What is our trading focus?

XAUUSD – Spot gold

XAGUSD – Spot silver

XAUXAG – Gold-Silver ratio

GLD:arcx – SPDR Gold Shares ETF

GDX:arcx – VanEck Gold Miners ETF

____________________________________________________________________________________________________

Global markets await tomorrow’s FOMC meeting with perhaps a bit more excitement than a meeting at this stage in the cycle would normally attract. The reason being last week’s upside break in longer dated bond yields following the stronger-than-expected US job report. This has led to renewed speculation about how ready the Fed is to implement yield-curve control (YCC).

A decision to introduce yield caps, on maturities out to five or perhaps even ten years, could be an important next step for risk assets, the Dollar and not least gold. Any hesitancy from the Fed tomorrow, on the other hand, could mean that risky assets have over-shot their potential for now and see a steep correction in risk assets in the near term and a back-up in the US dollar.

So far this week longer US treasury yields have backed down from the big move last week, likely as treasury traders are concerned about the message from the Fed, as any lack of clear intent to shift to an eventual yield-curve-control could see steepening set to continue. (alternatively, the yield curve could flatten if the markets feel that the Fed has grown uncomfortable with the markets’ current speculative frenzy).

From a gold perspective the reaction to a no-change would likely be mixed with the risk of rising yields and a weaker Japanese yen being off-set by potential weakness in stocks. On the other hand the introduction of a cap on longer dated yields could in our opinion be the trigger that lays the foundation for the next move up in gold prices.

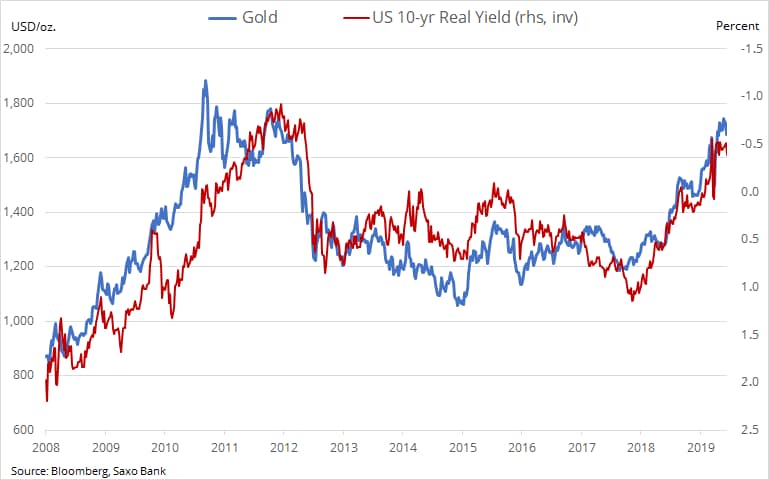

Gold’s long established inverse correlation with US real yields is already well established as per the above chart. Some of the major moves in gold during the past decade often started with developments in the bond market. The real yield is the return an investor get on holding a bond position once the nominal yield has been reduced by the expected inflation during the life of the bond. Rising inflation expectations would normally increase the nominal yield as investors would want to be compensated for the lower real return.

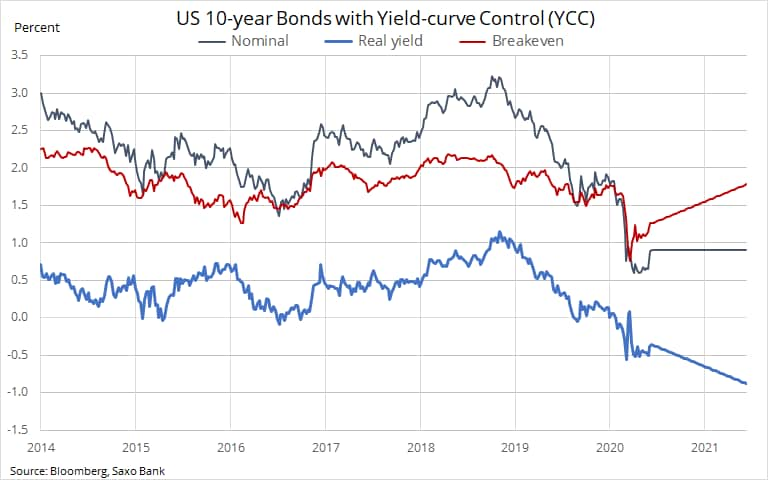

Yield-curve control locks the nominal yield at a certain maturity at a certain level above which the central bank steps in and buy whatever bonds are on offer in order to prevent yields from rising any further. Such a development would make fixed income investments utter useless as a safe haven asset, especially into a period where inflation is expected to make a comeback. Not only due to the massive amount of liquidity that central banks have provided but also due to unprecedented government stimulus creating the political need for higher inflation to support rising debt levels.

For now gold remains anchored around $1700/oz with speculative binge buying of stocks reducing demand for safe haven and diversification. The market has already firmly shifted the focus away from the Covid-19 pandemic to a V-shaped economic recovery. This at a time where economic data continues to paint a different picture while the pandemic, despite improvements in some regions, is still not under control. The WHO in their latest update said new daily cases have exceeded 100,000 in nine out of the past ten days with a record 135,000 new cases having been reported on Sunday. The bulk of recent cases coming from 10 countries, mostly in Americas and South Asia.

In my latest gold update here and video interview with Kitco News here, both written and recorded before Friday’s US report, I highlighted our reasons for maintaining a bullish outlook for gold and with that also silver. The recent price action has also once again put on display gold’s ability to frustrate while highlighting the need to be patience.

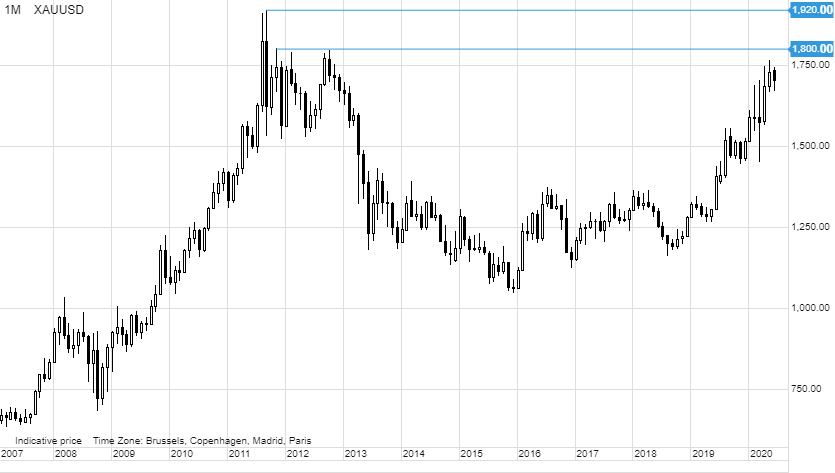

Hedge funds have cut bullish futures bet to a one-year low and this group of traders will have to re-engage on the long side before seeing gold trade higher. Hence the increased focus on the FOMC and with that the potential reaction across other asset classes. From a technical perspective a break above $1800/oz would be the trigger needed to send gold towards a new record high, thereby joining the multiple records already seen in other currencies so far this year.