Macro Dragon = Cross-Asset Quasi-Daily Views that could cover anything from tactical positioning, to long-term thematic investments, key events & inflection points in the markets, all with the objective of consistent wealth creation overtime.

(These are solely the views & opinions of KVP, & do not constitute any trade or investment recommendations. By the time you synthesize this, things may have changed.)

Macro Dragon WK #37: Mixed Jobs likely leave Gold overbought, the USD oversold & real-yields with upside. Its now really all about the US $3.5T infrastructure bill that is being kicked around in Congress

Top of Mind…

- TGIM & welcome to WK #37…

- In case you missed the latest Steen Chronicles that dropped over the wkd, have no fear, we got you. Steen’s Chronicle: Pax Americana – beginning of the end or The End?

- A special happy labor day wkd to our Canadian & Americans loved ones, friends, frenemies, clients & even family! Enjoy the long-wkd & the milestone signal that summer is at a close in the Northern Hemisphere. Is Winter Coming?

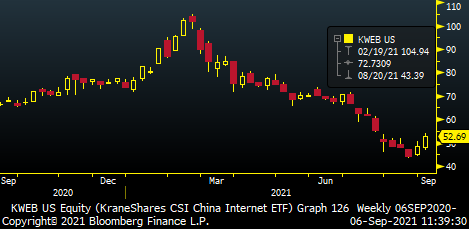

- Folks will be getting back to their desks on Tue in North America & note that YTD the SPX is +21, the NDQ is +22% & China Tech ETF KWEB is -32% YTD.

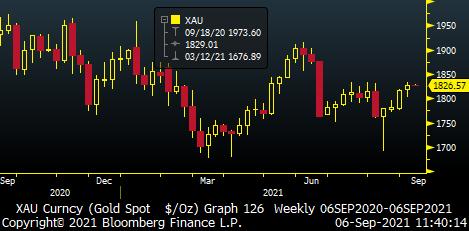

- KVP starts of the wk with the skews of wanting to be short gold (1827 +0.56% last wk), long the USD (DXY 92.035 -0.70%, except maybe on BRL + CLP) &…

- …looking for continued price confirmation on China tech (our VIPs can expect a detailed cut of this contrarian high conviction view that has been bubbling in the Macro Dragon kitchen) – worth noting the formal Saxo House view from Peter Garnry is to wait & if you have to pick something, do so in the consumer side given the lack of certainty.

- The Macro Dragon will do a piece on two significant events from last wk, that potentially bode to the start of a bottoming out in China Tech & the HK equity space – & yes, KVP also thought we were bottoming out in Jul & we kept getting hosed.

- Yet just like our Macro Reflections piece on Afghanistan, Macro Dragon Reflections: Afghanistan – The Return of the Taliban. What if, This Time Its Different? – sometimes one goes in against the crowd & consensus view that is screaming in despair to get out, “the sky is falling”, “it’s the end of the world”, etc.

- One thing about the consensus view, is it is actually right overtime – after all, that is what momentum is, consensus views & more importantly consensus positioning. Yet a consensus view from positions of extreme emotion, is almost never right. Remember Mar/Apr in 2020? Buying the pullback was the most insane thing to do, given what seemed likes maximum uncertainty & peak-bearish sentiment – for the record, at the time the Dragon still felt there was another -30% to -50% to come on the S&P 500, despite the dichotomy on being comfortable that credit had put in a floor (Yes, yes… don’t get KVP started… billions were left on the floor, to be made later no doubt) – yet under the right trade construction it was the exact right thing to do, in hindsight.

- Remember folks, the top & bottom are only known by looking back, yet now & then you need to take a step back, hoover up to 100,000 feet & ask;

“What is likely going to be super obvious in 6-9-12 months’ time when one looks back?” - So US data last wk showed solid holding up of the economy with healthy beat on ISM mfg. 59.9a 58.5e 59.5p & a slight beat on the more important ISM Serv. 61.7a 61.6e 64.1p.

- The Fri-Yay! jobs data was mixed, yet to a very much non-transitory camp.

