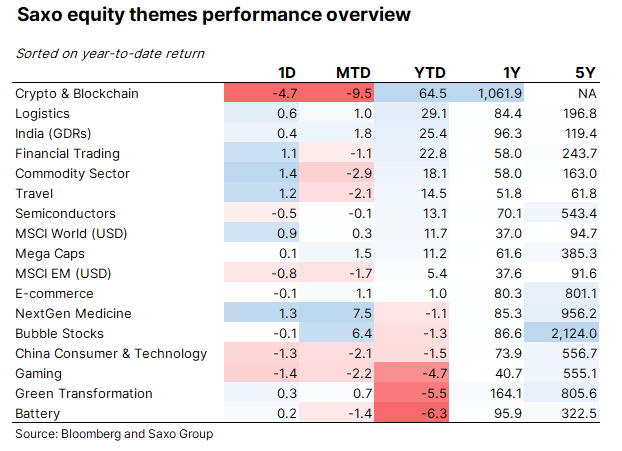

Regularly readers know we have created a lot of theme baskets that we track do understand market dynamics. Year-to-date the two best themes are crypto & blockchain and logistics. A theme basket we have not created yet is listed private equity firms, but if it were a theme basket it would be the third best theme this year up 26.9%. It should not be a big surprise given the low interest rate environment and benign funding conditions for private equity firms, although on the downside the competition for deals has gone up significantly.

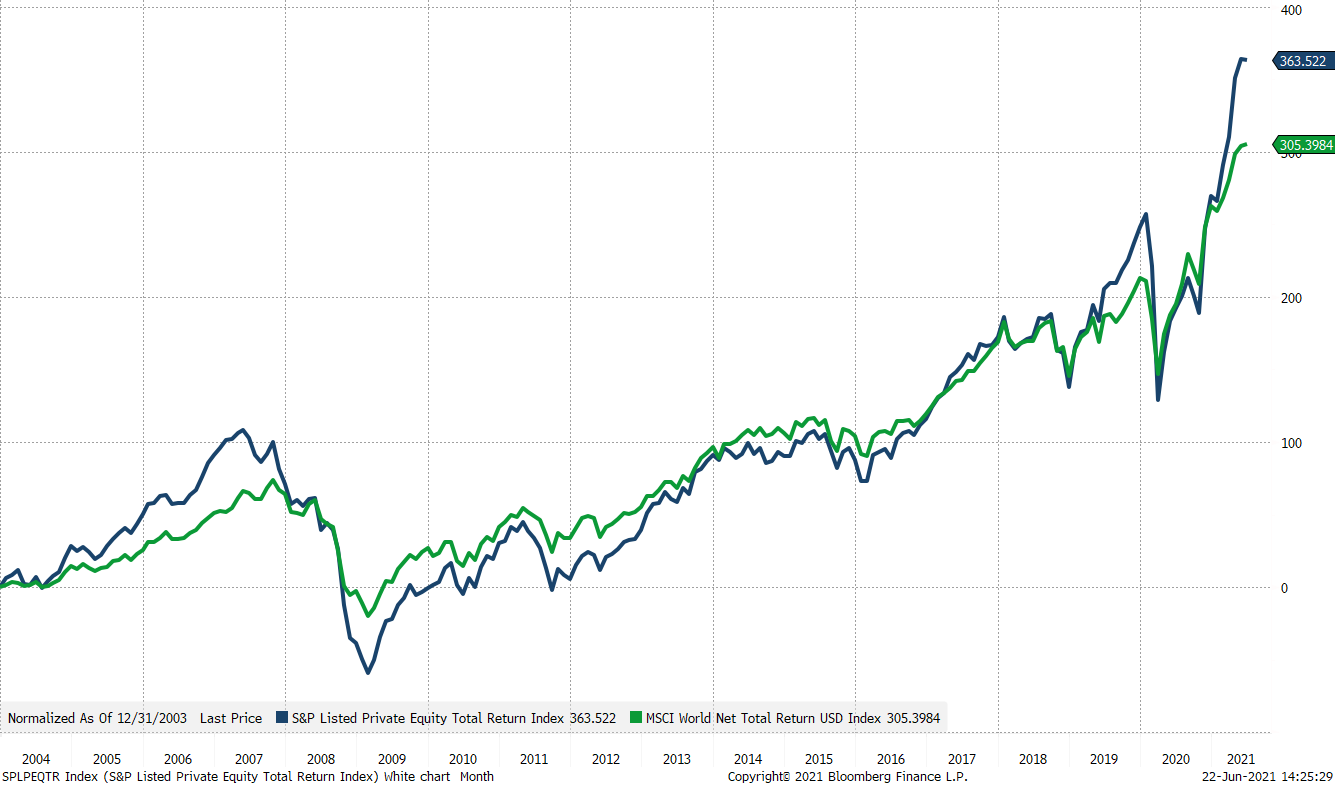

Since late 2003 listed private equity has delivered 9.2% annualized returns compared to 8.4% annualized for the MSCI World Index including reinvestment of dividends. However, the alpha has come with higher risk measured both in terms of variance and drawdowns. As the long-term total return chart above shows, private equity firms have done much better than the overall equity market since the lows in March 2020. Why are private equity firms doing so well and are there any risks?

