |

| Northland Power Inc | Wind | 7,731 | 9.7 | -50.5 | 19.2 | 131.5 |

| Boralex Inc | Wind | 3,315 | 6.5 | 22.3 | 24.9 | 143.0 |

| Aggregate / median values | 1,257,352 | 10.9 | -4.8 | 19.2 | 280.5 |

Source: Bloomberg and Saxo Group

* Peter Garnry has personal holdings in these companies

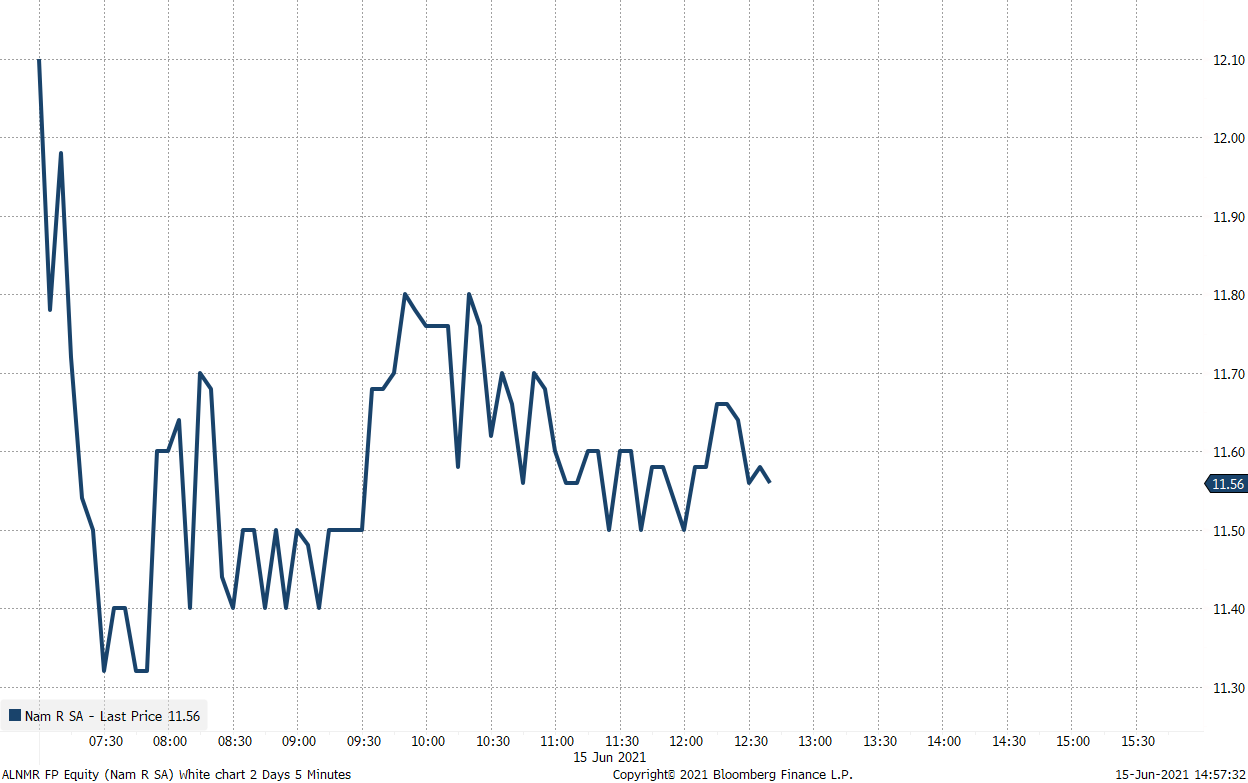

French NamR IPO is a sign of Europe’s “green equity wave”

Today, the French company NamR started trading after a very successful IPO raising €8mn on the Euronext Growth segment in Paris with shares up 14% from the IPO price. The company’s business model is collecting data on buildings and infrastructure to improve energy efficiency combining many different technologies from geolocated data, natural language processing, deep learnings etc. NamR’s IPO is a sign that Europe has a flourishing green technology sector and risk capital available to lift these companies into public markets and accelerate growth through raising equity capital. As we write in our soon to be released Q3 Outlook, the green transformation is Europe’s chance to win a technology vector since the continent lost the digitalisation to US companies.

NamR intraday share price on first day of trading