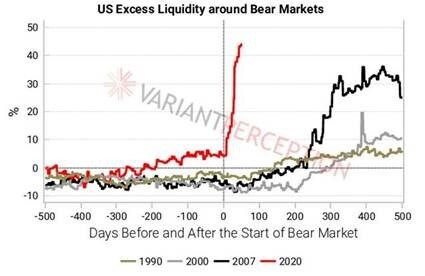

As the S&P 500 erases 2020 losses it has become clear that once again the gains of unconventional expansionary monetary policies gush over those who need it least, amplifying wealth disparities. This as the ownership of financial assets has become more concentrated to the top tier of net wealth distributions over the past 3 decades. However, as has been the case for many weeks, the narrative on the ground is not driving risk assets. Although the dichotomy bears note, not only with respect to the time decay of economic optimism and liquidity driven markets, but also the long term implications for financial stability and our social fabric.

As we have said before, the hope trade is firmly rooted in abundant liquidity and the promise of more if necessary, as central bankers bid to backstop asset prices. Along with the flows of investors driven up the risk spectrum via the lack of alternative (TINA) and the expectation that rates will remain low for an extended period. The sharp rebound off the March lows in turn drives continued speculative behaviour, as the fear of missing out (FOMO) becomes a driver and in this paradigm markets remain biased to the upside. Investors conditioned by the central bank put to “buy the dip” are reaching for yield and piling into risk assets as economic optimism grows around the re-opening of economies and slowing COVID-19 case growth. There is almost a perception of an unlosable game. Rationality has been swept aside, in favour of the notion that if the economy does recover far quicker than expected, the market has been right all along – win; if the economic recovery lags expectations, central banks will make good on their pledge to provide support as needed – win. The collective outcome of these drivers has resulted in risk assets rising with seemingly zero gravity. Resistance is futile, and expensive, but for those that share our fundamental view we can take comfort in that the very existence of TINA dictates you do not need to be positive on the expectations of a swift economic recovery, to be long stocks (and by default short cash/efficient markets). History teaches us, irrationality can persist in financial markets for far longer than you can remian solvent.

Moral hazard (when an entity has an incentive to increase its exposure to risk because it does not bear the full costs of that risk) in the form of FOMO/TINA and longer-term thematics (undermining social fabric) aside, liquidity induced bullish price action remains front and centre for the week ahead. Along with rising treasury yields, USD weakness and the prospects of YCC into Wednesday’s FOMC meeting.

Yield Curve Control (YCC)

YCC control was discussed at the previous FOMC meeting and with yields on the rise and the treasury curve steepening as bonds have continued to sell off, the question is turning to when not if. In an interview last week, the New York President, John Williams, confirmed the Fed are “thinking hard” about the prospect of targeting specific yields.

What is Yield Curve Control? YCC, where the central bank targets a specific long-term rate, as opposed to amount of bond purchases (QE) could be used to anchor various durations at certain levels. This lowers the cost of borrowing for debt instruments priced off treasury securities. Ensuring that whilst inflation remains low and deflation a risk, real yields are also harnessed, along with the unwanted implications of rising real yields on other asset classes. With YCC also comes the de facto monetisation of fiscal deficits as borrowing costs are kept low in the face of a huge amount of bond issuance required to fund the pandemic related relief packages. The adoption of YCC could also mean that because a specific quantity of purchase are not required, the Fed’s balance sheet may grow at a lesser pace. As we have seen in Australia, the RBA have been able to taper their securities purchase whilst keeping the 3-year yield anchored. Governor Lael Brainard has also spoken in support of capping yields for certain maturities.

Although last week’s rise in yields has stalled somewhat, the risks into this week’s FOMC meeting of YCC adoption being delayed and some better than expected data, along with the optics of the NASDAQ at record highs errs on the side of caution. With valuations at historic levels, it does not take much to upset the apple cart. A push higher in yields and bounce in the USD if Powell fails to deliver on the dovish rhetoric could prompt an uptick in volatility and some profit taking across technically stretched US equity indices.

Although risk assets are trading in a liquidity honeymoon, as we outlined above, risk-reward into this week favours a more cautious approach. Although the path of least resistance medium-term remains the rally continues due to the aforementioned liquidity induced fever. With so many unknowns remaining with respect to both economic normalisation and the virus itself, for short-term traders, now is the time to tighten stops and book some gains.

The ASX 200 has breached the 6,000 level marking a 9.6% gain in the last 2 weeks, outpacing even the surging Aussie dollar. This as investors contemplate the early re-opening of the economy as on a relative basis the Australian lockdowns have largely succeeded in containing the virus itself. Although the economic impact has been deep and devastating for many, with more than half a million jobs shed, in a relative world Australia still looks lucky.