FX Trading focus: JPY aggressively lower as yields bounce back after FOMC

The market got exactly what it expected yesterday from the FOMC, a statement with very few changes – basically small adjustments to the language describing the current state of the economy – and a Chair Powell presser that saw Powell doing everything to defend against the idea that the Fed even talked about when the appropriate time would be to talk about tapering purchases.

After the equity market close, risk sentiment enjoyed a boost and the USD sold off further on President Biden’s address before a joint session of Congress, one that outlined his priorities in the nearly $4 trillion of proposed stimulus packages on mostly infrastructure for the first round and social welfare programs for a later second round of $1.5 trillion. While he has tried to pay the bipartisan card in drumming up support for the bill, the 100% partisan vote on the last stimulus round could make his overtures a tough sell, which means that among others, the “kingmaker” vote in the Senate – “conservative Democrat” Joe Manchin, will need close watching for how much of the spending and taxation plans are likely to make it into law. For now, markets are not sweating the implications of eventual tax increases.

In yesterday’s piece, I perhaps overthought things in asking whether the treasury market might ignore the Fed’s wait-and-see approach and front-run an eventual taper message to be rolled out sometime this summer if inflation and employment levels are set to improve sharply. The immediate reaction was of course nothing of the sort, as the short end expectations for Fed tightening retreated slightly and the USD weakened fairly sharply, if modestly, while choppy longer Treasury and T-bond futures ended the day approximately unchanged relative to the day’s starting point. But the reaction by lunchtime here in Europe has developed in the opposite direction for yields at least, with a new local high in long US yields as German Bund (10-year sovereign) yields are also pressing on the key highs near -20 bps again today, helping to drive EURJPY to yet another cycle high in what has been a remarkable move from last Friday’s lows. A solid leg higher in EU yields would seem to be already priced into (as this rise would likely further tighten the EU-Japan yield spread, as Japan has declared the intent to cap 10-year Japanese Government Bond yields at 0.25%. Currently the 10-year JGB yield is +10 basis points, far below the early March high of +18 bps.

Chart: AUDUSD

AUDUSD has chopped back and forth and teased a break higher on a few occasions recently without following through, partly on the weak CPI print in Wednesday’s Asian session. And as I have noted previously, the backdrop looks very positive for a stronger Aussie if consider the basics like risk sentiment and we glance over at hot metals markets, while yield spread developments are utterly uninspiring to even negative for the pair and if US yields rise toward the cycle highs again, it could spook markets from commodities to equities, crimping risk sentiment and likely the AUD. The latter drag is probably why we aren’t already trading at 0.8200 or higher for AUDUSD. For now, we’ll let the technical developments lead the way, with a solid close above perhaps 0.7825 a hook for new longs that makes clear the risk/reward setup (stop south of 0.7770), while bears would either hope for a failed rally and then reversal or have to sit on their hands for a move back below at least 0.7700, if not 0.7650.

Elsewhere, the strong bid tone in risk sentiment in the wake of the FOMC meeting is boosting commodity FX and EM currencies, with USDCAD posting strong new lows for the cycle and the lowest since early 2018, while USDRUB has worked well back below the pivotal 75.00 area.

