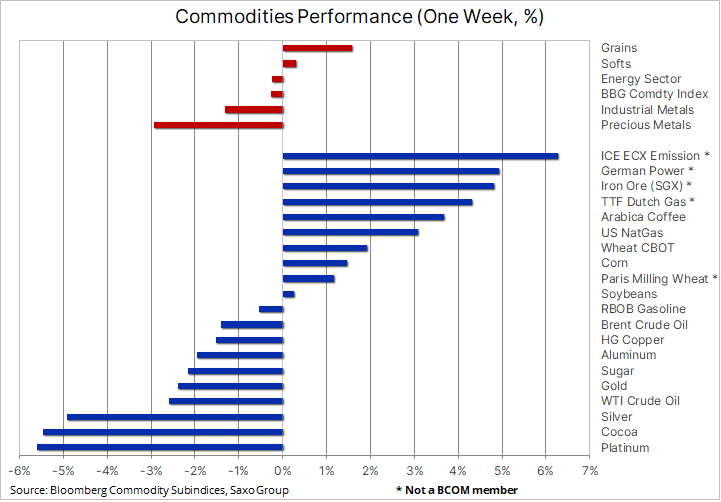

The commodity sector traded lower for a sixth straight week with continued losses in energy and metals, both precious and industrial, being only somewhat offset by another week of gains across the agriculture sector. Apart from recent dollar strength, renewed Covid-related lockdowns in Europe and the risk of a slowdown in China, the world’s top consumer of raw materials, markets were rocked on Friday on the discovery of a new variant of the coronavirus.

The new Covid variant, with a scientific description of B.1.1.529 but no Greek letter yet designated, has been identified in South Africa and observers fear that its significant mutations could mean that current vaccines may not prove effective, leading to new strains on healthcare systems and complicating efforts to reopen economies and borders.

These fears helped send a wave of caution over global markets on Friday with stock markets around the world slumping and US Treasury yields reversing course after rising earlier in the week on increased risk that central banks would speed up their normalization efforts to combat surging inflation. In forex, the Japanese yen jumped and the dollar, which had reached a 16-month high earlier in the week, reversed lower thereby challenging recently establish long positions.

Gold recovered after taking a 70-dollar tumble earlier in week when a break below the key $1830 technical level triggered selling from recently established hedge fund longs. Crude oil slumped following a week of high drama in the energy market which started with the US-led coordinated release of oil from strategic reserves. A move that raised concerns about a counterstrike from the OPEC+ group of nations who are due to meet on December 2 to set production targets for January and potentially beyond.

The agriculture market stayed relative immune to these developments with the Bloomberg Agriculture index hitting a fresh seven-year high led by continued gains in coffee and the key crops of wheat, corn and soybeans. There are individual reasons behind the strong gains recently, but what they all have in common has been a troubled weather year, and the prospect for another season’s production being interrupted by La Ninã developments, a post-pandemic jump in demand leading to widespread supply chains disruptions and labour shortages, and more recently, rising production costs via surging fertilizer prices and the rising cost of fuels, such as diesel. On December 2, the UN FAO will publish its monthly Food Price Index, and following gains during November, the index is expected to reach a fresh ten-year high.

The top performing commodity, apart from coffee, was iron ore which despite weakness on Friday had managed to recover from a recent slump on signs the Chinese steel industry was picking up speed again, thereby driving demand for the most China-centric of all commodities. Over in Europe, the energy crisis continued with punitively high gas and power prices driven up the cost of the benchmark EU emission futures contract rising to a record high, both in an attempt to support demand for cleaner-burning fuels such as currently-in-short-supply gas and to offset increased demand for higher polluting fuels like coal. With gas flows from Russia not yet showing any signs of picking up, the market did find some comfort from the inflows of LNG reaching a six-month high.

Crude oil was heading for a fifth straight week of losses, with the move primarily driven by worries that the new South African virus strain could once again led to lockdowns and reduced mobility. The Stoxx 600 Travel and Leisure Index has lost 16% during the past three weeks with renewed lockdowns in Europe potentially spreading to other regions. Before then, the US coordinated release of crude oil from strategic reserves had driven prices higher in anticipation of a countermove from OPEC+.

The OPEC+ alliance called the SPR release “unjustified” given current conditions and as a result they may opt to reduce future production hikes, currently running near 12 million barrels per month. The group will meet on December 2, and given the prospect for renewed Covid demand worries adding to the assumption of a balanced oil market early next year, OPEC+ may decide to reduce planned production increases in order to counter and partly offset the U.S. release.

With these developments in mind, the only thing oil traders can be assured of is elevated volatility into the final and often low liquidity weeks of the year. Having broken below the July high at $77.85, little stands in the way of a revisit to trendline support from the 2020 low, currently at $74.75.

However, we maintain a long-term bullish view on the oil market, although now potentially delayed by several months or quarters, as it will be facing years of likely under investment with oil majors losing their appetite for big projects, partly due to an uncertain long-term outlook for oil demand, but also increasingly due to lending restrictions being put on banks and investors owing to a focus on ESG and the green transformation.

Gold dropped below support in the $1830-35 area following Jerome Powell’s renomination as Fed Chair which, combined with speculation the White House, has forced a change in focus at the Federal Reserve. Faced with the prospect of more than 200 million people with a job getting hurt by the Fed’s passive action on inflation in order to support job creation for 8 million without, possibly led President Biden and his team to decide to keep Powell on board while at the same time reading him the riot act, demanding a change in focus.

Following the renomination both Powell and Brainard, the new vice-chair, came out showing a clear change in focus. Powell, among other comments, said: “We know that high inflation takes a toll on families, especially those less able to meet the higher costs of essentials like food, housing, and transportation. We will use our tools both to support the economy and a strong labor market, and to prevent higher inflation from becoming entrenched”.

Gold was hurt by these comments as they gave the dollar an additional boost while sending the number of 25 basis point rate hike expectations for 2022 up to three. At the long end, the yield on ten-year notes began challenging key resistance around 1.7%. Adding fuel to the sell-off in gold was data from the US CFTC highlighting the level of speculative gold long positions in the futures market had seen a tripling to a 14-month high before and especially after the early November CPI shock.

These developments saw a sharp reversal on Friday when the virus news broke, thereby supporting a strong recovery in gold back above $1800. Apart from long liquidation having created the space for new longs to enter, the initial recovery was clearly driven by safe-haven demand with crypto currencies slumping by more than ten percent while silver and platinum, given their industrial metal credentials, could be found at the bottom of this week’s performance table. A development that could see gold struggle to make further progress.

From a technical perspective, gold will need to climb through a band of resistance starting at $1816, and only a break above $1840 will signal momentum has recovered enough to trigger a move to a fresh cycle high above $1877. Much will depend on whether current vaccines will prove effective against the new strain, thereby potentially avoiding a bigger economic fallout.