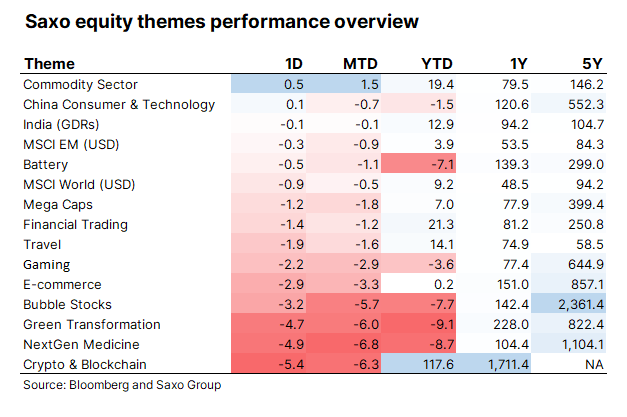

Back in early March, we first noted that green transformation stocks were turning from gold to dust as reality hit investors. While 2020 was a breakthrough year for green transformation stocks as oil and gas stocks were plunging on pandemic driven demand plunge for gasoline and jet fuel. This year, the table has turned with black energy and commodities taking the lead while green transformation stocks have been hit hard being the worst performing theme basket year-to-date down 9.1%. Our commodity basket is up 19.4% this year.

But yesterday’s session was interesting in that interest rate sensitive (those with either high debt leverage or aggressive equity valuations) theme baskets were hit hard, but without a big move in the US interest rates, while the commodity theme basket was up 0.5%. This was, otherwise, the pattern we observed back in February during the correction in Nasdaq 100. It indicates that the market is getting scared about inflation and how it will impact nominal interest rates and operating margins going forward.

Our green transformation basket (see below) has experienced pain across many of the sub-categories but especially the fuel cells & hydrogen segment and solar have experienced the biggest declines as strong performance last year has reversed. Our guess is that investors are beginning to calibrate their views on the green transformation and asking whether they are paying too much for future growth. As Warren Buffett said over the weekend at his shareholder meeting, it takes more to equity investing than a positive industry outlook. In other words, in the end it is all about the quality of the company.

| Name | Category | Mkt Cap (USD mn.) | Sales growth (%) | EPS growth (%) | Diff to PT (%) | 5yr return |

| Panasonic Corp | Battery & energy storage | 28,930 | -13.9 | -55.5 | 20.8 | 57.5 |

| Ganfeng Lithium Co Ltd | Battery & energy storage | 21,932 | 18.9 | 3.3 | 15.5 | 400.0 |

| Albemarle Corp | Battery & energy storage | 18,921 | -12.8 | -27.9 | -2.8 | 154.9 |

| Alfen Beheer BV | Battery & energy storage | 1,634 | 32.1 | 91.6 | 15.8 | NA |

| Carbios | Bioplastic | 409 | 13.3 | -45.0 | 20.0 | 289.6 |

| Avantium N.V. | Bioplastic | 187 | -28.6 | 3.9 | 70.6 | NA |

| Good Natured Products Inc (*) | Bioplastic | 177 | 65.5 | -57.6 | 65.0 | 488.6 |

| Symphony Environmental Technologies PLC | Bioplastic | 55 | 18.7 | 46.4 | NM | 381.1 |

| Aker Carbon Capture AS (*) | Carbon capture | 1,080 | NA | NA | 36.4 | NA |

| Tesla Inc | Electric vehicles | 648,899 | 38.1 | 2617.1 | -8.4 | 1,467.0 |

| NIO Inc | Electric vehicles | 62,149 | 202.3 | 37.9 | 53.3 | NA |

| XPeng Inc | Electric vehicles | 23,247 | 151.8 | NA | 77.4 | NA |

| Zaptec AS/Norway | Electric vehicles | 469 | 40.4 | NA | 50.2 | NA |

| Blink Charging Co | Electric vehicles | 1,479 | 125.8 | -60.6 | 51.3 | 10.1 |

| Waste Management Inc | Environmental services | 59,469 | 0.7 | -4.8 | 0.7 | 157.8 |

| Veolia Environnement SA | Environmental services | 17,818 | -4.3 | -50.1 | 16.1 | 49.4 |

