In this latest edition of Macro Reflections, KVP revisits his long contrarian bullish play on Brazil from late 2020, early 2021. This was a miss on the currency, yet a hit on the equities. We tune back in to an accelerating Hawkish Brazilian central bank in the BCB, that just hiked by +75bp last wk to 4.25%. Inflation is on fire (+8%) as the country faces its worst drought in close to 100yrs. We also take a look at the underperformance of Brazilian Equities (EWZ) vs. the rest of the Emerging Markets (EEM) and touch on the potential complications of Covid, as well as the 2022 presidential elections. VALE & PBR are also touched on.

(These are solely the views & opinions of KVP, & do not constitute any trade or investment recommendations. By the time you synthesize this, things may have changed.)

Macro Dragon Reflections: Brazil, Commodity Rich, +210M pop., +$1.4T GDP, Hawkish BCB, 2022 Political Elections & Consistently Punching Below its Weight. Love it!

Reflections…

Backdrop

- Brazil the country that seemingly has everything:

- 5th Largest country in the world at c. 8.5M square km, including some of the most fertile agricultural lands, as well as priceless tracts of the Amazon (c. 60%)

- Over 210M people, with an economy of over $1.5T & one of the better run, independent central bank in the BCB

- Rich in commodities, from oil to iron ore to agricultural products ranging from soybeans, coffee, sugar to beef & more

- Amazing beautiful people, rich in culture & heritages from all around the world (Europe, Africa, Asia, LatAm)

- World Class Footballers for those into their sports

- Yet at the same time not all as it seems, as its plagued with a number of things – all likely linked to the paradox of plenty (resource curse):

- Abysmal response & co-ordination around the response to the Covid-Pandemic. You had a president who referred to it as the ‘sniffles’… before later catching the ‘sniffles’ himself.

- General lack of sustainable structural reform, that is long overdue that is a function of less corruption, less generous retirement benefits & subsidies, massive increase in the ease of doing business, less protective capital markets & protection of the incumbent few

- The current $1.5T GDP forecast for 2021 is well south of the +$2.6T from 2011. Similar to other countries, debt has been increasing off the back of subsidies to alleviate the effects of Covid to its citizens

- The political landscape is a mixture of part comedy, part horror story & part fatigue in regards to not just the likely run-off candidates in 2022 – Lula & Bolsonaro – but also in any real significant structural reform making it through the government

- One of the biggest wealth inequalities in the world – which for context from Oxfam see’s the 6 richest Brazilian men having more wealth than 100M of its population and the 5% richest Brazilians having the same income as the remaining 95%. Brazilian women are on track to close the wage gap, IN 2047! And Black Brazilian will earn the same as whites IN 2089!

- Brazil is currently undergoing the most severe drought in close to 100yrs & inflation is on fire, with the most recent print clocking +8% for the month of May. This drought not doubt also has structural implication to the supply & hence global prices of a lot of the commodities that Brazil is known for.

Earlier This Year…

- The Macro Dragon was calling for a contrarian long Brazilian exposure at the end of 2020 & start of 2021, both through the Brazilian Real (USDBRL ndfs, or BRLUSD futures) & Brazilian equities (Either Bovespa futures or EWZ country etf, as we are playing the blob here – like any good Macro gal or guy 😉).

- This was off the ‘Worst is in’ Thesis on the view of, “it just cannot get any worse, its about as contrarian as Trump paying taxes, the downside is capped on Brazil given maximum pessimism & we likely are about to embark on a hiking regime from the BCB”.

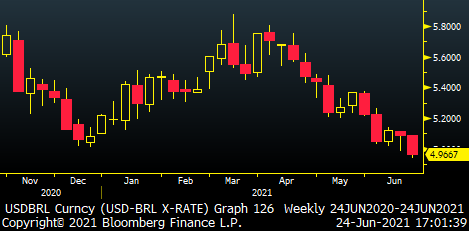

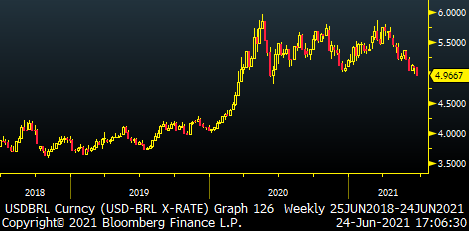

- This did not work out as envisaged on the Brazilian Real (USDBRL) which failed to break the pivotal 5.00 range, KVP’s timing was off here…

