FX Trading focus: USD holding its breath on cross-fire of factors.

Note: lucky me, the next two workdays are holidays for those in the financial service sector in Denmark, so this column will return on Monday, May 17.

On Monday, I took a stab at a few ways the USD move lower could play out after the shocking payrolls miss for April printed on Friday, and the price action since then has shown that the moving parts of the market are moving somewhat in conflict with one another, frustrating any follow on move lower for the greenback. The chief argument for US bears was the adjustment lower in Fed expectation after the weak payrolls data, which allows Fed members to sit on their hands for longer. But offsetting this, we have US long yields climbing since friday, helping to support the US dollar, as has the recent downdraft in risk sentiment. That very combination of weak risk sentiment and weak long bonds is highly unusual, and very stabilizing if it extends much longer, i.e., sufficiently to take the US 10- and 30-year treasury yields back toward the cycle highs (which are still some way off (I would expect if that develops, the USD will continue to make a stand and refuse to roll-over. To get the US dollar sustaining more persistent downside, we need risk sentiment to stabilize and relative US real yields to head lower still relative to peers.

Today we a have the economic calendar offering up plenty of possible triggers for shifting the odds for or against the US dollar, with the April US CPI release, Fed Vice Chair Clarida out speaking and a 10-year US treasury auction up later in the day.

In Europe, strong euro move of late is trying to find some more support from rising EU yields after the German Bund (10-year German sovereign yield) closed at a new local cycle high yesterday just shy of the post-pandemic outbreak high of -15 basis points. As with the above comments, this level likely needs breaking together with a stabilization of risk sentiment to set us on to the path of 1.2350+ in EURUSD, otherwise we risk bogging back down in the range with a close back below 1.2050.

Elsewhere, the CAD move remains impressive, almost too impressive, and it may be up to Bank of Canada governor Macklem to raise the strong CAD as an issue at a speech tomorrow to reverse or slow the move lower in USDCAD. Note EURSEK pushing on the local 10.10 area support as the last area ahead of 10.00, a fairly strong performance for SEK, given the recent weak global risk sentiment, and partly driven by a slightly hotter than expected 2.5% YoY inflation print, which was 0.1% above expectations (as were the month-on-month at 0.3%). That’s negative 3% real yields for Swedish deposit holders, for anyone that is counting. Apparently not many are counting, as Hungary yesterday printed a blistering 5.1% headline CPI reading – with no anticipation of imminent rate rises from the central bank there (in part as the core reading was only 3.0%).

Chart: AUDUSD

AUDUSD is a decent proxy for this latest USD move lower as well as the ramp since the pandemic lows in key commodities prices that are drivers of Australia’s economy, including especially iron ore. On that latter note, one thing that has likely held back the Aussie in the recent cycle is China’s ban on importing thermal coal from Australia and some discussion that China may halt LNG imports as a next step after halting strategic economic dialog talks “indefinitely” recently. The weak US payrolls on Friday drove the pair above the prior 0.7800-25 resistance, but the price action has gone nowhere since, restrained chiefly by weak risk sentiment. Meanwhile, the RBA, while it has teased the July meeting as being in play for adjustments in guidance, remains in wait and see mode together with the Fed, so short term Australia-US yields spreads, and even 10-year yield spreads, for that matter, are not signaling huge support for a move higher – 10 years a bit more so recently than the 2-year swap spread, which mid-range from the early March peak (right near 0 basis point, currently 6 basis points…yawn.). Tactically, if the pair closes back below 0.7750, traders will have a bearish reversal on their hands, while we likely need a new jolt lower in the US dollar that shifts the fundamental indicators more sharply against the greenback (together with a shift in risk sentiment back higher) to get the bullish case back on track.