| TOMRA Systems ASA | Environmental services | 7,138 | 3.8 | 36.0 | -7.9 | 361.3 |

| Cleanaway Waste Management Ltd | Environmental services | 4,478 | -1.1 | 42.0 | -8.5 | 302.2 |

| Plug Power Inc | Fuel cells & hydrogen | 12,362 | 55.0 | -292.5 | 122.1 | 1,181.3 |

| Ballard Power Systems Inc | Fuel cells & hydrogen | 4,838 | -14.3 | -26.9 | 75.8 | 1,061.4 |

| Bloom Energy Corp (*) | Fuel cells & hydrogen | 3,980 | 15.3 | 58.3 | 60.3 | NA |

| NEL ASA (*) | Fuel cells & hydrogen | 3,447 | 12.0 | NA | 45.6 | 434.3 |

| ITM Power PLC | Fuel cells & hydrogen | 3,217 | -82.3 | -37.2 | 75.9 | 3,021.8 |

| Ceres Power Holdings PLC | Fuel cells & hydrogen | 2,959 | 23.5 | -33.4 | 62.1 | 1,173.2 |

| China Yangtze Power Co Ltd | Hydro | 70,141 | 17.4 | 18.0 | 21.8 | 97.2 |

| Verbund AG | Hydro | 28,350 | -20.3 | 24.9 | -19.6 | 503.3 |

| Brookfield Renewable Partners LP | Hydro | 15,220 | 2.5 | -182.8 | 15.4 | 211.6 |

| Meridian Energy Ltd | Hydro | 10,169 | -2.4 | -56.1 | 0.3 | 188.4 |

| Enphase Energy Inc | Solar | 17,346 | 19.3 | 41.3 | 53.3 | 6,557.8 |

| Xinyi Solar Holdings Ltd | Solar | 13,334 | 35.4 | 82.9 | 57.2 | 357.4 |

| Sunrun Inc | Solar | 8,845 | 7.4 | NA | 85.3 | 478.7 |

| SolarEdge Technologies Inc | Solar | 11,360 | -9.6 | -35.5 | 38.7 | 880.6 |

| First Solar Inc | Solar | 7,848 | -2.6 | 32.7 | 18.2 | 42.5 |

| Scatec ASA | Solar | 4,090 | 42.2 | NA | 29.6 | 539.5 |

| Orsted AS | Wind | 60,221 | -27.2 | -86.3 | 22.6 | NA |

| Vestas Wind Systems A/S | Wind | 40,660 | 15.0 | -24.4 | -3.6 | 207.3 |

| Siemens Gamesa Renewable Energy SA | Wind | 23,026 | 1.3 | NA | 13.7 | 96.0 |

| China Longyuan Power Group Corp Ltd | Wind | 11,792 | 4.1 | 18.6 | 20.6 | 150.6 |

| Northland Power Inc | Wind | 7,537 | 24.2 | 20.4 | 29.3 | 137.4 |

| Boralex Inc | Wind | 3,140 | 6.5 | 17.0 | 39.9 | 160.5 |

| Aggregate / median values | 1,262,357 | 12.0 | 3.3 | 29.3 | 329.8 |

Source: Bloomberg and Saxo Group

* Peter Garnry has personal holdings in these companies

Despite the recent sell-off, analysts remain bullish on green transformation stocks with a median price target 29% above current price. Today, Vestas representing the second-biggest company in the wind segment published earnings. Vestas missed on Q1 operating income due to Covid-19 bottlenecks with components stuck in the Suez Canal and lower activity generally, but the market was buoyant about the order backlog hitting €44.7bn vs est. €34.1bn sending the shares up 8%. Like so many other companies Vestas is feeling the pressure from rising commodity prices on steel and transportation saying it will begin meaningfully increase prices on wind turbines.

Our view is still long-term positive on the green transformation and is the biggest transformation of our economy since the digitalization started 25 years ago. It will create huge opportunities for investors but over time many companies will not be able to live up to expectations. The biggest risk to the basket is aggressive equity valuations which could become a major headwind for equity returns despite growth if the uptake in revenue and earnings is slower than what the market is currently discounting.