There’s no denying it, reflation is not the dominant theme in Australia’s 1Q inflation data. Price pressures are weak outside of transport and health, and both headline and underlying inflation missed expectations.

Headline CPI rose by 0.6% q/q in 1Q, and the ‘trimmed mean’ core measure lifted just 0.3% in 1Q, decelerating to a record low 1.1% y/y.

Although the data is still subject to various Covid related disruptions, e.g. with the HomeBuilder scheme impacting the price of new dwellings and the Job-ready scheme impacting tertiary education fees, there’s no denying price pressures are subdued. Other issues preventing the visible price pressures mounting across global survey data at the producer level from passing through to end-user prices could be the enhanced ability for retailers to absorb higher costs whilst government subsidies have been in place. This may change with the end of the JobKeeper wage subsidy.

The data were disappointing following the recovery seen to date in both the labour market and the economy, shining the spotlight on the RBA’s challenge to meet mandated price targets and their ability to wind back accommodative policy settings.

The irony being, although inflation is not visible in the ABS’ price indices, house prices, healthcare, education, childcare – Just about everything you want/need – have continued to inflate through the years! In the last quarter, according to Domain, across the nation house prices have risen 5.7%, the fastest pace in almost 18 years.

With inflation well below the RBA’s target band and the central bank having missed their target for a number of years, the RBA remains in a difficult position and rates are set to remain at a historic low for quite some time. The onus is on the central bank to keep their foot on the gas as they (rightly or wrongly) try to guide the economy toward full employment. Although at this point policy is sharply limited by the zero bound. Governor Lowe has stressed the RBA’s inflation-targeting regime now requires actual, not forecast, inflation to be within 2-3% target band before raising rates. This likely requires wages growth in the order of 3%, and a headline unemployment rate tracking 4% and below. The last time unemployment was close to 4% was back in 2007.

At present, the economy is far from full employment or full capacity, significant labour market slack remains, promoting sustained weakness in wages and demand, limiting any underlying inflationary pressures. This was an ongoing problem pre-pandemic.

Headline inflation will rise in the June quarter, potentially recording above 3% temporarily, due to Covid base effects and other one-offs, but beyond that price pressures look set to remain subdued. Unlike the US, could Australia be returning the pre-pandemic slow-flation regime? Certainly, without a concurrent push from the RBA and Canberra combined, it would seem inevitable. To avoid slipping back to the pre-pandemic weakness and promote a self-sustaining recovery, policy must operate in tandem, saving fiscal consolidation for a later date. In an encouraging about face Treasurer, Josh Frydenberg, seems set to follow the offshore consensus on “fiscal dominance” and job creation, with the government shifting their focus toward driving unemployment lower. To full employment and beyond.

Elsewhere, the inflation story is transpiring in spades with clear inflation visible across the commodity complex. From copper to semi-conductor chips prices are picking up, and the list of key commodities that are readily inflating is long a growing – from corn, copper, plastics, and steel, to wood and resins. These higher input costs, increasing the probability of price pass-throughs.

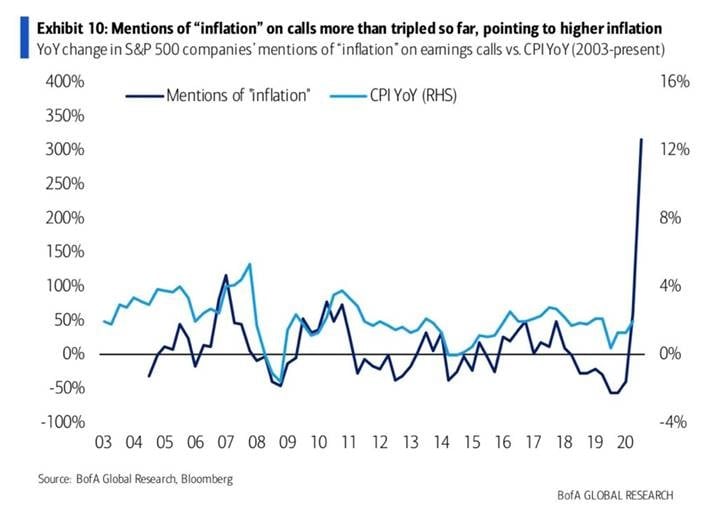

In the US inflation mentions on earnings calls have picked up significantly and several companies are preparing to hike prices in a bid to offset rising input costs. Coca-Cola, P&G, Kimberly Clark Chipotle and Whirlpool are all talking about price increases later this year. The Whirlpool CFO outlining that the company are raising prices between 5-12% to protect its bottom line. Honeywell’s CEO also pointed to these budding price pressures on their earnings call, “inflation is taking hold. There’s no doubt about it. We knew it. We see it, it’s real”.

Against this backdrop we have pandemic fatigued consumers with fiscally bolstered incomes and high savings that are ready to spend. Confidence is on the up, the labour market recovery is underway and household spending expectations are close to all-time highs. Fed chair Powell outlined back in March “You’ll see people reluctant to raise prices.” An expected reluctance that forms part of their “transitory” inflation narrative. However, this is not coming to fruition as cashed up consumers are ready to spend and the impact of rising input costs are beginning to pass through to end-user prices. It seems only a matter of time before official data reflect the trends unfolding across the goods economy and a spectrum of commodities.

These trends in pricing and pricing intentions are confirmed in other data which we have outlined previously. Against this backdrop it is logical to expect higher inflation. Markets have recognised this shift, but it is not sufficiently discounted yet. Despite the Fed playing down inflation and continuing to point to transitory inflationary pressures (a trend that is clearly not transpiring in the real world), for markets, fresh drivers of this emergent trend are likely to be found in coming months as economic data collides with extremely favourable base effects, supply shortages and rebounding demand.