Macro Dragon = Cross-Asset Quasi-Daily Views that could cover anything from tactical positioning, to long-term thematic investments, key events & inflection points in the markets, all with the objective of consistent wealth creation overtime.

(These are solely the views & opinions of KVP, & do not constitute any trade or investment recommendations. By the time you synthesize this, things may have changed.)

Macro Dragon WK #25: All about the Fed (Yawn!), with lower lows in vol & higher highs in the S&P…

Top of Mind…

- TGIM & welcome to WK #25…

- Morning got away from KVP with a few key calls that could not be recalibrated. You know most days you get in the Spaceship ready to take over the galaxy & fight evil 24-7. Other days you get in & its clear as day, you should not be operating any heavy machinery… today is very much the latter…

- …heavy machinery aside, not too much that is top of mind that feels new, fresh or insightful… & that is also part of the process folks…

- … Leonardo did not do a string of Mona Lisa’s… in fact most of his works were unfinished… (tempted to leave it here & press send/publish… someone get this man a NetFlix special!)

- Last wk was about the US inflation print, we got it – it was a banger, with a 5-handle despite an already elevated expectation of 4.7%, yet the MoM beats were nothing like the previous month’s…

- Net-Net the mkt did not seem to care, yet there was a mish-mash of moves into the close off the wk from a cross-assets basis that kinda leaves KVP shrugging his shoulders & eloquently muttering “no idea! What that was all about.”

- The dollar closed the wk higher, despite yields closing lower, equity volatility collapsed with the VIX -4.7% 15.65 (super conducive for the MEME|WSB names), S&P continued to grind to new ATHs with a chart that looks set to break-out. The growth & tech segments continue to recover beautiful since the May 10thish lows, that we were lucky enough to call.

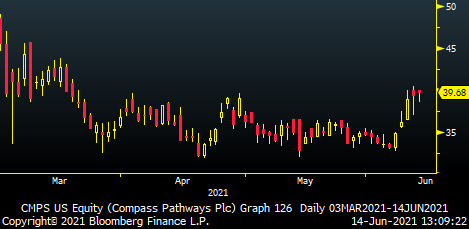

- Compass Pathways (CMPS) clocked +20% last wk. The range of returns on the MEME|Shorted stocks that KVP is tracking did +67% to -19%, with 80% of the 30 names closing in the green for the wk. There are a number of interesting charts there including CMPS, BYND, PTON, ABNB, TY, WOOF, SDC, etc.

- Gold $1877 -0.74% – which has been trading weak over the last 1-2wks – is looking dodgy for the bulls around these lvls (granted two wkly drawdowns of c. -1.3%, after 4 wks of a c. +8% run, does not necessarily a trend, reverse) & one has to also wonder if Copper $453.75 +0.19%, could retrace from these $450-455 lvls to c. $420/30.

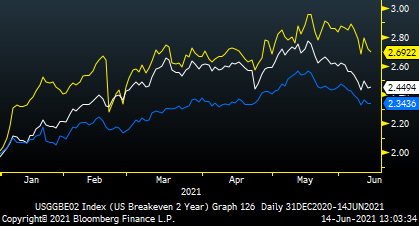

- One potential interpretation from the lower yields & break-evens (move higher in real rates), is that the bond market either does not care about inflation, feels that its going to be transitory, feels Biden may not have enough starch & support in the Dems to get big Fiscal Done, is simply in a retracement phase (we did go from c. 80-90bp to 170bp!), or the Fed is dead until at least end of Aug’s Jackson Hole, so really the Sep 15 meeting.

- Or perhaps a hybrid of a number of those points.

Healthy retracement in Break-Evens across 2-5-10yr horizons

- No new hard views these sides… yet worth noting that summer should see the classic volume dissipate as the institutions get off their desks & gladly venture forth from their small home offices. Which leaves one wondering, low vol, lower volume, advantage WSB|MEME crown… at least until the next string of NFP numbers & the Aug-Sep phase of the year.

- So Fed is meant to be a dude & a paint drying event – which naturally means there is tail-risk to the downside for a number of assets (except vol, dollar, financials, insurers, cyclicals) if for some reason there seems to have been a lot of tapering being discussed and/or there is a big upward adjustment in the inflation forecasts. Again, these are low delta events.

- Cannot help but thing, the more switched on consistently profitable traders are structuring part of their portfolio to benefit from a potential move from the Fed in late Aug to Sep. Whether that is puts & put spreads on US duration or just an etf like TLT, upside calls on the dollar, puts on US10yr bond, downside expression on equities… not yet too sure… but the markets are the ultimate buffet, players choice.

- For now we are in goldilocks lala land… & that by itself creates it own set of opportunities.

- One last thing, Turkey could be fireworks given the CBOT rate decision on Thu – post Erdogan last wk saying rates are again too high. Remember we have had 3 central bank governors in 2yrs, rates are at 19%, inflation is rampant, they used up all their reserves & oh, the vast majority of Turkey’s trade is dependent on the USD. If you think we cannot see another massive cut as was previously the case, clearly you are already forgetting the key lesson from 2020 – that ANYTHING IS POSSIBLE!

- Don’t forget Biden is still on the European tour with chats with Erdogan (Mon) & Putin (Wed) also on the register.

Rest of the Week & Other Reflections

- Econ Data: China monthly growth data, US PPI & RS, NZ quarterly GDP figs

- CB: CHF -0.75% e/p, USD 0.25% e/p, BRL 4.25%e 3.50%p (worth noting CBoR hiked by +0.50% last Fri to 5.50% as we flagged) JPY -0.10% e/p, TRY 19.00% e/p

- Fed Speak: We should be in blackout, no one scheduled to speak yet that could open up post the Wed FOMC statement, press conference & forecasts.

- BoE|GBP: Bailey set to speak on Mon & Tue

- BoC|CAD: Macklem set to speak early Asia Thu / late Americas Wed

- RBA|AUD: Mins out on Tue, Lowe set to speak on Thu

- Hols: CH & AU out on hols today, back in on Tues.

- Dragon Interviews U-Tube Channel for easier play-ability… Check out our recent Crypto Interview with The Spartan’s Group Casper B. Johansen & yes, the increased volume for regulation coming out of the US is actually a massively positive structural aspect for the space. Translation: Regulation of Crypto = Acceptance of Crypto.

–

Start<>End = Gratitude + Integrity + Vision + Tenacity | Process > Outcome | Sizing > Position.

This is The Way

Namaste,

KVP