What is our trading focus?

OILUKJUL21 – Brent Crude Oil (July)

OILUSJUN21 – WTI Crude Oil (June)

GASOLINEJUN21 – RBOB Gasoline (June)

NATGASJUN21 – Natural Gas (June)

____________________________________________________________________________________________________

The commodity sector remains on a tear with several key raw materials from copper and iron ore to corn and palm oil trading at or near multi-year highs. Inadvertently thereby adding to the debate over whether commodity-driven inflation pressures will be persistent enough to force the Federal Reserve to tighten policy sooner than currently expected. Hence the focus on today’s U.S. CPI data which is expected to show a year-on-year jump of 3.6%. With most of the change being down to seasonality, the focus may for once be centered on the monthly increased, expected at just 0.2% compared with 0.6% in March.

The rally this past week has been led by industrial metals and grains while crude oil and natural gas for various reasons have struggled to keep up. Overall, however, the Bloomberg Commodity Spot index is trading at a fresh ten-year high, and now up by one-third since early November when vaccine news accelerated growth and demand expectations.

As mention crude oil and natural gas have both been lagging some of the blistering pace of other commodities this past week. Oil continues to be torn between the uneven recovery in global fuel demand, especially due to continued virus flareups across Asia. Adding to this has been the disastrous hacking attack on the Colonial Pipeline which supplies 2.5 million barrels/day of fuel products from refineries in Texas to consumers along the U.S. East coast. As a result the U.S. national average retail gasoline prices have risen above $3 a gallon for the first time since 2014, but while fuel stations across the East and South have started to run out, some refineries have been forced to cut runs leading to lower demand for crude oil.

A bigger-than-expected cut in crude stocks, reported by the American Petroleum Institute last night, was offset by a big increase in gasoline stocks. The weekly petroleum status report from the Energy Information Administration is due later at 14:30 GMT, and as per usual I will publish the result and charts on my Twitter profile @ole_s_hansen.

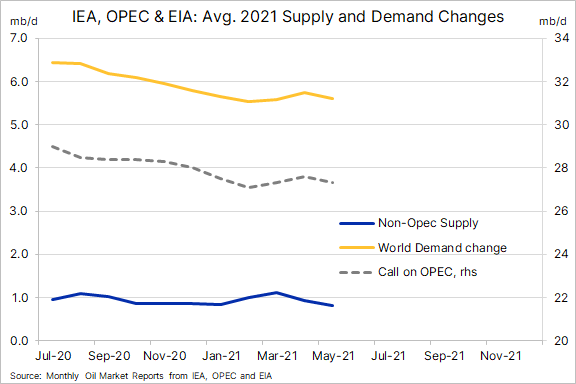

During the week, OPEC, the IEA and the EIA have all published their monthly oil market reports. Overall no major changes were made with world oil demand seeing a small downgrade due to virus breakouts in Asia while non-OPEC supply was lowered due to slower US shale growth.

Since late March Brent crude oil has traded in a rising but narrowing channel, currently between $70.80 and $67.25, the latter also being the 21-day moving average, a technical indicator which gives a good idea about short term momentum. We struggle to see Brent make much short-term headway above the triple top at $71.3, so while urging short-term caution we maintain a bullish outlook for the second half of 2021, primarily due to the prospect for a rapid growth in global fuel demand as vaccine rollouts reduce the impact of local virus flareups.

Natural Gas has spent the past couple of weeks trading sideways within a relative tight range between the $2.86 and $2.98, levels that represents the 50% and 68.2% Fibonacci corrections of the February to March sell-off. The close proximity to the rising trend line from the April low points to a market that is getting ready for break, either towards $2.80 or higher towards the February high around $3.31.