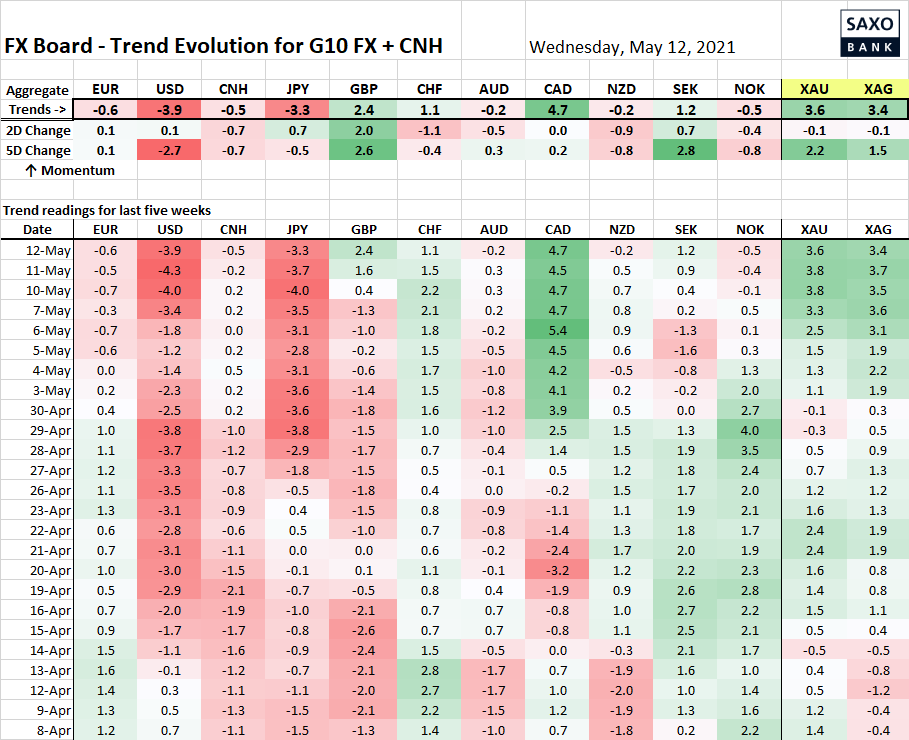

Table: FX Board of G-10+CNH trend evolution and strength

Not a lot of change to the recent developments since our last update, with the sterling move still strong, the AUD attempt to get something going however fading a bit, while CAD remains a standout on the trend strength.

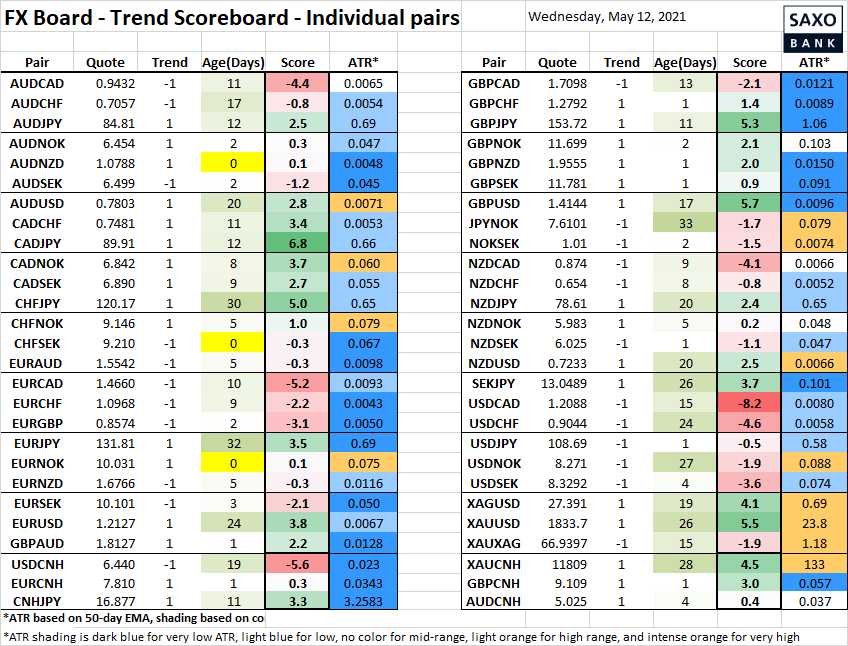

Table: FX Board Trend Scoreboard for individual pairs

Noting the AUDNZD and EURNOK flip-flopping hopelessly as a symptom of the near term struggle to get new momentum going in commodity-linked trades. The AUDUSD signal turned positive a full 20 session ago – at a daily closing price of…0.7728, only about a percent below the price as of this writing. Implied volatility is generally low and has remained surprisingly so through this latest bout of weak risk sentiment.

Upcoming Economic Calendar Highlights (all times GMT)

- 1230 – US Apr. CPI

- 1300 – US Fed Vice Chair Clarida (Voter) to speak on economic outlook

- 1700 – US 10-year Treasury Auction

- 2100 – New Zealand Apr. REINZ House Sales

- 2301 – UK Apr. RICS House Price Balance