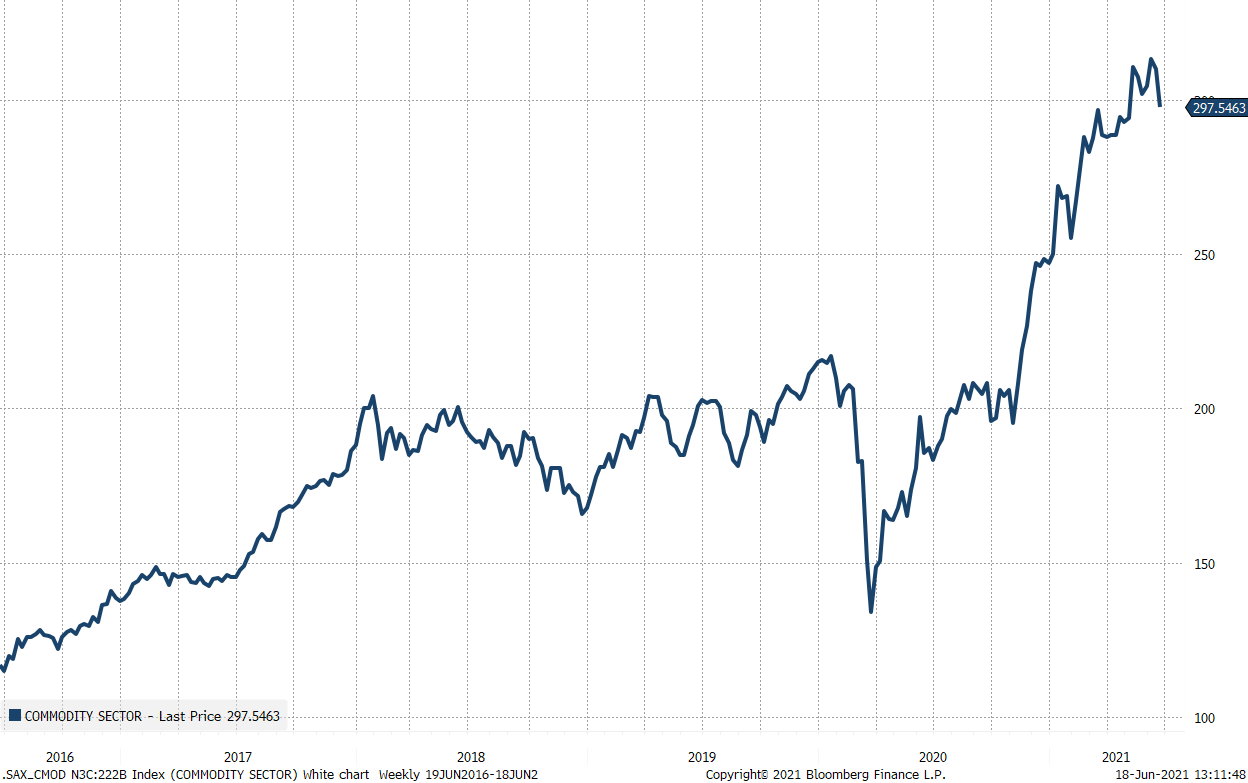

Our commodity sector basket dropped 2.7% yesterday in the biggest single-day drop since September 2020 when the value and reflation trade was still under pressure. The commodity sector is now at the lowest levels in more than six weeks underscoring that consensus is bolstering around the transitory narrative on inflation and growth with the world back to normal by mid-2022. Rising commodity prices have negatively impacted growth in China and reduced profitability in its corporate sector which has forced China to strengthen its currency to alleviate some of the pressures. The Chinese government has recently begun releasing strategic commodity reserves in key industrial metals to take some steam out of the commodity market. This can have a short-term effect, but the long-term pressures will likely remain due to the green transformation in the developed world and excess fiscal stimulus in the US.

5-year weekly chart on Saxo’s Commodity Sector basket

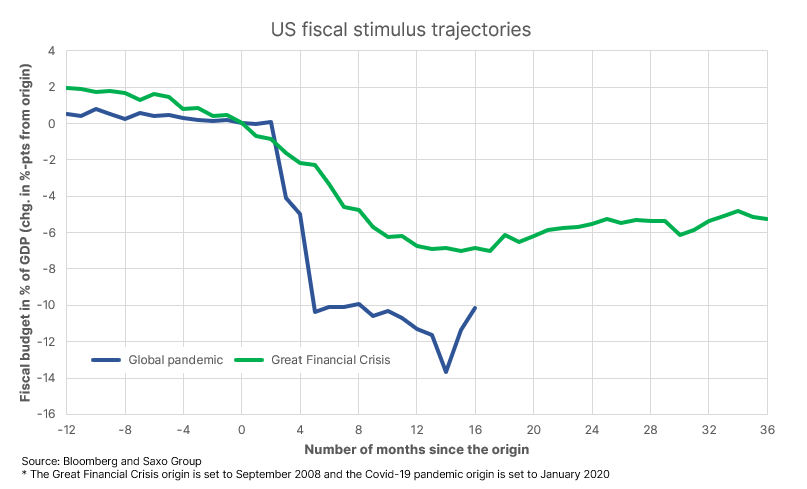

The current reflation reboot is an interesting change in markets because either most market participants and central banks are right and we will return to normalcy within a year, or else this is one of the biggest traps in recent history. We are still leaning towards that inflation will be stickier than expected based on excessive fiscal stimulus for longer driven by Covid-19 response and the green transformation. The chart below shows the current fiscal stimulus change since origin between the pandemic and the Great Financial Crisis. We clearly see the big difference in policy response and the question is whether policy makers overlearned the 2008 crisis.

Even if things normalize and let’s say the fiscal stimulus change this time reaches same level as post-2008 after 20, that is a 6%-pts change from origin, months things are quite different. The comparison is that of -9.2% fiscal deficit by May 2010 compared to -11.1% fiscal deficit by September 2021, but even more importantly these almost identical levels of stimulus will happen with different labour markets. In May 2010, the total unemployment rate in the US stood at 16.7% whereas the current total unemployment rate is 10.2% and declining rapidly. In other words, the risk of excessive stimulus and the economy running too hot is still a clear macro risk and key catalyst for future inflation.

In today’s podcast we covered the breakdown of the transportation sector in US equities and also highlighted Caterpillar’s recent decline with the stock price down 14.2% over just 9 trading sessions, the steepest sell-off since March 2020 during the peak of the pandemic panic. Caterpillar is valued around the average for global equities at 5% free cash flow yield, so it cannot be valuation concerns that have driven down its share price. Since the reflation trade is losing momentum Caterpillar’s move down must be related to the market pricing in lower growth in accordance with the transitory and ‘back-to-normal’ scenario. On the other, this scenario will keep rates lower for longer and extent the demand in the construction sector, so this week has seen many mixed and contractionary signals.