Earlier this week we launched our next equity theme basket covering the financial trading industry which has been turbocharged by the pandemic, and today we are launching the next basket covering the semiconductor industry.

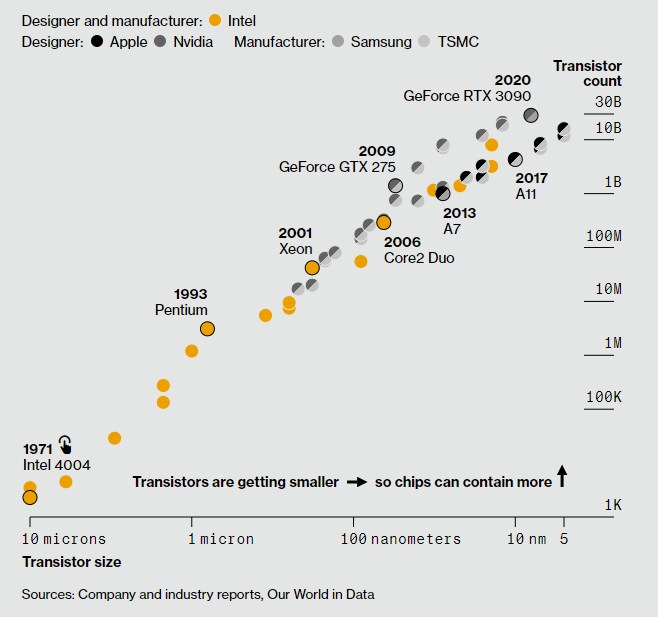

The past six months there has been a worsening supply situation globally in computer chips hitting the car industry hard with Ford Motor losing around half of its production in Q2 due to a shortage of microprocessors. Demand for microprocessors in various industries, graphical processing units for crypto mining and gaming, and memory chips are booming and has taken the semiconductor industry by surprise. The problem is that manufacturing of semiconductors is “harder than rocket science” according to industry insiders and in a recent article by Bloomberg it is laid out why it is so difficult to increase capacity. For one, it costs around $15bn to build an entry-level manufacturing facility due to the requirements for clean rooms (cleaner surgery rooms) and very expensive equipment.

The demand driver for semiconductors over the coming decades following the initial demand of personal and business computing following by data centers will be the trend of Internet of things, which is basically the idea that ever more physical objects in the world will get microprocessors and sensors integration and communicate with the Internet. There is an increasing adoption for instance of trash bins running on solar cells with sensory chip integration sending a signal to a central unit telling a local municipality when to pick up trash. This saves man hours and needless driving for many cities. This is just the beginning and cars will likely be much more connected in the future driving more demand for semiconductors. Finally, the 5G rollout globally will also add to demand over the coming decade. For more insights into the future of semiconductors read the paper Semiconductors – the Next Wave by Deloitte.

Our semiconductors basket consists of 30 stocks with a combined market value of $3trn dominated by TSMC, NVIDIA, ASML, Intel, Broadcom, Texas Instruments, and Qualcomm. The median revenue growth rate the past year has been 7.6% while earnings have grown almost 20% as prices have increased due to the rising demand and ongoing supply constraints. Sell-side analysts are bullish on the industry with a median price target 19% above the current price. Samsung is the largest producer of memory chips, but we have chosen to exclude the company as the main value driver of Samsung is its mobile division. Our theme baskets aim to provide as much pure exposure to the theme as possible. Sony has been excluded for the same reason as Samsung. The basket also contains Mediatek and SK Hynix which are based in Taiwan and South Korea respectively and not tradable on the SaxoTrader. We have selected those two companies because of their size and importance for the industry, and because sometimes tracking the theme better is more important than all companies are tradable on the SaxoTrader.

| Name | Mkt Cap (USD mn.) | Sales growth (%) | EBITDA growth (%) | Diff to PT (%) | 5yr return |

| Taiwan Semiconductor Manufacturing Co Ltd | 598,369 | 25.2 | 36.2 | 22.2 | 498.4 |

| NVIDIA Corp | 359,949 | 52.7 | 72.9 | 13.9 | 1,574.8 |

| ASML Holding NV (*) | 266,671 | 18.3 | 45.6 | 12.7 | 589.4 |

| Intel Corp (*) | 229,560 | 8.2 | 9.9 | 20.9 | 116.5 |

| Broadcom Inc | 181,217 | 5.7 | 19.2 | 15.5 | 268.6 |

| Texas Instruments Inc | 167,758 | 0.5 | 1.7 | 9.8 | 267.6 |

| QUALCOMM Inc | 151,885 | -3.1 | -13.7 | 26.4 | 216.1 |

| Applied Materials Inc | 119,562 | 17.8 | 29.5 | 19.5 | 610.4 |

| Micron Technology Inc | 95,489 | -8.4 | -31.6 | 37.7 | 748.8 |

| Advanced Micro Devices Inc | 94,565 | 45.0 | 91.4 | 28.9 | 2,016.6 |

| Lam Research Corp | 87,140 | 4.1 | 7.7 | 20.6 | 796.1 |

| SK Hynix Inc (***) | 84,153 | 18.2 | 30.4 | 33.3 | 421.6 |

| Tokyo Electron Ltd | 70,209 | 24.1 | 33.1 | 5.1 | 725.8 |

| MediaTek Inc (***) | 60,412 | 30.8 | 71.7 | 33.9 | 550.3 |

| Analog Devices Inc | 56,784 | -6.5 | -6.6 | 17.0 | 211.8 |

| NXP Semiconductors NV | 52,506 | -3.0 | -12.4 | 17.6 | 133.2 |

| Infineon Technologies AG | 50,613 | 6.7 | -12.6 | 23.9 | 183.1 |

| KLA Corp | 47,812 | 27.1 | 16.2 | 17.3 | 412.4 |

| Microchip Technology Inc | 39,215 | -1.4 | 20.3 | 12.5 | 233.4 |

| Semiconductor Manufacturing International Corp | 35,616 | 25.4 | 38.1 | 11.9 | 295.1 |

