FX Trading focus: JPY trying to steal the spotlight from the US dollar with sudden surge

The most interesting development across market since the knee-jerk reaction to the more hawkish than expected turn at the Wednesday FOMC meeting has been in the US yield curve, with the front-end of the curve (and out to about five years) maintaining the jump in yields on the hawkish surprise, while the 10-year and especially longest end of the yield curve reversed and yields dropped sharply – the 30-year yield even posting a new cycle low. With the JPY sensitive to long US yields a well-established correlation (if an at times inconsistent one), the yen surged yesterday, with perhaps pressure on EM and sharply weaker commodities prices an additional booster to the long neglected currency, which I have felt for some time has been under-appreciated for its real yield credibility. That credibility was on display overnight as the country printed an unchanged headline CPI year-on-year in May. The Bank of Japan, meanwhile, generated headlines for planning a new facility to fund climate priorities starting later this year but was not a factor in the JPY move.

So we have an interesting setup heading into next week as many macro trades that have been popular since pandemic lows have hit a real speed-bump here on the Fed’s change of direction this week. Do we get a follow-on move for a counter-trend extension of this development for a few weeks? I lean toward the latter, given the initial strength of the move we have seen this week, partially contingent on today’s closing levels.

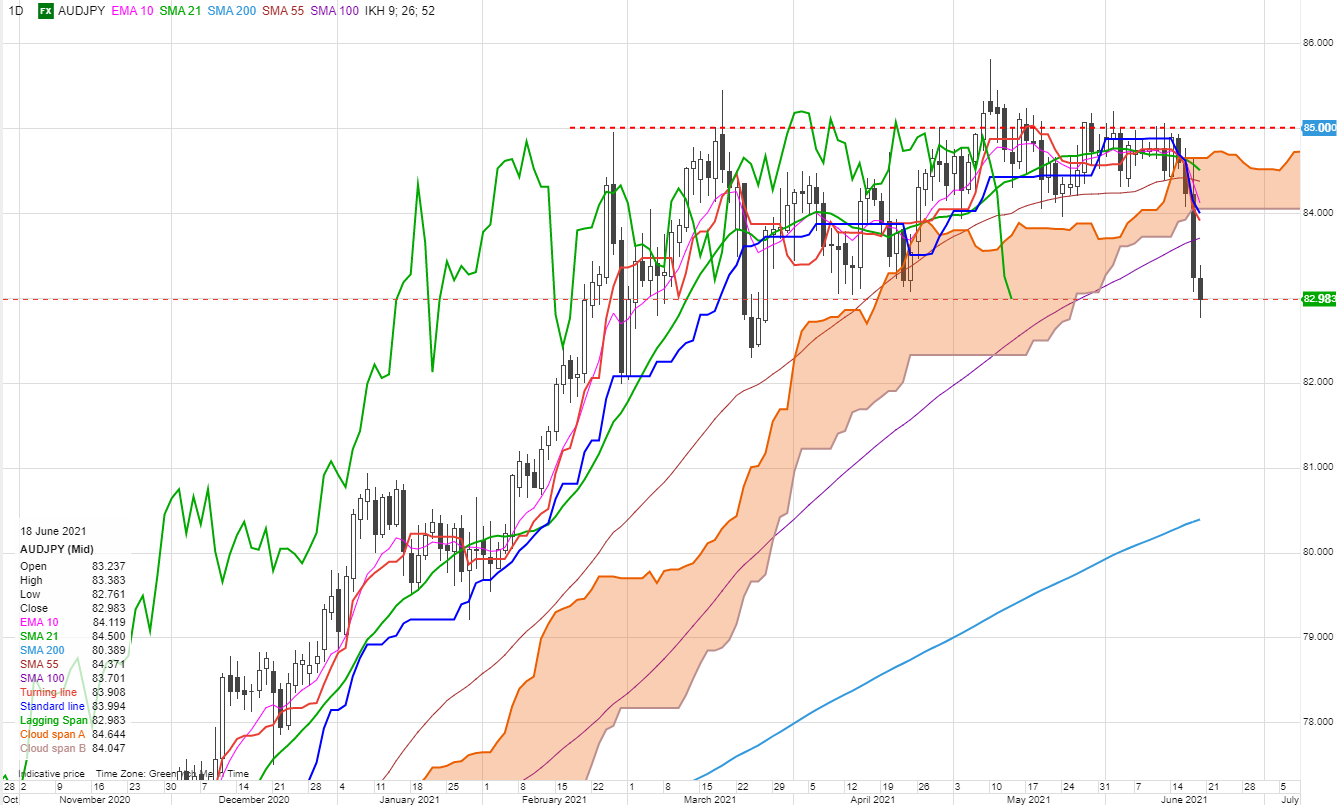

Chart: AUDJPY – that old “risk proxy”

A pretty powerful combination of factors lining up here against the Aussie and in favour of the JPY as the commodity complex has come in for a broad correction here, while long US yields just yanked down to new cycle yesterday despite the hawkish turn from the FOMC this week. A kicker was the reminder overnight in the form of the May CPI data out of Japan that Japanese real yields remain quite strong, while negative yields reign elsewhere. I have been looking for the risk of a JPY back-up for some time, but none unfolded until now, and the move could extend if