Macro Dragon = Cross-Asset Quasi-Daily Views that could cover anything from tactical positioning, to long-term thematic investments, key events & inflection points in the markets, all with the objective of consistent wealth creation overtime.

(These are solely the views & opinions of KVP, & do not constitute any trade or investment recommendations. By the time you synthesize this, things may have changed.)

Macro Dragon WK # 28: RBA, ISM Services, FOMC Mins, China Tech (DIDI), 4th of Jul Wkd & SAXO’s 3Q Outlook

Top of Mind…

- TGIM & welcome to WK #28…

- Don’t want to get to attached to the price action & closes last wk, as we highlighted in the Macro Dragon from WK # 27: Noisy Week Ahead with Month/Quarter/1st Half-end plus NFP Friday!

- The US NFP of 850K beat by about +120K from the expected 720K print – market interpretation on the day was higher equities, lower USD, lower yields & higher CMDs. I.e. the number was from the proverbial burglar story of breaking & entering, a.k.a. Goldilocks’ “just right”. Not too hot for a more hawkish Fed, not too cold for a reversal from the Fed.

- So whilst the breaking out of equities to ATHs on BOTH the Nasdaq-100 (FANGs back in force) & the S&P 500, resonates with a low vol environment & still this smooth waters until the 2nd half of the 3rd quarter. Worth noting a lot of these tech & growth charts looking very bullish, even things like Banana, I mean Apple, are breaking out higher.

The moves in the USD, CMD complex & bond market feel a lot more convoluted to KVP at least. Oil cont to be relentlessly strong despite a lack of agreement from OPEC from last wk, with talks extending into this wk.

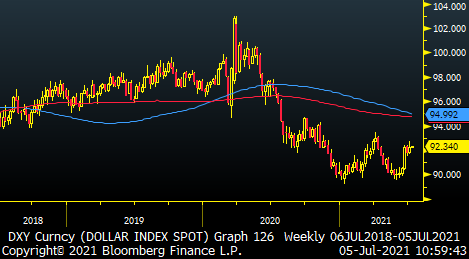

- Currencies as a whole cont to be range bound, yet was still an overall wk of USD strength… & things like BRL almost gave back their gains over the prior 2wks. Incidentally interesting to see crosses like MXN & TRY outperform vs. the EM complex. Despite the USD reversal lower off the NFP print on Friday, generally leaving most USD crosses looking wk on shorter time-frames (daily, hourly, tick)… the wkly DXY chart is not bearish.

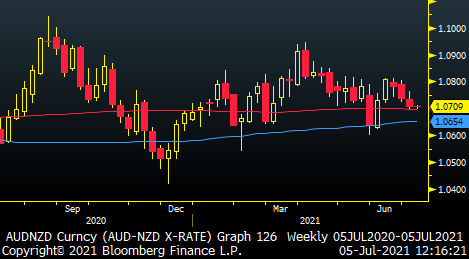

- Not much was standing out from a charts perspective FX wise, yet from a contrarian angle, despite delta being lower than when we flagged it two wks back… upside surprise in Aussie crosses could be interesting given RBA rate decision tmr. Basically one has to weight the hot economy & data, vs. the “here we go again lockdowns”.

- Don’t get me started on the whole hammer & dance – its screaming dislocation… we (countries, policy makers, citizens) all have to walk through the same doorway eventually.

- And its doorway that is not perfect, filled with eventual partial vaccination of +50% to +75% of the population, herd immunity, masks being dropped for those that have been vaccinated (incentives drive people folks, we get what we incentivize for & right now globally we have a lot of incentives working against getting vaccinated) & lastly start re-opening borders for travel for folks with vaccines who have tested negative for Covid (drop the quarantines).

- There is no smooth & super safe path out of Covid, it’s just the distribution of collateral damage that we all have to take… the tough medicine now or later? And whilst everyone talks about the death toll cost, no one talks about the cost that literally billions will face on decades lost (shut businesses & jobs that may never be regained), gaps in education & opportunities, stress, etc.

- Australia & New Zealand’s initial heralded strength of isolation, is now a weakness… After all, if there are no infections on a wide scale basis, what’s the justification for the broader population to get vaccinated?! So it should be no surprise that NZ & AU vaccine penetration has been abysmal – for context, less than 10% of the population in New Zealand have been vaccinated. In Australia, its not much better.

- Covid is like Global Macro or taking responsibility in your portfolio of life… you can run, but you cannot hide forever.

- Anyhow, going back to markets…

- …China tech – which we flagged from last wk & love as a 2H laggard, contrarian & underweighted play – had a great wk, but is running into serious headwinds this morning on the back of the Didi Chuxing [DIDI, think the Uber or Grab of China] listing in the US last wk which is ‘coincidently’ running into investigations on the use of private data from Chinese regulators (have ordered app to be removed from App-stores).

- Personally KVP was surprised that they listed in the US in the first place. Name was up c. +17% in first two days, before falling over 5% on Fri on the news of the investigation. Suffice to say, sound like its due for another -5% to -10% easily when the US is back in on Tuesday.

- So clearly the China Tech space starting the wk on some headwinds & the key risk cont. to be political. If one can get comfortable with that they are likely a long & if not, then one should stay away – unless of course one feels there is a lot more restrictions coming through, in which downside expressions are the way to go.

- KVP still thinks a basket of China Tech ( Tencent, BABA, Baidu, JD.Com, Weibo) likely has a +25% to +50% over the next 6-9 months… perhaps call options are a way to mng the risk, until there is clarity on some names being in the clear.

- US will be back on Tues, following the 4th of Jul wkd.

- Key movers this wk are likely going to be off RBA Tues rate decision, where the delta is low but tail-risk is to hawkish skew (i.e. RBA seeing through the fatigued hammer & stumble).

- US ISM services, worth noting Mon morning has seen a massive miss on China Caixin Service PMIs 50.33a 54.9e 55.1p.

- We also have FOMC mins on Wed, China PPI|CPI & Cad jobs data on Friday.

- Wishing everyone a phenomenal start to the new month, quarter & an even better 2nd half than the 1st. Remember there are always opportunities.

Recent Works to Keep In Heavy Rotation

- Viva la Revolucion! Saxo 3Q Outlook is out – make some time for it, we touch on the green revolution that is here to stay & having a structural impact on European Politics.

- KVP weighs in on a potential Asia investor skew into Europe, looking at the UK as a spin-off from the conglomerate & less effective EU. As well as highlighting China Tech’s underperformance in the 1H21, vs their Global Counterparts especially in ‘Merica.

- Macro Dragon Reflections: Brazil, Commodity Rich, +210M pop, +$1.4T GDP, Hawkish BCB, 2022 Political Elections & Consistently Punching Below its Weight. Love it!

- Where we highlighted the vast underperformance of Brazilian equities vs. their EM counterparts, as well as the Brazilian Real – both of which seem set to be breaking out to big levels of appreciation.

- Dragon Interviews U-Tube Channel for easier play-ability…

–

Start<>End = Gratitude + Integrity + Vision + Tenacity | Process > Outcome | Sizing > Position.

This is The Way

Namaste,

KVP