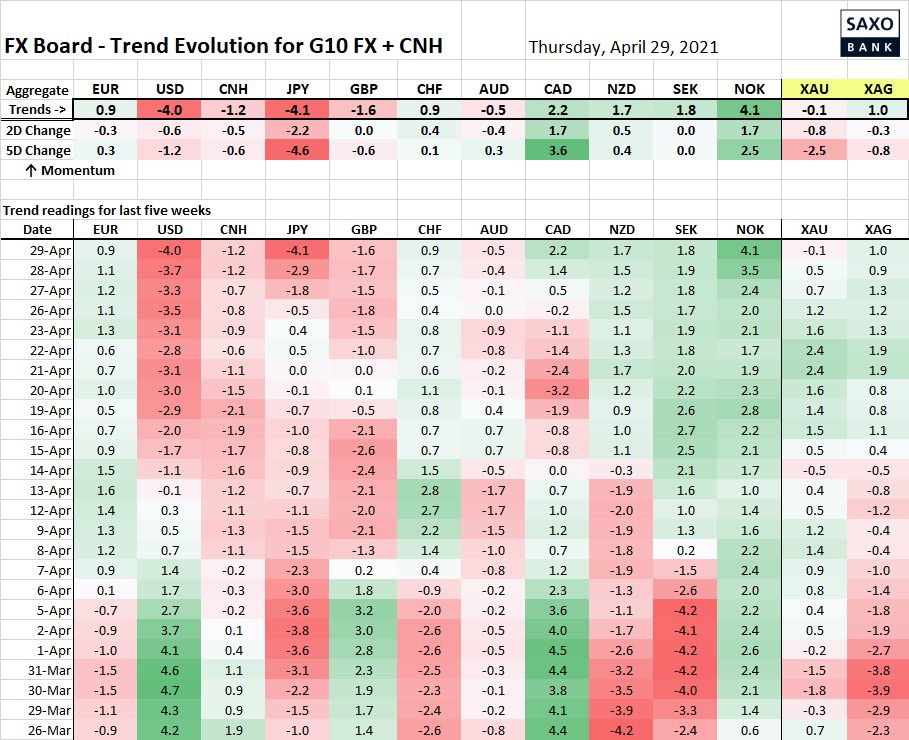

Table: FX Board of G-10+CNH trend evolution and strength

The JPY and USD are vying for bottom spot on the FX Board trend evolution, while NOK is taking the top spot in trending positive on the combination of a firmer euro and the highest oil prices in more than a month, as EURNOK marks a new cycle low today well below 10.00.

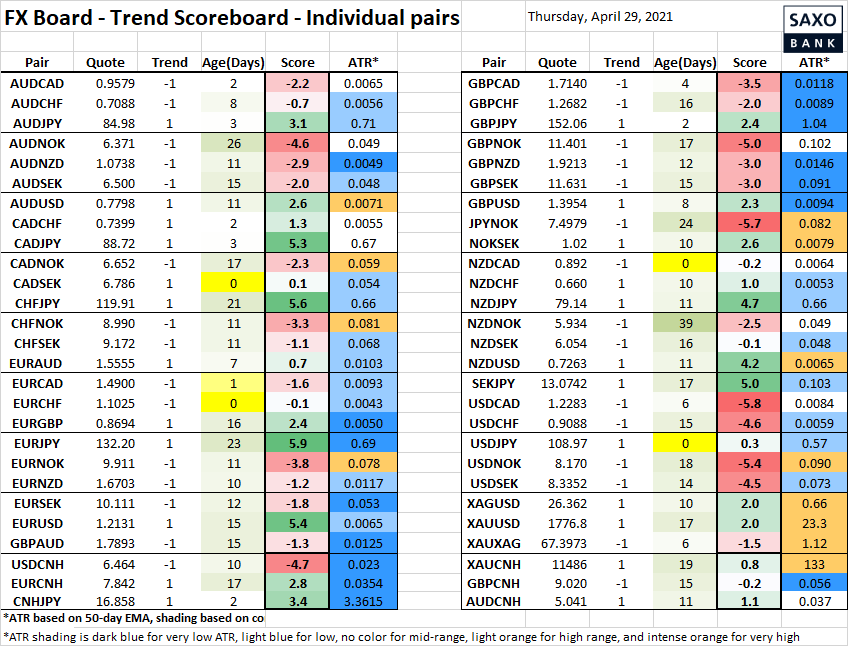

Table: FX Board Trend Scoreboard for individual pairs

The EURJPY rally now showing the hottest trend reading in the individual pairs, while USDNOK is and USDCAD are also running hard to the downside on the rise in oil prices. Note USDJPY trying to post a positive trend cross-over reading today, which is a tough one to buy without a more impulsive rally in US treasuries that supports the USD more broadly.

Upcoming Economic Calendar Highlights (all times GMT)

- 1200 – Germany Flash Apr. CPI

- 1230 – US Q1 GDP Estimate

- 1230 – US Weekly Initial Jobless Claims

- 1430 – US Weekly Natural Gas Storage Change

- 2330 – Japan Mar. Jobless Rate

- 2350 – Japan Mar. Industrial Production

- 0100 – China Apr. Manufacturing and Non-manufacturing PMI