Macro Dragon = Cross-Asset Quasi-Daily Views that could cover anything from tactical positioning, to long-term thematic investments, key events & inflection points in the markets, all with the objective of consistent wealth creation overtime.

(These are solely the views & opinions of KVP, & do not constitute any trade or investment recommendations. By the time you synthesize this, things may have changed.)

Macro Dragon WK # 35: Does Jackson Hole = Short Gold, Short Bonds, Short CMDs & Short Equities, Long USD & Long Volatility?

Top of Mind…

- TGIM & welcome to WK #35…

- Hope everyone had an excellent, restful & productive wkd – here in SG, where we continue to reopen & are now knocking on hitting +80% of the population being fully vaccinated, it was perk just to be able to be out grabbing some great food & drinks with some inspiring people. Almost felt like a mini-vacation…

- Before we go into why KVP is short gold above $1780 as we kick off the wk or try to answer “Does Jackson Hole = Short Gold & Bonds & Commodities, whilst being long the US Dollar & Volatility?” lets just lay out the wk ahead. (& yes, we will also check-in on Equities, in relation to JH)

Week #35: What’s likely in store?

- Whilst the tailwind themes of the Delta variant, Afghanistan & China assets (Equities, Credit & max uncertainty around regulatory overhang) continue into the last wk of the month, the clear focus from a Macro & Markets perspective will be Jackson Hole. Which kicks off Thu US & extends into the wkd.

- Central Banks: BoK 0.63%e 0.50%p

- There are also minutes out this wk on Thu from the ECB (EUR) & Banxico (MXN) – cons. view there are likely ECB on hold for a while & Banxico turned more neutral post the last two hikes (first of which was a surprise). So any directional skews there could be surprises, yet highly unlikely.

- Small Comment on CBs: Worth noting that Norges Bank meeting last wk, indicated that they are still on for Sep, which would make them the first G10 CB to hike.

“The Committee judges that there is still a need for an expansionary monetary policy stance. At the same time, economic conditions are starting to normalise. This suggests that it will soon be appropriate to raise the policy rate from today’s level”

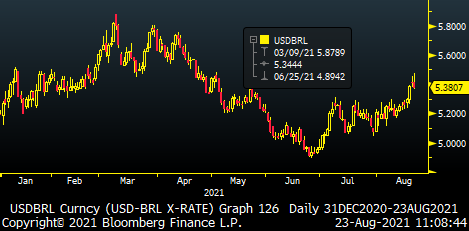

- Yet RNBZ blinking last wk (told you Kiwi skews were looking soft), is likely going to make a lot of market participants hesitant for any positioning going into a potential hike from say Norges Bank, BoE or BoC. Meanwhile you got places like Brazil, where the CB has hiked by +350bp this year & the currency is breaking to ever weaker levels.

- At 5.3807 we are now above the 100D & 200D moving averages. Worth noting BZ inflation was last in at +9% & this is a CB that is still hiking & wants to get its policy lifting in before national elections in 2022.

- GeoPolitics & Policies: US VP Kamala Harris is in Singapore today with a trip to Vietnam later this wk, South East Asia very much the focus on this US state visit. Cont. media & political party posturing around Afghanistan click bate, as well as signal being sort over the noise in regards to China policy (So far equities & credit are firmly in a bear market).

- Econ data: Flash PMIs across the board will be key this Monday. Later in the wk we will have US durable goods, 2nd take on 2Q US GDP 6.7%e 6.5%p & on Fri, the Fed fav. PCE index (core 0.3%e 0.4%p, 3.6%e 3.5%p)

- We’ll have final GDP out of the EZ 1.5%e/p, GER IFO sentiment, as well as money supply & private loan data.

- Holidays: No major bank holidays out there.

So Does Jackson Hole = Short Gold, Short Bonds, Short CMDs, Long the USD & Volatility?

- Well so far, let us use the technical term, kinda’!

- Last wk saw another mammoth gain for the DXY, as the broader dollar index lifted by +1.1% to 93.50. With AUD -3.2%, NZD -2.9%, NOK -2.5% & CAD -2.4% – the CMD currencies – pulled back the most. With JPY -0.2% & CHF -0.2% being the best in the G10 complex.

- EM complex through up some confusion with TRY being the best vs. the USD last wk with TR of +0.8%, whilst MXN -2.3%, BRL -2.4% & ZAR -3.6% secured the bottom of the pack. CNY -0.31% continues to be stable vs. the USD, despite decelerating economy, the zero-covid policy & lockdowns in China, regulatory overhang & at some point a likely accommodative response needs on both the monetary & fiscal policy side. Overall the broader USD EM basket jumped +1.3% to 1158.

- Gold was actually basically flat from a spot perspective at $1781, with silver 23.03 pulling back -3.1% for the wk.

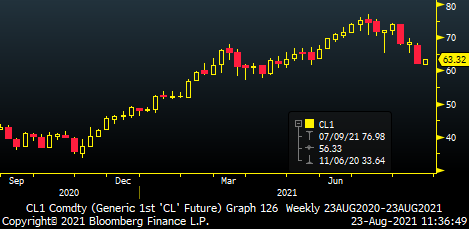

- Oil saw much heavier dent with brent Crude down c. -9% to 62.32. That takes us down about -20% from the c. $77 high set in early Jul. And the chart is look pretty construcive with 200MA at $60.40 & 200WMA at $55.78.

