- What: There is need to reduce risk into Q4 – Stagflation light is a real risk.

- Why: In the official narrative, inflation is moving from “transitory” to “temporary” (but is actually structural in our view) with waning real growth as energy prices are out of control. We are talking about 2-3 times more expensive energy costs for consumers and companies. This will hit margins and is a tax on growth.

- What to do: No reason to panic, but reduce risk or buy protection. Long volatility or Long puts.(Talk to your account manager or GST support for ideas…) Alternatively or in addition, look to buy Commodity Indices which continue to perform under supply constraints and rising energy demand. (See the example below).

- What else: Seasonality is bad in September and October and the German election could lead to Bund yields rising, Middle East (Iran, etc.) could see crude oil above $80.

- Saxo Strats views: We are moving to reduce only on equity exposure until further notice and buying PUT on US indices….

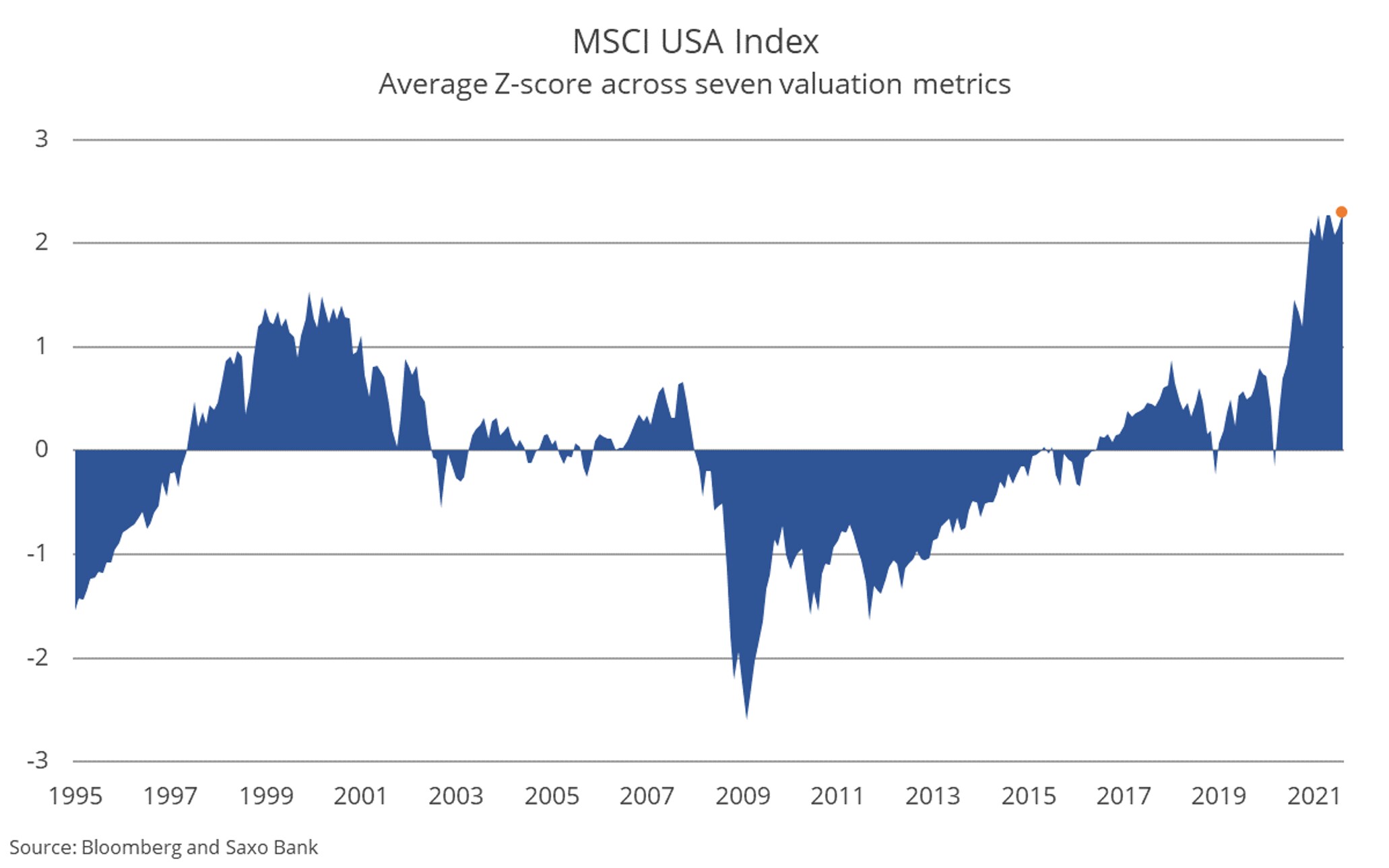

Chart: our internal valuation model. Below is a Z-score model derived from seven different measures of the stock market valuation. This is to avoid bias in data, but this chart is clear: the market has never been more expensive, ever!

On top of this several chart lines are at risk …. Most of them originating from the pandemic outbreak lows in 2020…..

