There is a new bond in town, which is getting much attention. I am talking about the joint European debt issued to finance the NextGenerationEU (NGEU) fund. Although it isn’t the first time that Europe sells common liability bonds, the scale at which it is stepping up issuance will bring a much-needed change within the European sovereign space.

Europe’s debt has more than double since last summer as the bloc was trying to tackle the economic shock provoked by the coronavirus pandemic. However, before new bond issuances under the NGEU fund, the total amount of joint debt issued by the European Union amounted to roughly €140 billion. The bloc is looking to issue bonds at a larger scale this time around: € 800 billion, between €150-200 billion a year from now until 2026. This will bring profound changes to the European sovereign space. For the first time in history, it will provide a European yield curve that can be used as a benchmark when pricing bonds in euro currency.

Harmonization of funding costs across Europe will be unequal

The large issuance of European joint debt will provide stability and standardization in the European market by compressing the spread of various European countries versus the Bund. While the bonds will be financed through taxes enforced broadly within the European Union, the disbursements under the NGEU fund will be unequal and directed to countries that need it the most to recover from the Covid pandemic. Italy, for example, will be the biggest beneficiary of these funds as it recently secured €191.5 billion. It is also the country offering the highest yield in the euro area, even above Greece. Therefore, Italy will benefit the most from spread compression. The spread BTP/Bund should tighten faster than any other country, as highlighted in our recently published quarterly outlook.

However, we are less optimistic about French debt. The credit stance of the country deteriorated notably during the past year, with public and private debt soaring faster than anywhere else in Europe. In nominal terms, French debt has surpassed Italy’s, and the country will benefit from a fourth of the package that Italy has secured from the NGEU fund.

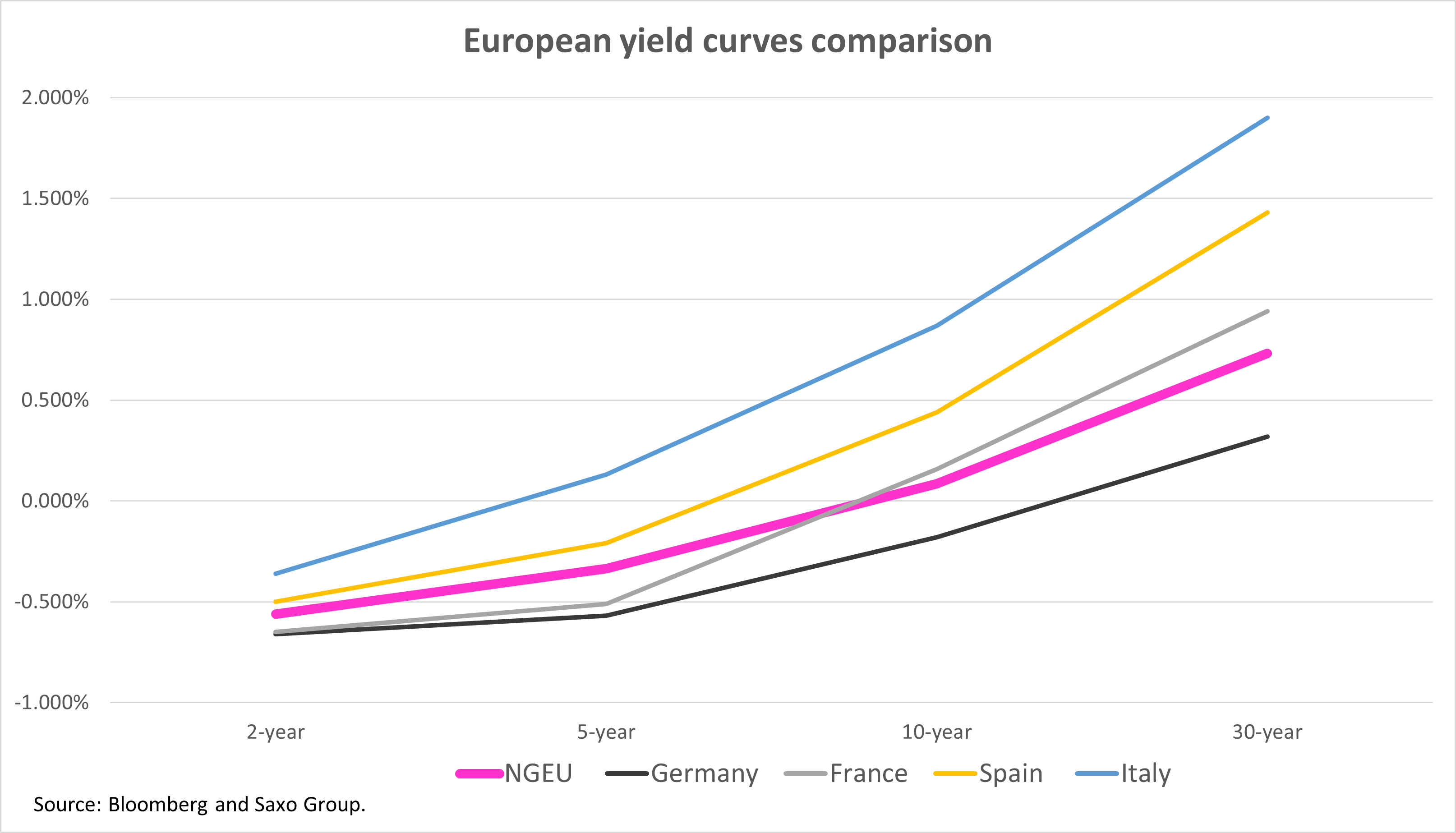

Although France’s credit fundamentals remain much more robust than Italy’s, French government bonds are the second-lowest yielding sovereigns in Europe after Bunds and pay a negative yield up to nine years.

When comparing French government bonds with the newly issued NGEU bonds, it is possible to see that France’s front part of the yield curve prices below Europe’s joint liability debt up to five years. It implies that the market believes that French debt is safer than NGEU bonds.

Research from Goldman Sachs highlights that one of the risks underlying NGEU bonds is that they do not protect against extreme scenarios such as a euro-area breakup. Yet, now that the EU is taking serious steps towards better European integration, it looks that a separation is unlikely to happen. However, those expensive French government bonds in the front part of the yield curve appear to be a market distortion provoked by the ECB’s big pockets. Precisely for the same reason, Greek government bond yields are now below Italy’s.

Expect more NGEU bond issuance and exponential demand for these securities

So far, Europe has issued 5-, 10- and 30-year bonds under the NGEU fund, but it is planning to sell more before August’s summer break. So far, the issuances have been a great success. While demand exceeded the €20 billion 10-year bond sale seven times, the combined orders books for the 5- and 30-year bonds exceeded €170 billion, covering the sale by fourteen times.

Real money will want to buy more of these bonds because it is an opportunity to buy into a safe-haven while getting a considerable pick up over the German Bunds. That explains why the 30-year tranche attached the highest demand in the recent bond sales: it offers roughly 40bps over a 30-year Bund providing a yield of 0.732%.

EU green bonds will be popular and save money for the EU

A third of NGEU bonds will be issued as green bonds. The choice is not random. ESG investments have a longer-term horizon compared to traditional investments. That way, policymakers make sure that the stimulus will be stickier and be there for the next generation, precisely as the fund’s name suggests.

Additionally, the EU would save considerable money by issuing green bonds. The “greenium” spread that Green bonds pay over their benchmark is currently between -2 to -6bps. Over €240 billion of debt represents savings ranging between €48 million to €144 million. The question is whether that greenium can be compressed even further as ESG investors are supply starved and a larger number of participants want to take exposure to the new green European benchmark.