Did you know that people that identify safety vests and exits are more likely to survive adverse situations?

In this analysis, we’ll try to explain what does stagflation mean for your investments. Even if this scenario does not materialize, we believe it is necessary for investors to consider it and to identify safety vests and exits well ahead of time. Therefore we determine what assets are detrimental to your portfolio and which can be helpful in such a context.

Stagflation might be the real challenge ahead for markets as elements point to the fact that it may take over the reflation trade.

While the reflation trade sees a strong pick-up in economic growth and inflationary pressures, stagflation sees higher inflation without much real growth. So far, the economy seemed to strengthen together with inflationary data. However, the nonfarm payroll miss last week and strong CPI readings today suggest that inflation may pick up before the problems hindering growth are resolved.

This changes investors’ approach towards their investments completely because it means that economic growth might not be strong enough to sustain record high asset prices. Thus valuations will need to correct according to the real economy’s activity. Otherwise, nominal growth (real growth plus inflation) may continue to rise through inflation, eroding value from asset prices.

Assets that will strive amid stagflation:

- Inflation-linked bonds could be helpful as they pay the inflation rate. Right now, the majority of TIPS and European inflation linkers are pricing with a negative yield. This happens because the market’s inflation expectations are well above the yield offered by nominal government bonds. Albeit negative-yielding assets are a turn-off, they remain a pure inflation play that will hedge one from inflation risk. Indeed, if inflation will not pick up, investors will pay a small yield, but if inflation picks up, they will receive a coupon equal to the CPI index.

- Higher-yielding nominal bonds will provide a buffer against rising inflation and interest rates. This is a point we have been vocal about, and we continue to stress. Unfortunately, only junk bonds and emerging market bonds provide a yield high enough to hedge against this risk. We like junk bonds the most because they are closer to a recovery in the US and Europe. Emerging market debt, especially EM sovereign bonds, remain vulnerable to a delay in vaccinations and local accommodative monetary policies that will inevitable devalue their currency. The latter is a critical issue in light of the exponential amount of hard currency debt that these countries took in the wake of the Covid-19 pandemic, raising important questions concerning the sustainability of their debt.

- Commodities. Despite the economy is not growing and inflation continues to rise, there will always be a need for commodities. Yet it is important to highlight that while in the short term inflation and commodity prices are correlated, in the long run, higher prices will depress economic activity, pushing commodity prices back down.

- Consumer staple stocks. Staples will be a good bet because they are necessary to live despite high inflation. Stocks that are sensitive to increasing interest rates, such as those that my colleague Peter Garnry calls bubble stocks, are most likely to struggle.

What to avoid at all cost in the bond market:

- Nominal bonds offering low yields, such as sovereign bonds. This is what makes this cycle utterly different from others in history. While in the past nominal yields were giving a buffer against rising inflation, now they are not anymore a reliable source of income. Although accommodative monetary policies might keep interest rates low for longer, the risk to hold these securities outweighs the benefits.

- Duration. Since the global financial crisis, the economy has been characterized by a deflationary environment and easy monetary policies. This made it possible for assets with long duration to perform quite well. However, since yields have started to rise in the US and in Europe, assets with long maturities have begun to lose value quickly. The more yields will rise, the more bonds will be decimated.

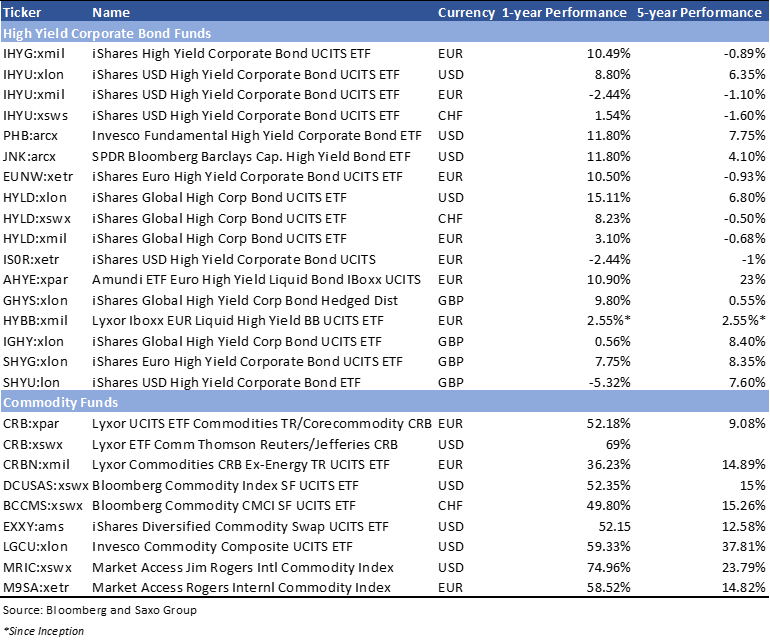

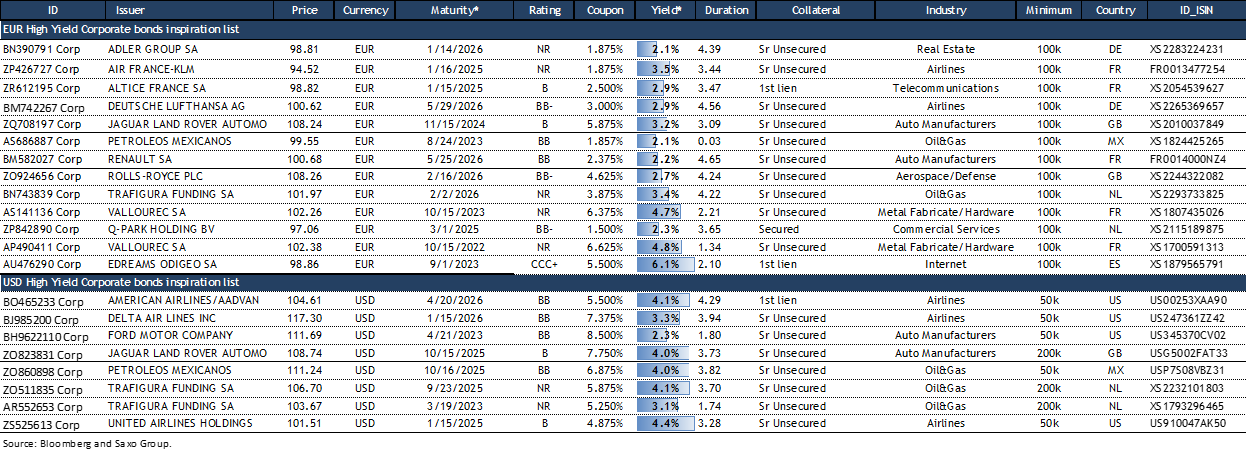

To simplify your search, below are some ETFand bonds, which can be helpful to consider in this environment.