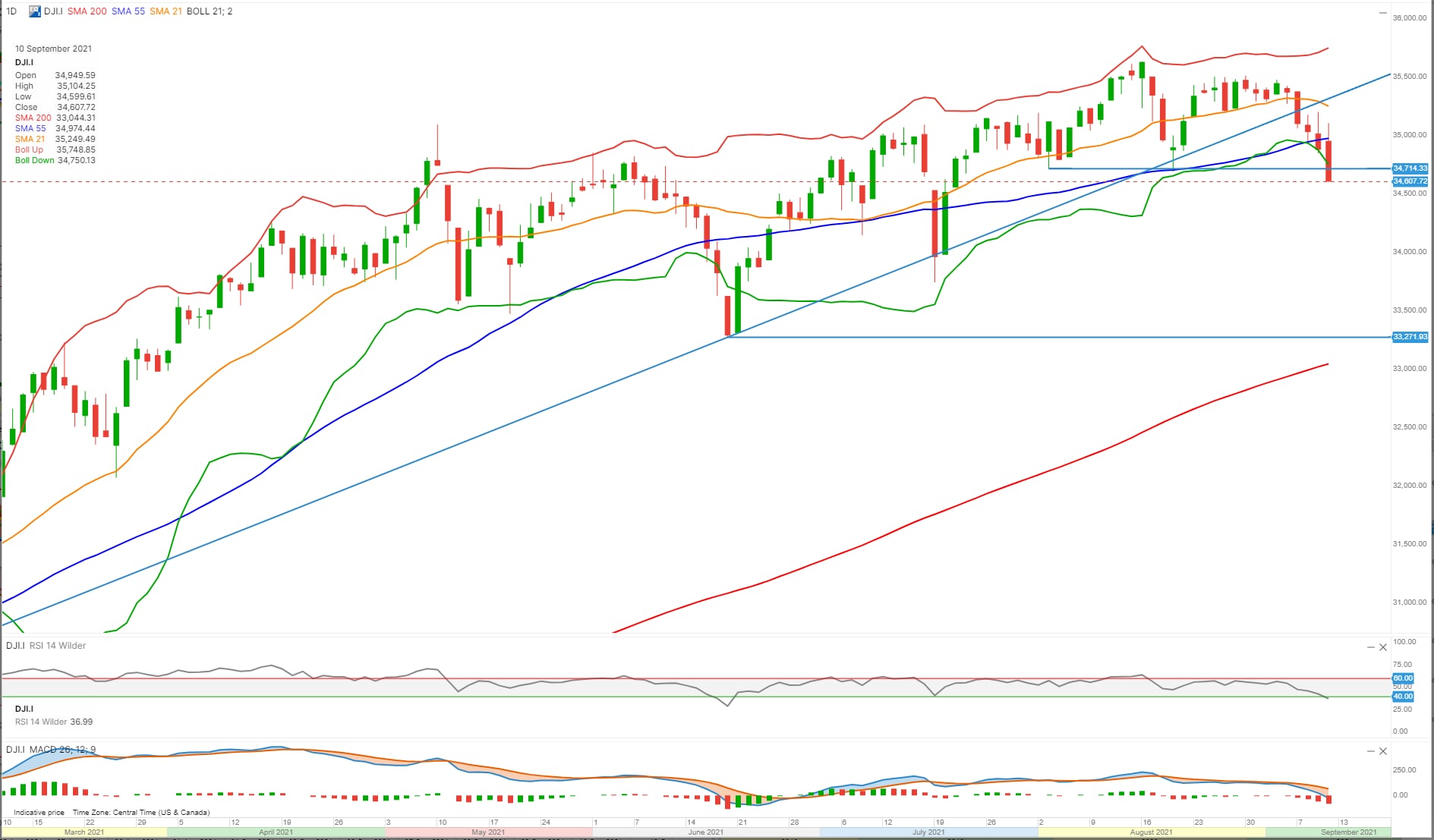

Then this from Kim Cramer Larsson – our in-house chartist:

“With its close below support at 34,714 Friday Dow Jones Industrial Average Index has established a bearish trend. RSI below 40 is confirming the bear picture and we could see lower levels over the next week or so.

To reverse the downtrend a close above 35,510 is needed. First warning of that scenario unfolding would be for the Index to break back above the rising trend line its broke last week.