- Naturally the energy equity & credit names have also gotten a beating, the likes of Petrobras $10.10 [PBR] & PetroChina $2.98 [857 HK] were down -7% to -12% last wk alone. Even the XLE $45.89 energy etf closed down -7.1% for the wk. Blue Chip names such as BP 287.85 -5.7%, Shell 1392.4 -4.6% & Exxon 52.74 -7.1% did not fair much better.

- Narrative right here is likely blend between slower China & more challenging delta variant/covid strategy, is pushing back the reopening trade.

- KVP has been a mega bull since pre-elections last year on energy & no doubt about it, the ‘easy’ part of the leg has played out. So whilst still structurally bullish, factors such as JH, debt ceiling, the passing/failing of the $3.5T infra bill & how soon do we get a China policy response will really dictate signal over current noise & sentiment.

- Its worth also noting as we get closer into year end 2021, we get the reverse of winter encroaching on the Northern Hemisphere vs Summer coming into the Southern Hemisphere (Advantage NZ & AU). For now, unless one has a long-only & strategic horizon mandate, stick to the technicals & charts, as fundamentals are being ignored.

- Volatility has clearly been in the party, with the VIX jumping +20% last wk to close at 18.56, yet we did make a wkly high of 24.74 – so do not mistake the mean for the variance, its choppy beneath the surface.

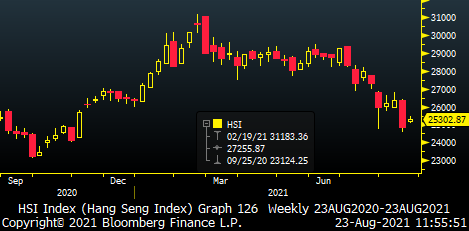

- Particularly with CH & HK equities…. For instance this Mon morning JD Health International (pharmacy chains) is up +11% at c. 64.25, yet the name is down -57% YTD & just -36% in last month alone.

- HSI $24,950 closed last wk down -5.84% we are making new lows – and this after a rare -10% pullback last month (which has only occurred 4% of the time since the start of 2009). So yes we are oversold, there are a lot of cheap, one of a kind businesses out there, likely with excellent yield, but that does not mean the lows are in yet.

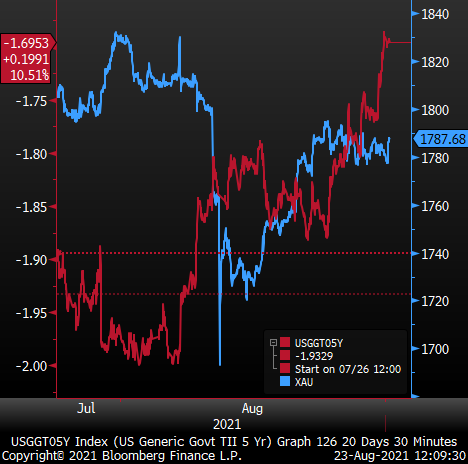

- We are almost certainly going to be getting a signal from Powell on when we can expect the taper program to be announced & started, i.e. an indication of whether Sep 22 is live, or its on the consensus Nov 3 meeting. It’s a path of least embarrassment now for the Fed, if they don’t talk about the taper at JH, then we could see a big crash lower in yields (reversal in the real rates spike we have seen), spike in gold & risk assets in general – all things that could make any tapering announcements that much more volatile later.

- KVP likes to start this wk with a short gold skew, its lagging the big spike in real rates which he feels should be well held going into JH. Would keep this simple short from these $1780/1790 lvl, with a stop at above 1806 / 1812, targeting 1/3 at 1725, 1/3 south of 1700 & let the balance run on a trailing stop of $20-30. Would also adjust the stop loss to entry on tgt one being hit, then to a trailing stop loss of 20-30 on tgt 2 being hit.

- Any massive reversal & breakdown in real rates, i.e. from these -1.70% lvs back to say -1.90%/-2.00% lvls would also result in the closing of the trade. End of the day, this is a play on the gold price needing to move lower to catch up with the spike in higher real rates.

- He also continues to like being long SGD (re-opening play, vaccination almost +80%, upgraded strategy on operating in a covid-world) vs. the likes of EUR, SEK & on the other side of JH, vs. CHF & JPY.

Recent Works to Keep In Heavy Rotation

- Hardy weighs in with a Warning brief: market sell-off risks may be at highest since pandemic outbreak. “We are at the end of the post-pandemic policy cycle and this brings with it the potential for a period of significant transitional volatility. This article is an abridged set of points looking at the evidence that the broader market is at risk of rolling over significantly in coming days and weeks and what investors can do to generally risk market exposure.”

- Viva la Revolucion! Saxo 3Q Outlook is out – make some time for it, we touch on the green revolution that is here to stay & having a structural impact on European Politics.

- KVP weighs in on a potential Asia investor skew into Europe, looking at the UK as a spin-off from the conglomerate & less effective EU. As well as highlighting China Tech’s underperformance in the 1H21, vs their Global Counterparts especially in ‘Merica.

- Macro Dragon Reflections: Brazil, Commodity Rich, +210M pop, +$1.4T GDP, Hawkish BCB, 2022 Political Elections & Consistently Punching Below its Weight. Love it!

- Dragon Interviews U-Tube Channel for easier play-ability…

–

Start<>End = Gratitude + Integrity + Vision + Tenacity | Process > Outcome | Sizing > Position.

This is The Way

Namaste,

KVP