long yields remain pinned lower and the sell-off in equities broadens (huge divergences yesterday in the US, with the median value stock down and quite badly, even as growth and momentum cheered the fall in longer yields). There’s certainly room for a considerable back-up in the JPY crosses without “breaking” anything, although any such move would likely have to see further downside pressure on long safe-haven yields and a significant further correction in commodities prices. AUDJPY is still within the multi-month range, but the focus looks lower if this move doesn’t immediately back up, perhaps eyeing the 200-day moving average, currently at 80.40, or even more to the downside if the market conviction in the trades that have proven so successful since the pandemic lows are in for a more significant consolidation.

Fed signals to rule them all? It’s interesting to see the USD backing up sharply against nearly every other currency outside of the JPY when we have also seen some solid signals elsewhere this week indicating that other central banks are or will be leaning toward tightening move. Yesterday, a solid jolt higher in Norwegian rates on the back of the Norges Bank meeting indicating a September rate hike and strong hike bias thereafter saw has offered NOK no support, with EURNOK in fact squeezing to a new multi-month high as of this writing. A chunky sell-off in oil amidst a stronger USD is of course a key NOK headwind, but there could be considerable further short-term pain for NOK shorts on the back of this, with EURNOK possibly backing all the way up to its 200-day moving average above 10.40, where I would start to interested in poking at the short side again as long as oil isn’t tumbling below major supports at the time.

As strong as the CAD has been since the April 21 Bank of Canada, it has dropped back very sharply here and is already running into key trend resistance at 1.2350-1.2400. As well, the repricing of the USD higher and AUD lower, together with an extremely strong May jobs report, will allow the RBA to dramatically loosen up its guidance at the July 6 RBA meeting. AUDUSD is looking at closing this week possibly below the range support and 200-day moving average around 0.7555.