However, what is interesting is that the Future has not yet confirmed a bearish trend. The Future closed just above its support at around 34,572 Friday and has started the week on a positive note. However, RSI dipped below 40 indicating negative sentiment meaning the support could easily come under pressure next few days. A break and close below could fuel selloff down to strong support at around 33,285.”

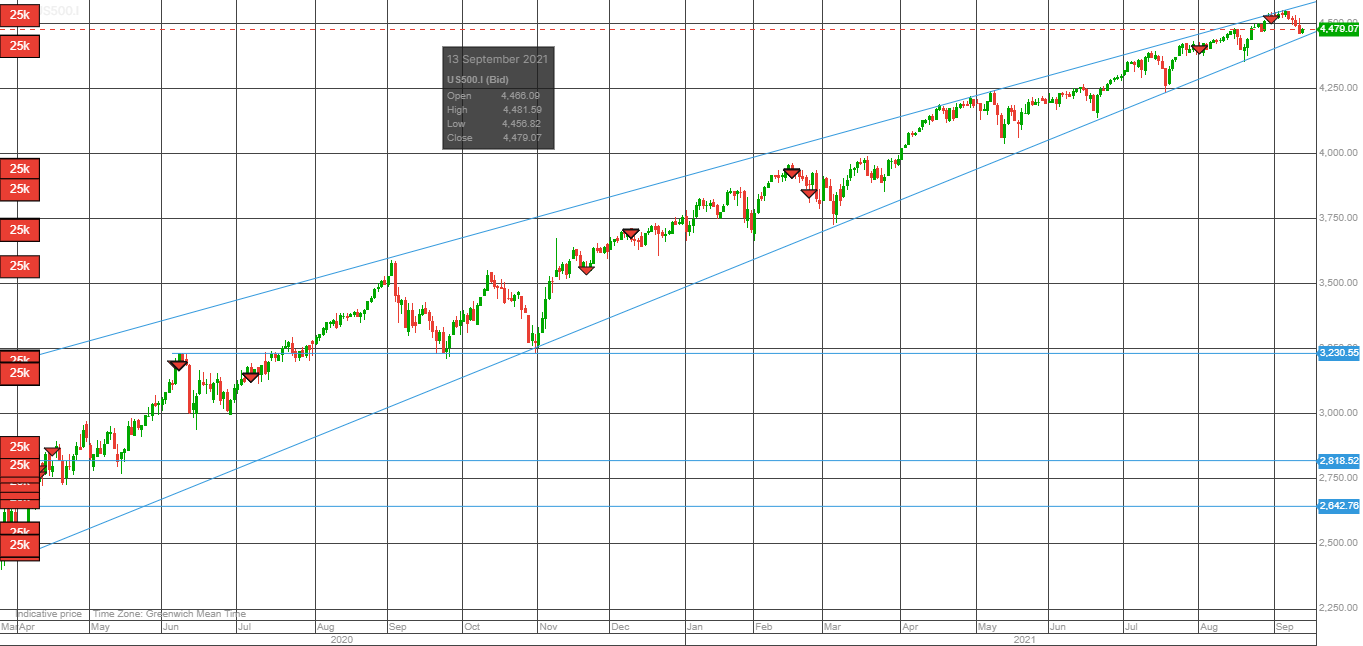

Courtesy of Kim Fournais, this long-term SPX chart:

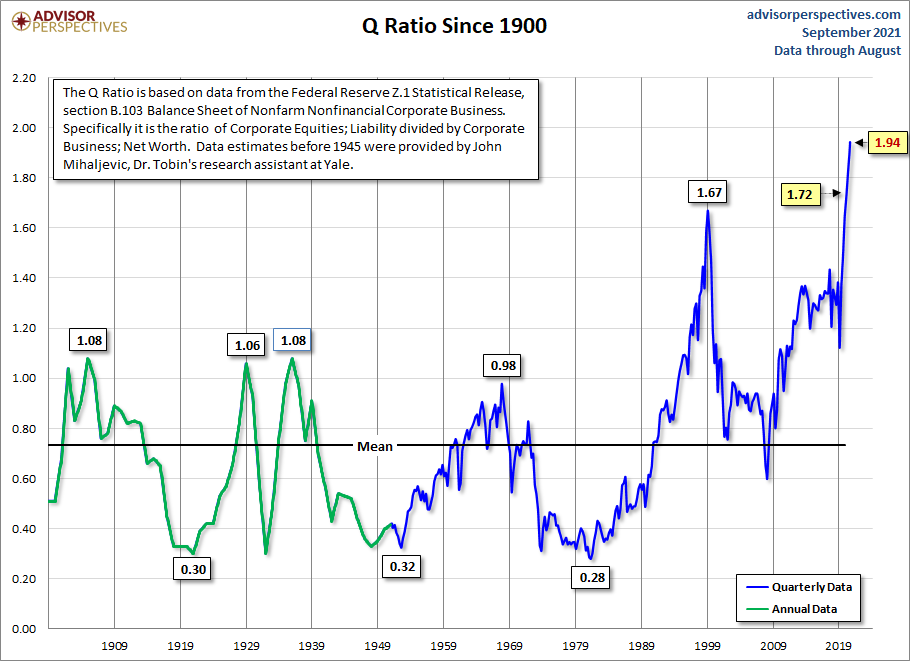

The Buffett Indicator: The Tobin Q valuation

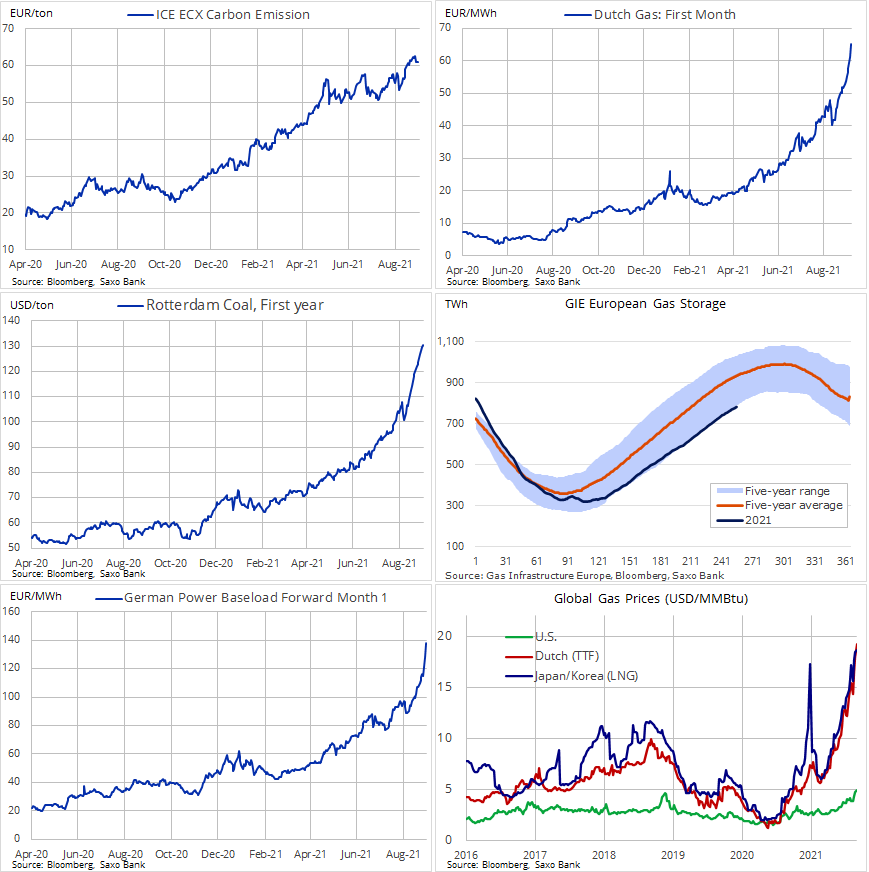

Cost pressures / Inflation remain very underestimated:

courtesy @Ole S Hansen (OLH).

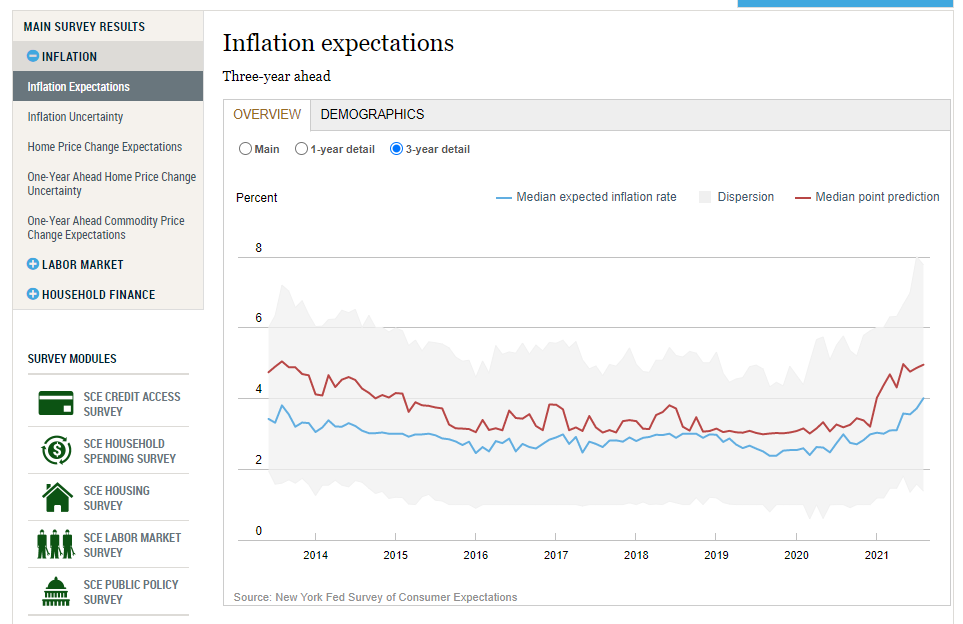

And then there are inflation expectations, which have seen in a seismic shift by some measures, including the New York survey of 1- and 3-year forward inflation expectations. Fed officials often refer to whether inflation is well-anchored – in our view, it is rapidly becoming downright unhinged. A further rise in rates to reflect these higher inflationary outcomes and rising expectations is coming and soon, driven by supply chain disruptions and this massive increase in energy input prices. I advise several companies, speak in front of even more, and none have hedged this move – not a one.

Invesco DB Commodity Index Tracking Fund:

Conclusion:

Only inflation can stop this equity market, it’s that simple. And we know the response function from policymakers as well. If or when this market drops, then ever large fiscal and accompanying monetary interventions will be mobilized and most of it tilted to more ESG and Green Transformation priorities. What policymakers have failed to account is the premise we outlines months ago: The physical world is simply too small for the attempt at upgrading infrastructure, fighting inequality with ESG and fighting climate change with the green transformation. Just this week, the UK is paying up huge amounts to fire up coal plants to keep the lights on, and tonight Illinois will probably halt the formerly scheduled decommissioning of the state’s nuclear power stations. A friend of mine commented that “Policy makers are now more fearful of blackouts than climate change”… Reality struck this week in energy and just maybe in risky assets.