Long-term returns have been driven by financial leverage, expertise in niche financial markets such as distressed companies, infrastructure, growth capital to non-listed companies, mergers and acquisitions, real estate, and credit, which are parts of the financial markets that many market participants have difficulties accessing. This expertise and network effects within industries, banks, and governments, create alpha for the shareholders. The question is always whether the risk-adjusted returns are that good.

This recent report from Deloitte touches on some few factors. One of the key aspects during the pandemic has been financial assistance to their portfolio companies. With greater uncertainty came harder refinancing terms for many companies and the turmoil in many industries also created deal opportunities. It seems private equity firms have been aggressive in providing financial assistance to their portfolio companies providing them a better foundation to accelerate out of the pandemic. The report also states that the asset under management will grow rapidly over the coming years for private equity firms. In theory it sounds great but from a shareholder perspective it sounds like more capital chasing higher equity valuation lowering future returns. But interestingly enough that is not what we are observing in market pricing of listed private equity.

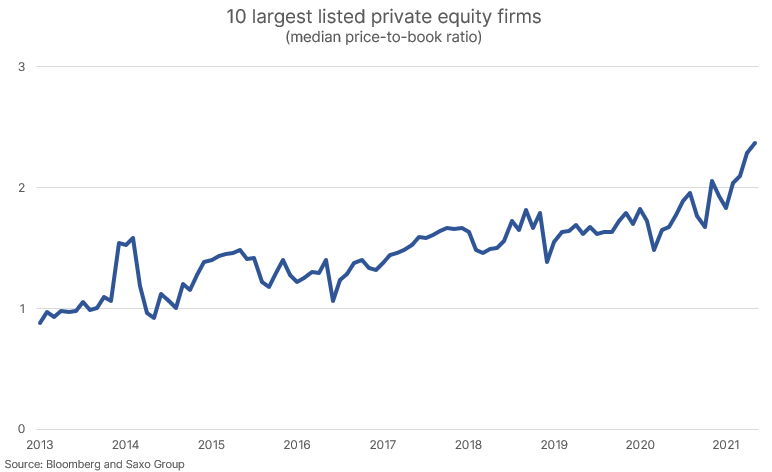

The listed private equity firms in the chart are: Blackstone Group, Partners Group, Brookfield Asset Management, 3i Group, KKR, Apollo Global Management, Intermediate Capital Group, FS KKR Capital, Ares Capital, and Owl Rock Capital

The chart above shows the 10 largest listed private equity firms on their median price-to-book ratio showing that the industry just hit the highest measure price-to-book ratio on record at 2.4x compared to 0.9x in January 2013 and an average of 1.5x over the entire period. Higher price-to-book values can mean many things but the core signal stemming from the Dupont model is that the expected return on equity is going up; this could be because more portfolio companies are becoming digital companies although that is not what we generally observe. Alternatively, the higher price-to-book ratio could mean that there are more intangible assets not showing up on the balance sheet. Whatever the explanation is private equity firms are historically expensive and have high return expectations. They also have considerably financial leverage as KKR’s balance sheet shows and debt leverage has rapidly increased since 2012, but the lower interest rates have kept a lid on interest expenses. In other words, private equity firms have enjoyed the tailwind of monetary policy.

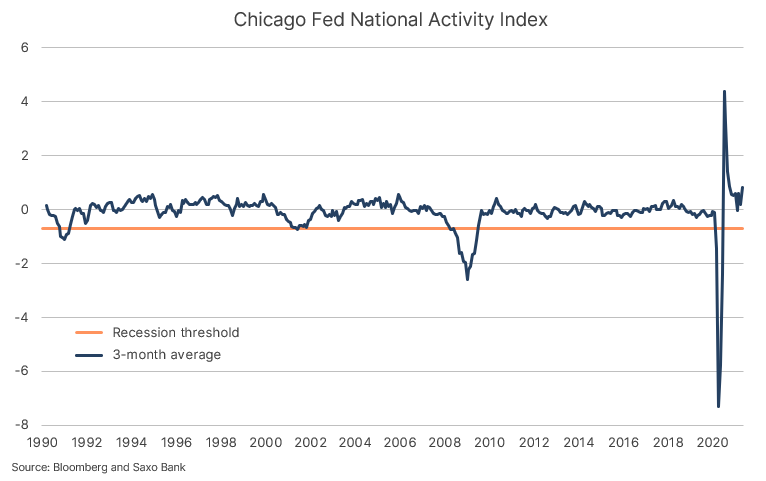

The US economy is the hottest since 1984

The talk is all about inflation these days. While supply side effects are a big part of the current inflationary pressures the demand side is also strong driven by fiscal stimulus. Due to debt saturation in the economy the credit growth cannot be a meaningful amplifier of inflation in the developed world, so it must be direct stimulus from the fiscal side. But how big is the current stimulus?

The broadest measure of the US economy is the Chicago Fed National Activity Index measuring 85 indicators on the US economy with positive values meaning the US economy is growing above trend growth. The three-month average is currently 0.81 which is the highest since 1984, so the US economy is currently expanding at a rapid pace. This aligns well with estimates that the US economy by Q4 will operate well above its GDP potential which at that point will add further to inflationary pressures. The current macro indicators on the US economy also suggest that we will get a very strong Q2 earnings season which starts in three weeks from now.