Tapering is now consensus within the FOMC: There are eleven on the FOMC who will decide on taper timing. Of this group, the large majority (i.e. Powell, Vice Chair Richard Clarida, Federal Reserve Bank of New York President John Williams and Federal Reserve Bank of Chicago President Charles Evans) look to be advocating late 2021/early 2022 taper. Our baseline is that taper could start from November onwards with a gradual reduction of $10bn per month, with an emphasis on mortgage-backed securities.

Arguments in favor of tapering: We think this is the right time to taper for the following reasons.

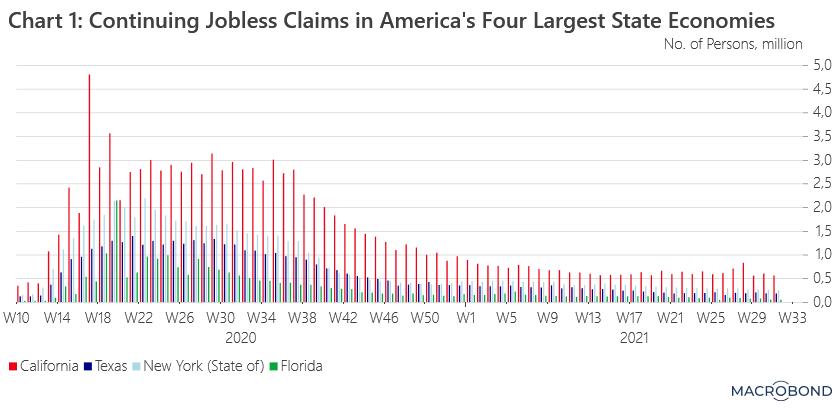

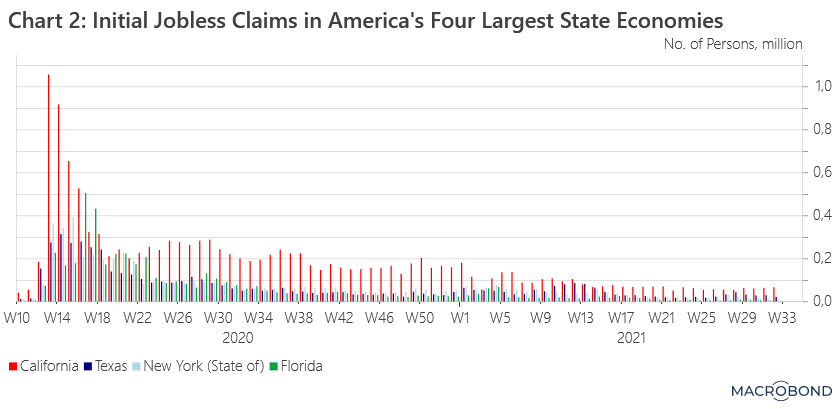

1. The labor market recovery continues at speedy path (chart 1, chart 2). This is the most important signal in favor of tapering, in our view. The latest July non-farm payrolls showed strength across the board. The headline figure increased by 943k in one month and the May and June headlines were revised upward by a total of +120k. The rate of unemployment is also decreasing fast. The official U-3 rate fell to 5.4% in July. It is expected to reach a low of 5.2% in August. The U-6 rate, which is a better gauge of labor underutilization and is followed closely by economists, is down too, at 10.1% in June versus a pandemic peak at 22.40% in August 2020. But what is probably the most impressive is that the involuntary part-time employment, which gives a real sense of people that want to work full time but cannot, was down to 4.48 million, below the long-term average of 5.4 million.

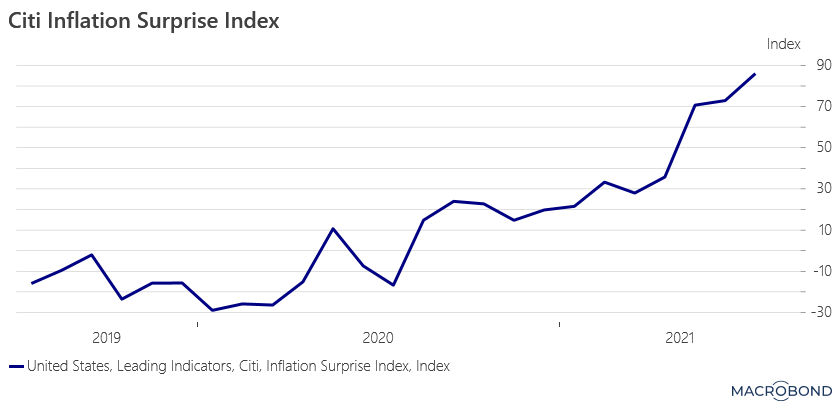

2. There is no reason to run the economy hot longer. According to the latest July FOMC minutes, «most» participants believe that substantial further progress has been made towards the inflation goal. We suspect that behind closed doors there are concerns about the inflation trajectory (see Chart 3). The data support the general FOMC view that currently elevated inflation is likely transitory. But there is a real risk that inflation remains elevated longer than the Fed and the market believe. Some factors pushing inflation up are cyclical (i.e. all the CPI categories impacted by the reopening of the economy, such as hotel fares or used cars). But others are structural (i.e. the lack of investment in fossil fuels/energy which is feeding into import prices and core inflation). A broadening of U.S. price pressures is a real risk to the recovery.

3. With the expansionary jump in fiscal policy, the Fed can slowly withdraw support to the economy without much risk. The current U.S. fiscal stimulus is massive. It could reach up to $4.5tr if completely approved ($1tr in infrastructure package already approved and $3.5tr package for social and greening goals partially approved). With more money flooding the economy in coming years, we can expect U.S. economic activity to stay elevated. In this context, the Fed’s role will mostly be to make sure that overall financing conditions remain broadly accommodative.

Don’t expect much on tapering this week: Powell’s speech is scheduled for 27 August, at 14:00. Market expectations are high. What will be the pace of tapering? If gradual, over how long? Mortgage securities first or Treasuries? And what might happen if inflation keeps accelerating beyond the Fed’s 2.5% per annum expectation? All these questions will remain unanswered. We don’t expect Powell to front run the FOMC or stray too far from the July FOMC minutes. The only real interest might be any emphasis on the Delta variant and how it could impact the U.S. recovery and, potentially, the Fed monetary policy. Last week, Dallas Federal Reserve President Robert Kaplan warned he may rethink his call to taper to start in October due to the variant. Until now, the Delta variant had no material effect on mobility. According to the latest data released by Google, the visits to retail and recreation stores – which are a good barometer to assess the economic impact of the pandemic – are back to the same level as before the outbreak. But a pending question remains regarding how quickly people will get vaccinated, especially in Southern States. If it were without the variant, it is almost certain Powell would have made an official taper announcement at Jackson Hole.

Methodology: Citi Inflation Surprise Index is a real-time model, designed to analyze the accuracy of Wall Street’s inflation forecasts. A positive index value indicates that recent inflation data is higher than the consensus of economists’ expectations. A negative reading denotes inflation data which is lower than expectations.