| STMicroelectronics NV | 32,982 | 6.9 | 8.8 | 31.8 | 568.3 |

| Xilinx Inc | 29,991 | -0.5 | -2.4 | 13.1 | 209.4 |

| Teradyne Inc | 20,741 | 36.0 | 54.9 | 15.9 | 599.2 |

| ASM International NV | 14,895 | 3.4 | -8.9 | 21.7 | 762.9 |

| MKS Instruments Inc | 9,769 | 22.6 | 62.9 | 30.8 | 421.1 |

| SUMCO Corp | 7,270 | -2.7 | -9.0 | 12.0 | 350.2 |

| Brooks Automation Inc | 7,029 | 14.9 | 55.0 | 13.6 | 991.0 |

| SOITEC | 6,319 | 34.6 | 23.7 | 27.9 | 1,453.9 |

| Tianshui Huatian Technology Co Ltd | 5,363 | 3.4 | 45.8 | 39.4 | 172.7 |

| Siltronic AG | 5,174 | -5.0 | -23.0 | 2.0 | 880.6 |

| Aggregate / median | 2,989,016 | 7.6 | 19.7 | 18.6 | 460.0 |

Source: Bloomberg and Saxo Group

* Peter Garnry has holdings in these companies

** Samsung and Sony have not been selected because their semiconductor business is not the dominant revenue driver

*** Mediatek and SK Hynix have been selected despite not being tradable on the SaxoTrader

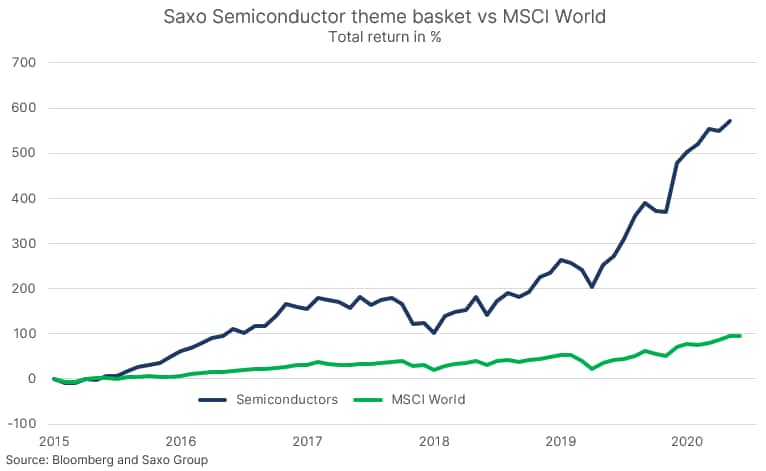

The basket is up 572% since December 2015 translating into an annualized return of 43% making the semiconductor industry one of best performing industries in the world in recent time. Past performance is of course no indicator of future performance and since we select stocks for the baskets on market value, there is always a selection and survivorship bias in the past performance measure. Therefore, investors should not look so much at past performance but instead look at present performance, the quality of the company and their outlook but deciding on which stocks to get exposure to.

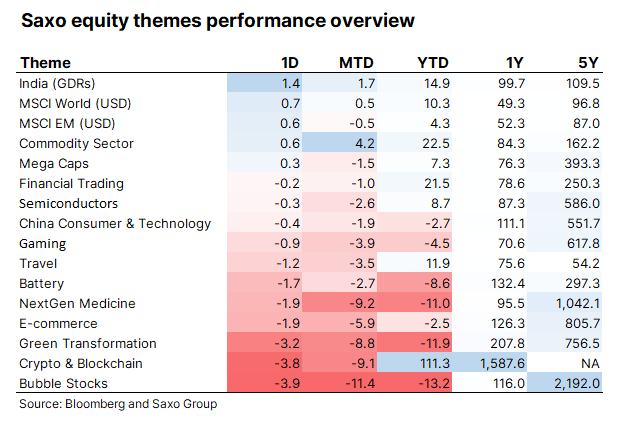

As our performance table on our theme baskets show, semiconductors have had a tough month but are still up on average 8.7% for the year making it one of the better performing themes this year.

Risks to consider

The key risk to the semiconductor theme basket is lower demand or rising input costs from equipment or commodities. The ongoing trade war between the US and China which centers around technology of national security interest, such as semiconductors, could also potentially increase supply constraints and increase costs in the industry as manufacturers will have to geographically diversify their production locations. As most of semiconductors are produced outside the US but purchased via consumer products in the US or Europe, a falling USD and EUR against Taiwanese Dollars or South Korean Won impacts profitability.