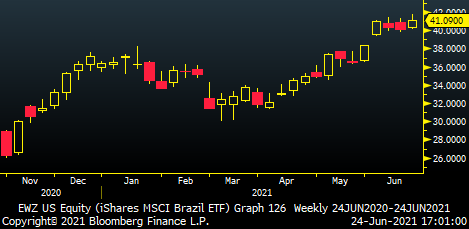

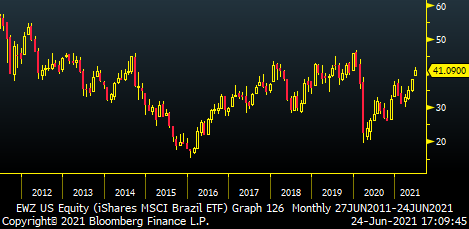

- …yet did play out on the equity side with the EWZ etf continuing to grind higher & after some risk-off around the end of 1Q, we are breaking out to new highs as the back end of May…

Checking Back-In… BCB at 4.25% post a +75bp hike, with another +75-100bp potentially on Aug 3

- We now have a hawkish central bank that has hiked 3x this year, with the latest hike from last wk being +0.75% to 4.25%.

- They are expected to hike by at least another +0.75% in their next meeting, as we now have Brazilian inflation running hot at +8.1% in May & +6.8% in Apr. Its also worth noting next year is a presidential election year & the BCB likely wants to get all their tightening in by year-end so as not to be accused of any political meddling in 2022 (hikes/cuts would be considered a move against/for the incumbent).

- BCB’s next meetings for 2021 are: 4 Aug, Sep 22, Oct 27, Dec 8

- Plus 6 more CPI prints left for 2H21: Jul 8, Aug 10, Sep 10, Sep 9, Oct 8, Nov 10, Dec 10

- The weekly long term chart on the real, shows that if this is a real break of the pivotal 5.00 lvl, the ‘easy’ move is to 4.80, then 4.50 from these 5.00 lvls. With the longer-term move of 4.00 to 3.50 subject to future commodity growth demand, election results in 2022 as well as the monetary policy of both the BCB & the Fed.

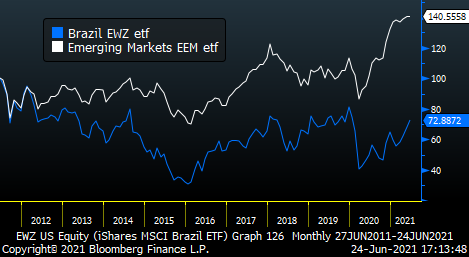

- On the equity side, one needs to pull back a 10yr monthly chart to really see the potential of where we could be going with this break-out higher.

- Its also worth noting that EWZ (Brazil) has vastly underperformed vs. EEM (EM) for the last decade, with EEM up to 140, vs. Brazil down to c. 73. That’s a +70% underperformance

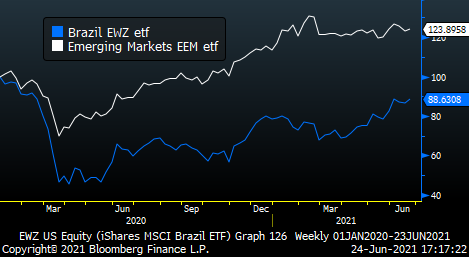

- If one standardizes to the start of 2020 (pre-Covid) there is still a +35% outperformance to EM’s favor (124 vs. 89), leaving KVP considering whether being long EWZ vs. EEM may make sense as a play for the lag in Brazil, proxy to the commodity secular green-tech/infra. cycle, as well as better value, as well as contrarian play

- Naturally risks as always remain: New virus mutation that complicates the pathway out of covid for the country, corruption, 2022 presidential elections, stronger USD given Fed pivot from the Jun 16 meeting (with Jackson Hole late Aug, to Sep 15 expected as next indication of Fed taper).

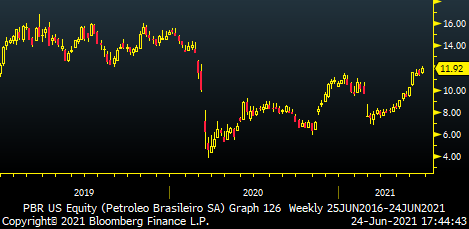

- For those looking for purer stock plays, there are a number of blue chip names (with ADRs in the US) like Vale [VALE, iron ore player] & one of the best Brazilian Macro Minds that KVP knows whispered something about energy player Petrobras [PBR] – which can give one a proxy to long-term oil exposure, Brazil + EM exposure, +30% FCF Yield & at c. $11-12 stock price is still -30% to -25% from its pre-covid lvls of $16.

–

Start<>End = Gratitude + Integrity + Vision + Tenacity | Process > Outcome | Sizing > Position.

This is The Way

Namaste,

KVP