- Yes epic miss on NFP at 235k a 725k e 1053k r (+110K from last months beat), yet big beat on Avg. Hourly Earnings (AHE) with a +0.60%a +0.30%e/p MoM & +4.3%a +3.9%e +4.0%p. This now takes us to 5 consecutive beats on AHE both on a MoM & YoY basis. The U/R also came in line at 5.2%a/e down from previous 5.4%.

- So what does this mean for Macro? Well it gives the Fed a delay taper to next year card & it almost definitely crushes any chance of an announcement in Sep 22. It also fully turns the focus for the most important factor now being around the $3.5T Infra bill in Congress – that is basically going to be the fulcrum for just how much risk-on / risk-off we get from now into year end.

- Also worth noting last wk surprise as “Suga Suga” a.k.a. Yoshihide Suga, resigned as the Japanese PM , igniting a bullish rally in JP equities. The Nikkei did +5.4% last wk to close at c. 29,130 & is already off to a big start this wk, +500 points on Asia Mon morning at +1.72% to 29625.

- Narrative is folks are underweight, new leadership will unleash more fiscal spending & there is really only upside on the progress on the vaccine front (c. 40% of country vaccinated, expecting it to get to 80% by Oct/Nov). Its going to be hard to replace a once-in a generation leader like Abe (who stepped down end of last year) & the risk is we go back to what was the norm of the rotating door of Japanese PMs. What could be super interesting is if the popular & controversial (to a heavily male dominated society) Governor of Tokyo, Yuriko Koike, throw her hat into the PM race.

- There is a lot of key election risks into yearend folks from Japan, to France & likely most importantly, German – as the latter will see a new regime after 16yrs of one of the all-time GOATs of leadership, Angela Merkel.

Rest of the Week

- US & CA back in on Tue, following the long labor day wkd – interestingly enough, volumes are generally higher on the shorter wk following labor day that the wk before. Which makes sense, as early Sep is when most folks are back on the desk.

- Econ Data: Much lighter overall, we got ZEW surveys out of Germany & EZ block. There is a PPI theme with figs due out of China & US, plus inflation from China – for context 9.1%e 9.0% is PPI skew from China (inflationary to RoW!). For CA, Fri will be key gives jobs data due & also have BoC Gov Macklem speaking on Thu (post Wed BoC mtg)

- Central Banks: All are likely tail-risks to the hawkish side, meaning that is the lower probability event. We got RBA on Tue, BoC on Wed & ECB + BNM on Thu.

- The later is a little more spicey, given the EZ inflation beat last wk (MoM 0.4%a 0.2%e -0.1%p, YoY 1.6%a 1.5%e 0.7%p) & calls from the hawkish camp (read Bundesbank & Northern Europe) to need to start tapering & raising rates at some point.

- Taper will be the focus on the RBA – will they not delay it, worth noting Sydney (23% of AU pop.) has been pretty much in lock-down since their last mtg in Aug 3 – & on the BoC – Who have tapered twice & may be on the fence on current further reductions in bond purchases, given some recent weak data, GDP miss, etc.

- Bank Negara Malaysia will likely stay put at 1.75%, whilst CBR on Fri will continue on their hiking campaign to 7.00% from current 6.50%.

- The Russian Central Bank governor, Elvira Nabiullina – one of the best in the world in KVP’s view – has been very adamant about inflation being real & far from transitory, she has not been mixing up her words here.

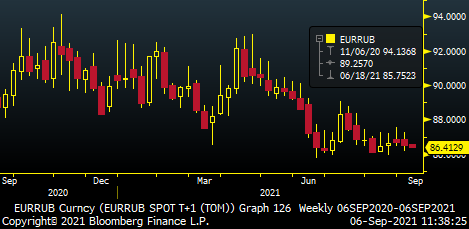

- Perhaps Snowflake Powell should take a page out of her book. And yes, on the Macro Dragon we’ve been bullish RUB fans pretty much since Sep/Nov 2020 (when we got contrarian long on fossil fuels). If they do hike to 7.00%, they should be taking the crown for the highest yielding liquid EM FX out there (not counting TRY for obvious reasons).

–

Start<>End = Gratitude + Integrity + Vision + Tenacity | Process > Outcome | Sizing > Position.

This is The Way

Namaste,

KVP