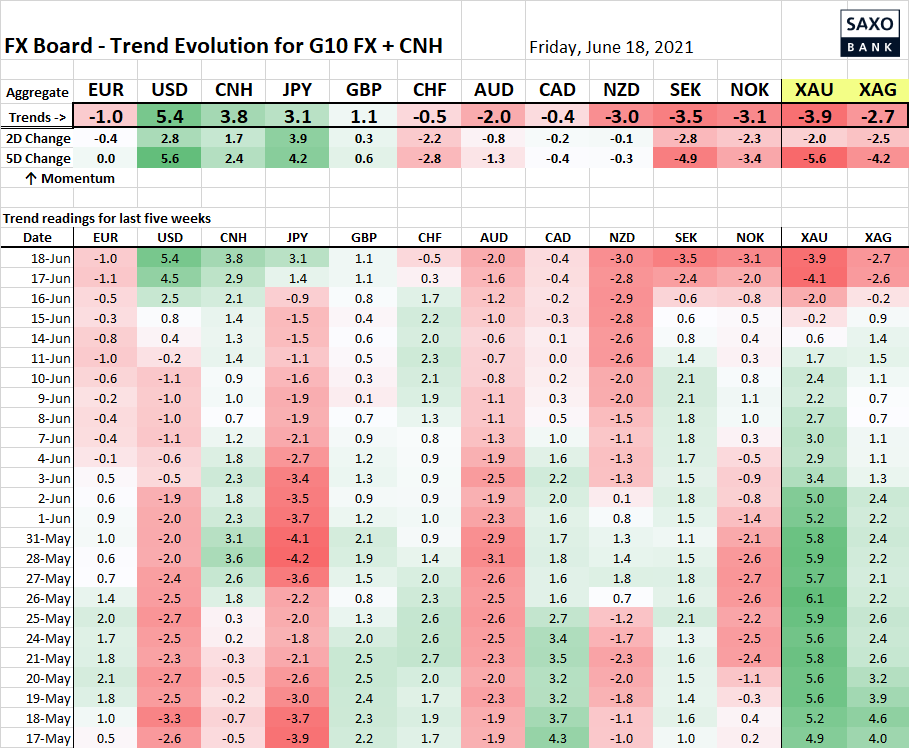

Table: FX Board of G10 and CNH trend evolution and strength

The USD trend has picked up to quite strong levels here, with the momentum showing the JPY playing some solid catch-up. Although arguably most of the JPY move has unfolded on a single day – yesterday – so a bit more progress needed to indicate proper trending behaviour. Note the odd divergence in the CHF and JPY.

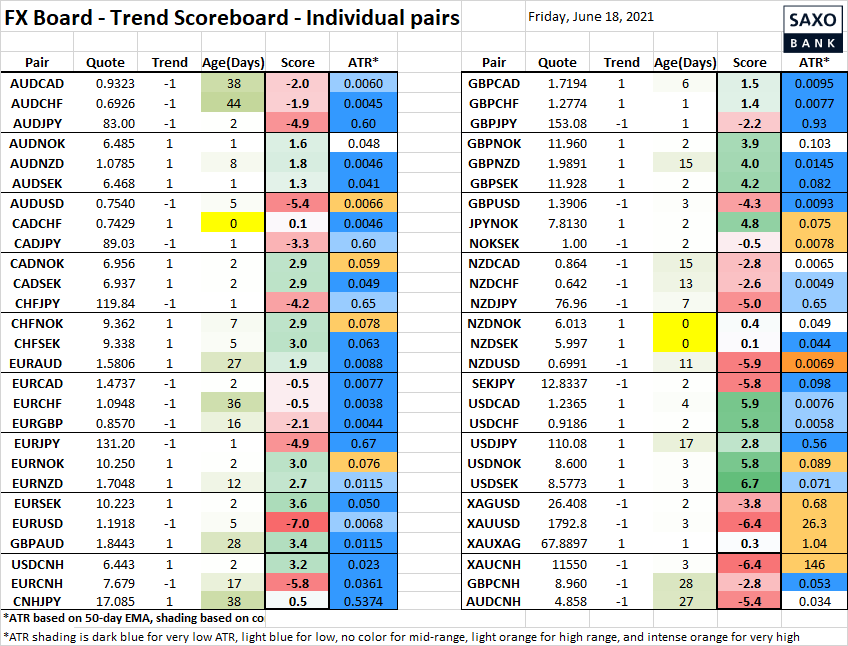

Table: FX Board Trend Scoreboard for individual pairs

Brand new developments of note are not noteworthy here, rather it is the remarkable acceleration in a number of recent breaks that is most interesting, including EURSEK and EURNOK and even more so USDSEK and USDNOK, but also in the JPY crosses that is most worth noting here. Meanwhile, a trend like the EURCHF down-trend is suddenly in danger of reversing if current or higher levels are maintained for another session of two.