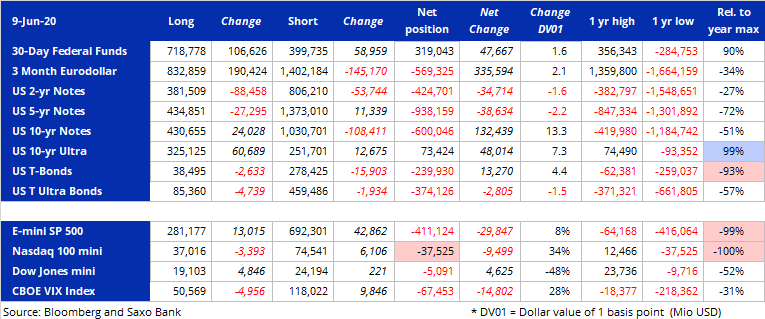

Saxo Bank publishes two weekly Commitment of Traders reports (COT) covering leveraged fund positions in bonds and stock index futures. For IMM currency futures and the VIX, we use the broader measure called non-commercial.

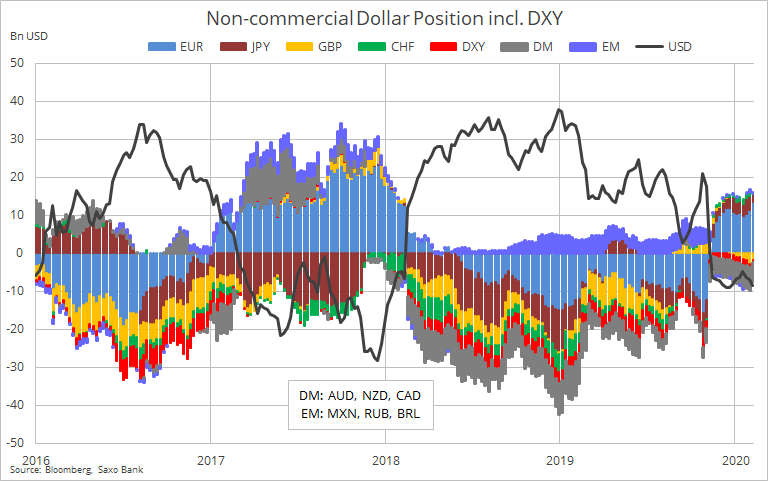

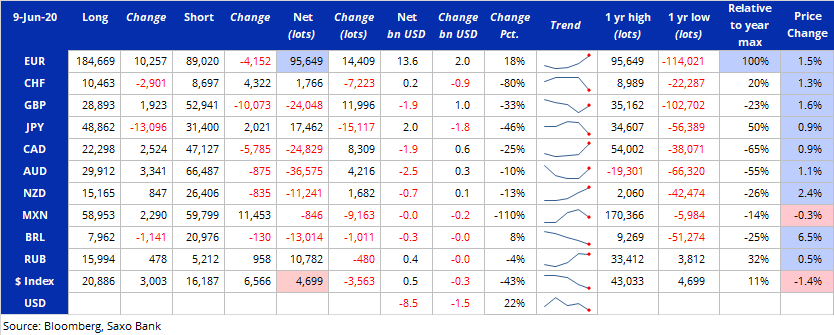

Hedge funds and other large speculators increased their dollar short against ten IMM currency futures and the Dollar Index by 22% to $8.5 billion, a seven-week high. The risk-on seen during the week supported fresh buying of the euro, reduction of yen longs while short positions in other pairs continued to be scaled back.

The change was led by the euro where the net-long reached 96k lots, the most bullish since May 2018. Adding to the rising dollar short was short covering in GBP, CAD, AUD and NZD. The Japanese yen meanwhile was sold with the net-long dropping to the lowest since March.

The Commitments of Traders (COT) report is issued by the US Commodity Futures Trading Commission (CFTC) every Friday at 15:30 EST with data from the week ending the previous Tuesday. The report breaks down the open interest across major futures markets from bonds, stock index, currencies and commodities. The ICE Futures Europe Exchange issues a similar report, also on Fridays, covering Brent crude oil and gas oil.

In commodities, the open interest is broken into the following categories: Producer/Merchant/Processor/User; Swap Dealers; Managed Money and other.

In financials the categories are Dealer/Intermediary; Asset Manager/Institutional; Managed Money and other.

Our focus is primarily on the behaviour of Managed Money traders such as commodity trading advisors (CTA), commodity pool operators (CPO), and unregistered funds.

They are likely to have tight stops and no underlying exposure that is being hedged. This makes them most reactive to changes in fundamental or technical price developments. It provides views about major trends but also helps to decipher when a reversal is looming.