The continuation of the economic recovery has been on full display in recent weeks as survey data continues to accelerate, granted COVID base effects are playing their part, but aside from cliff-edge base effects, an organic acceleration is taking hold as vaccine rollouts gather pace and reopening’s continue. This momentum in the economy and across a host of raw materials and commodities continues to present sustained momentum in pricing intentions and inflationary pressures.

Although the move higher in long dated yields in the US has stabilised of late, we posit that despite the Fed’s dovish rhetoric, this consolidation in yields is far more likely than the inflationary pressures to be “transitory”. With the upcoming US jobs report Friday being a key catalyst, alongside the ongoing inflationary read throughs intensifying across a suite of indicators and input costs set to continue in the coming weeks/months, for the next leg higher in longer dated nominal yields. Job gains well above expectations could quickly shift the range-bound Treasury market.

In the US, although nominal yields remain range bound, breakevens are tracking higher. For 5-year TIPS, the breakeven inflation rate hit 2.70%, its highest since 2008. The 10-year breakeven rate is sitting at the highest level since 2013, at 2.47% and clear signs of inflation are visible across the commodity complex, soaring shipping and freight costs and PMI data. From copper to semi-conductor chips inventories are tight and prices are rising. The list of key commodities that are readily inflating is long a growing – from corn and steel, to lumber, resins and cotton – and survey data is reflecting the pressures of these higher input prices. These higher input costs, increasing the probability of price pass-throughs and goods-price inflation as supply dislocations continue and demand rebounds with the vaccine rollout and concurrent reopenings. Companies are not waiting to see if price pressures are transitory, cashed up consumers are ready to spend, and the impact of rising input costs are beginning to pass through to end-user prices.

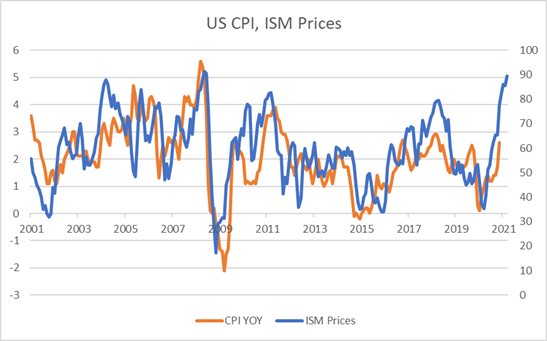

This week the US ISM manufacturing survey’s sub index of prices paid hit the highest level since July 2008, an ongoing indicator of pricing pressures manifesting through the supply chain. Businesses including Nestle, Carters Inc. and Colgate-Palmolive have also added to the list of companies preparing to hike prices in a bid to offset rising input costs. And outside of the US a global manufacturing output prices are sitting at the highest level since 2009 as the sector remains hampered by supply chain delays and input shortages. Although the input cost hikes may be transitory to some degree, companies aren’t waiting, and inflation expectations are growing. Consumers’ expectations for price inflation are the highest in 7 years.

Services

Although these dynamics are yet to unravel through the service sector, we are beginning to see the return of pent-up demand, and the shift from pandemic related goods consumption back to services flowing through to higher costs in the service sector. According to the ISM services update yesterday, prices paid by service providers climbed for a third straight month. The imbalances that have manifested throughout the goods economy likely to be evident in the service sector as cashed up, pandemic fatigued consumers return with a vengeance, with the demand recovery outpacing the return to full supply capacity.

Base Effects

We are now entering the period where we will see higher inflation prints as the “base effect cliff” comes firmly into play. Throughout the corresponding period last year, in the throes of the pandemic as the world went into lockdown, we saw a sharp deceleration in prices. These low base effects mean that if the CPI just holds (no increase) month over month in April (unlikely!) the headline read will still be 3.3% yoy. As supply bottlenecks, increasing input costs, and pent-up demand collide with the base effects cliff it is logical to expect higher inflation is coming and that long-end yields will trade higher in the coming months.

Persistent Inflation

Post the pandemic related disruptions, the case for higher inflation over the medium term rests upon Covid-19 becoming a catalyst for a permanent shift away from the status quo, as fiscal primacy takes the reins. The pandemic has turbocharged many pre-existing trends as well as forging new ones. Under a new inclusive agenda, policies in focus are redistributive and aimed at moderating the rise in income inequality, safeguarding jobs and attempting to stimulate demand/investment and green transformation via increased government spending.

Following the enactment of the latest COVID-19 relief bill, on average the poorest quintile of households will see annual incomes boosted ~20%, generating an increased capacity to consume for those with the highest marginal propensity to do so. Framing this against the backdrop of a structural shift toward fiscal dominance, we will see significantly higher spending and transfers to the individual bringing a lasting step-up in consumption, compounding supply constraints. That is why we see a pivotal regime change in interest rates/inflation, supercharged by the new era of fiscal dominance, green transformation and supply constraints.

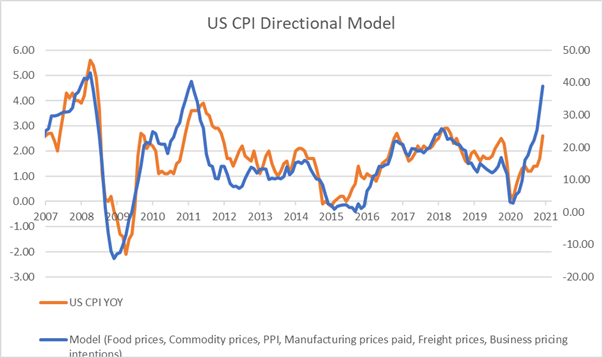

These trends in pricing and pricing intentions are confirmed in other data which we have outlined previously. Against this backdrop it is logical to expect higher inflation. Markets have recognised this shift, but it remains under-priced, by our methodology CPI could be headed well above 3%. Despite the Fed playing down inflation and continuing to point to transitory inflationary pressures (a trend that is clearly not transpiring in the real world), for markets, fresh drivers of this emergent trend are likely to be found in coming months as economic data collides with extremely favourable base effects, supply shortages and rebounding demand. As a result, upwards pressure on yields remains. A lot of the alpha generated YTD has been in response to a global reflationary cocktail and nascent inflation pressures, as the year progresses it will be increasingly important to be on the right side of these trends, reallocating from bonds to commodities and equities – positioning toward higher inflation, commodities, cyclicals, and higher rates.