Yesterday’s Federal Reserve meeting can hardly be labelled as a non-event for the financial market. Jerome Powell’s stubborn conviction that inflation will be transitory should make the market panic because no elements suggest that. On the contrary, the bloated Fed’s balance sheet and an unprecedented amount of budget stimulus point to sustained inflationary forces ahead.

Not to sound ancient, but let’s briefly talk about Milton Friedman and his teaching about monetary policy and inflation. According to the notorious economist, inflation is always a monetary phenomenon, and there is a lag in the effect of monetary policies. Therefore, inflation will be provoked by the exponential growth in the broad money supply we have witnessed since the Covid-19 pandemic. However, a lag in the reaction of monetary policies can lead the central bank to commit a policy mistake that the market will pay dearly.

In recent history, central banks committed a policy mistake that ultimately led to the Great Recession. Excessive accommodative monetary policies both in the US and Europe created macroeconomic imbalances, culminating with the 2007-2008 global financial crisis. At that point, authorities didn’t take into account the macroeconomic risks that their accommodative policies entailed. We can say the same about this time around, too. Equity valuations are at an incredibly high level, and the stock market hits new highs every other week. However, high valuations do not reflect deterioration within the credit space caused by skyrocketing leverage.

The current economic environment is challenging not only because assets are riskier than before and more expensive. For the first time in history, the market lacks a safe-heaven. Interest rates remain at ultra-low levels providing no buffer in case of rising inflation (real interest rates are negative) and little upside in case of a market crash (US Treasury yields will not dive below zero).

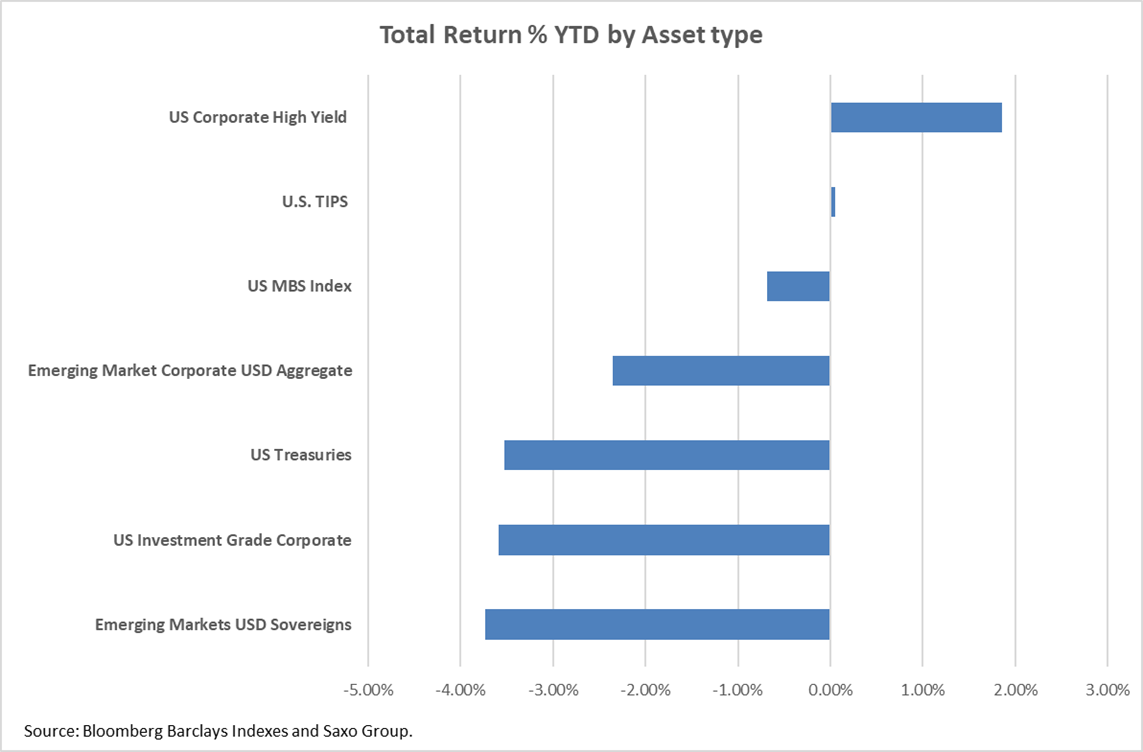

Therefore, it’s easy to explain the chart below. Since the beginning of the year, the only assets that provided positive returns are high yield corporate bonds and TIPS. Why? The only option for bond investors is to find shelter among the riskiest assets. Junk bonds are the only ones to provide a yield high enough to build a buffer against inflationary pressures. At the same time, TIPS serve to hedge against inflation.

Stay away from US Treasuries

Jerome Powell left US Treasuries extremely vulnerable by leaving monetary policy unchanged and improving the economic outlook slightly. Indeed, as the economy improves and inflationary pressure becomes more pronounced, US Treasury yields will resume their rise. We believe that 10-year US Treasuries can hit 2% by summer. At this level US Treasuries will find strong resistance. The big question is, what will happen at 2%? Will the stock market tumble, or will it weather the rise in rates? If the selloff in equities is substantial, US yields may retreat below their pivotal level. Still, there is a bigger chance that amid a correction, the macro-economic backdrop continues to improve, pushing yields even higher.

Within this context, it doesn’t make sense to hold US Treasuries. Even if 10-year Treasury yields dive below 1%, the upside remains limited because the Fed said several times it wouldn’t tolerate negative interest rate policy (NIRP). However, the downside is unlimited because yields can rise well above 2%, depending on inflation expectations.

Keep close to the economic recovery. Pick risk and duration carefully.

We believe it is best to look within the US high yield corporate space over emerging markets because the first will be closer to the economic recovery. Moreover, junk corporate bonds are offering a substantially higher yield compared to EM sovereigns. Indeed, high yield corporate bonds provide a yield of 4% for less than four years duration. To get the same yield within the EM sovereign bond space, it’s necessary to extend the duration to 8-years, exposing one’s portfolio to interest rates sensitivity even further.

Neither assets come without risks. Indeed leverage in both the corporate sector and the EM sovereign space is increasingly high. This is why it is necessary to cherry-pick and be comfortable to hold their debt till maturity. The goal is to lock in a yield high enough without running into defaults. However, you should expect a repricing of these assets as Treasury yields aim higher.